The European investment market is highly developed, but the digital experience remains uneven: even leading platforms show limited maturity across core user scenarios.

Markswebb analysts studied the digital investment landscape in Europe to reveal how this fast-growing market actually works from the inside.

The research aims to uncover market structure (supply), audience behavior (demand), and the gaps between them that create opportunities for digital services.

All key insights and materials are included in the full report: benchmark results, analysis of the digital investment services landscape and investor profiles, and a curated library of best practices.

The public report includes a curated set of best practices, 10+ UX insights, and a detailed overview of the European digital investment landscape. It also provides access to a free interactive map of digital investment services and the underlying dataset.

What you will gain from the research

• Find high-impact features and solutions across service types and user scenarios.

• Avoid common mistakes and recurring UX issues in the market.

• Understand investor behavior and design faster for all segments.

Contents

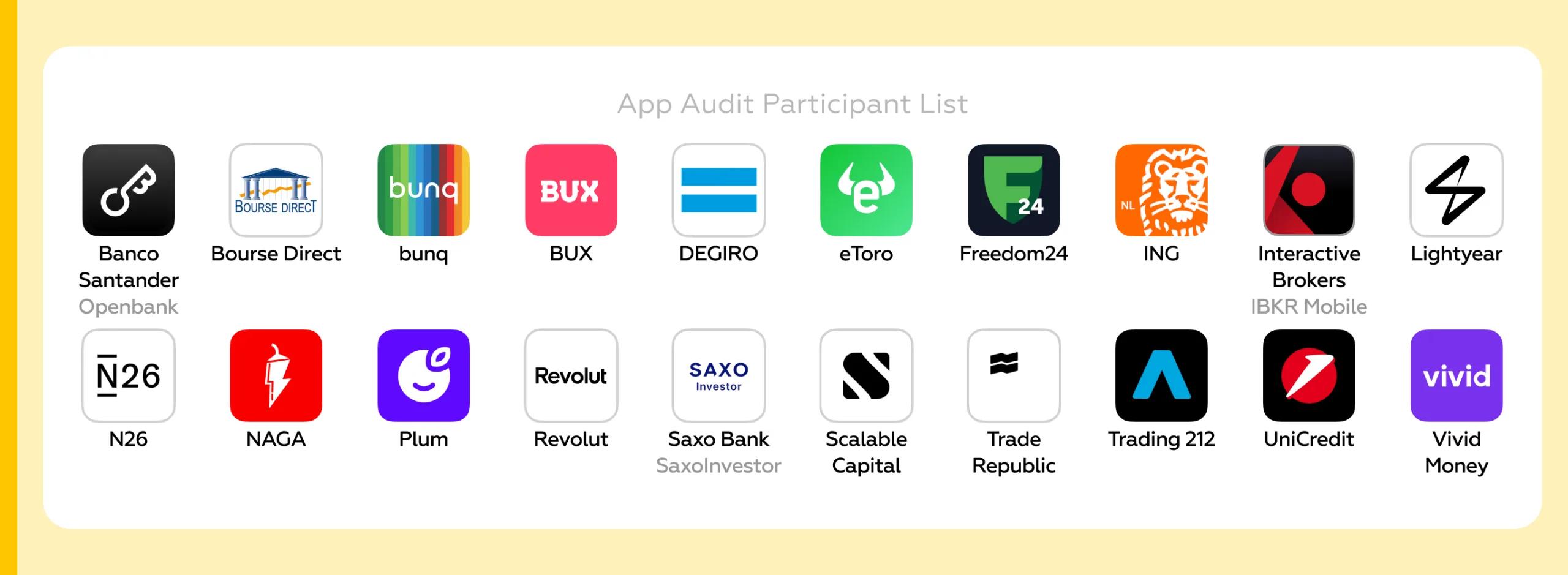

The study covers leading digital investment services in Europe, including: Revolut, Saxo Bank (SaxoInvestor), Interactive Brokers (IBKR Mobile), Trading 212, Trade Republic, eToro, Scalable Capital, Lightyear, N26, Freedom24, BUX, DEGIRO, ING, Vivid Money, bunq, NAGA, Banco Santander (Openbank), Plum, Bourse Direct, and UniCredit.

The European investment market has been shaped over decades and today demonstrates a high level of maturity — both in terms of supply and user behavior.

At the same time, competition remains intense. Alongside traditional banks and brokers, neobrokers, crypto platforms, and robo-advisors are rapidly expanding. This creates an environment where new product models, interfaces, and user interaction scenarios are constantly tested and refined.

The relative independence of investment services from the traditional banking sector accelerates this evolution.

Additional momentum came from macroeconomic shifts. In 2022, inflation in Europe reached 8.3% and remained above target levels in 2023. This significantly changed user behavior: traditional savings instruments are no longer perceived as a reliable way to preserve capital.

Against this backdrop, investing has shifted from being optional to essential, further amplified by digital accessibility. The number of retail investors has grown, intensifying competition for user attention.

The key growth driver is the quality of user experience — usability, transparency, and the ability to adapt quickly to changing user needs.

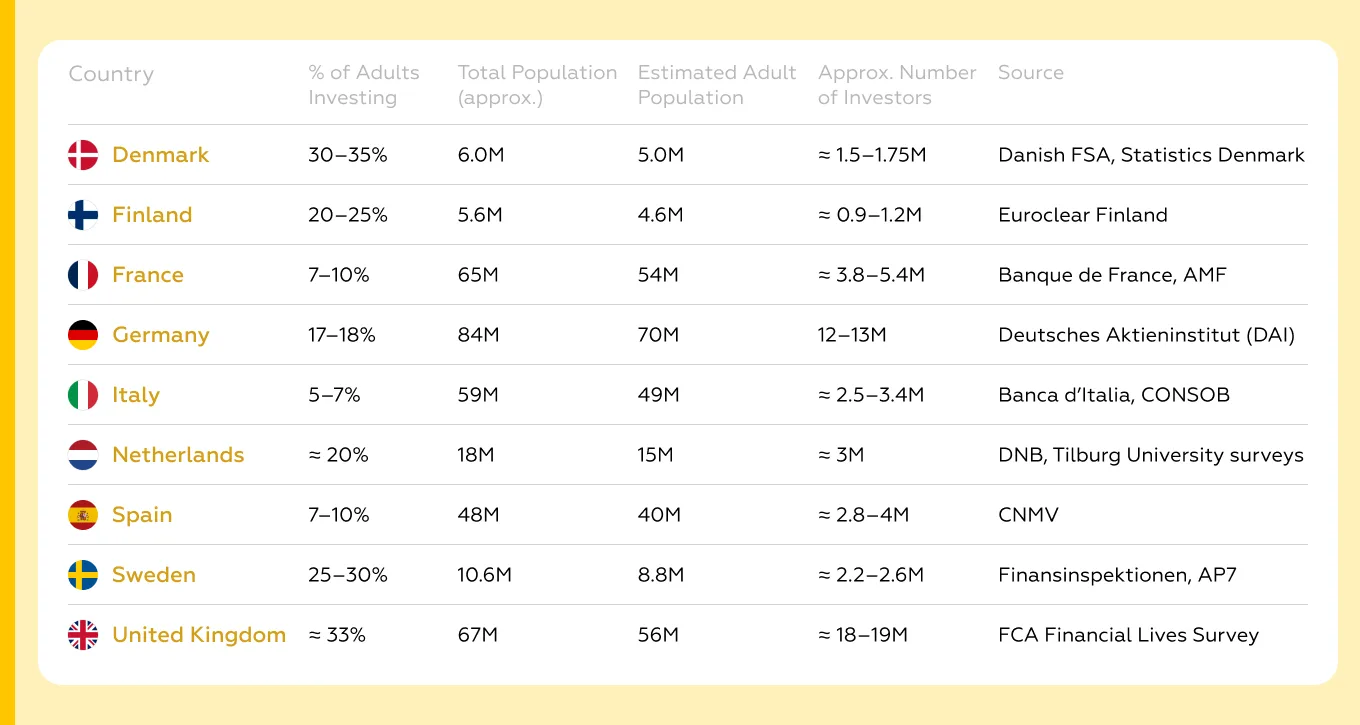

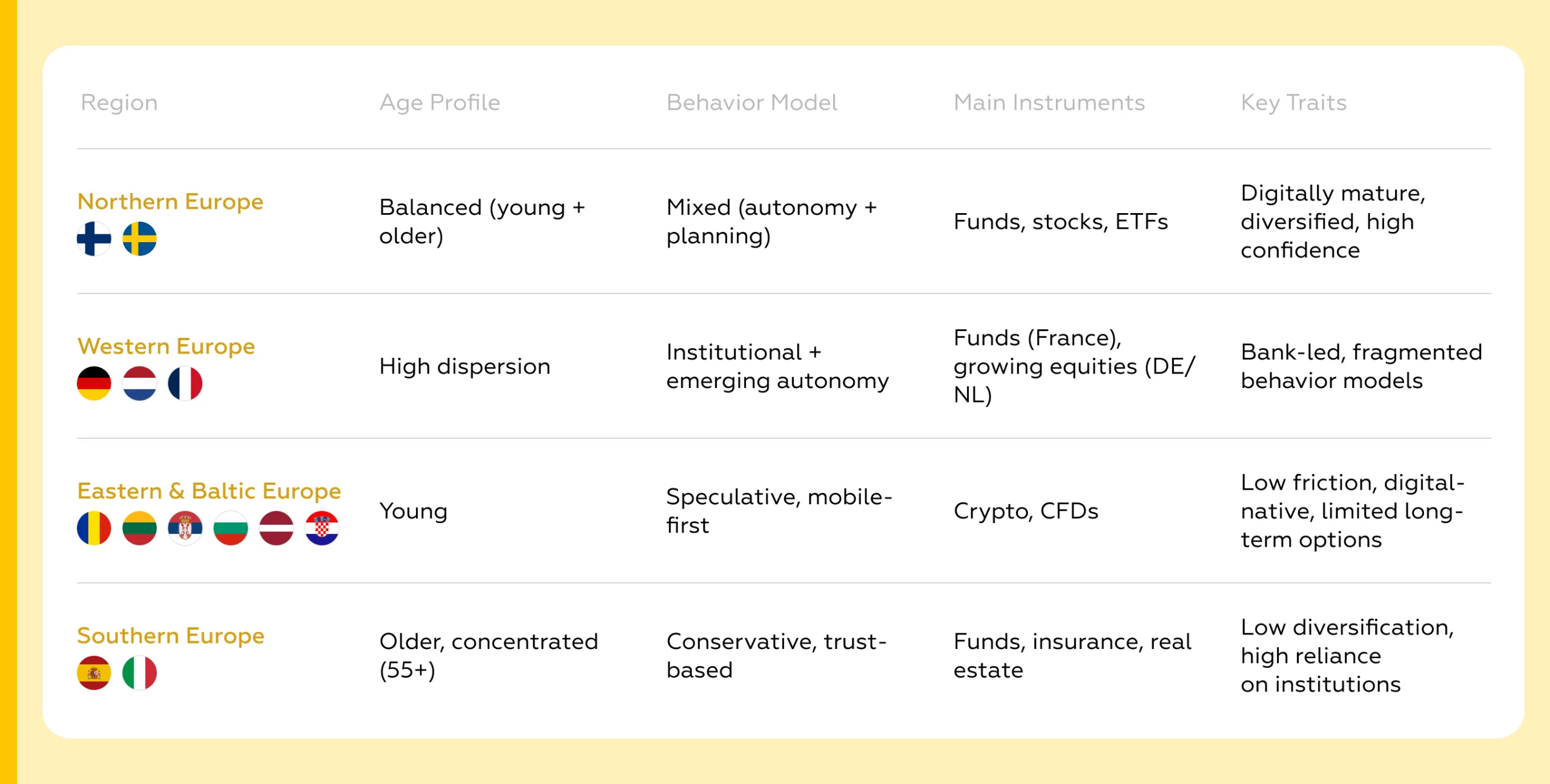

Investor participation differs significantly across Europe, with Northern Europe showing the highest levels of retail investment activity. Denmark, Sweden, Finland, the Netherlands, and the United Kingdom stand out by both the share of adults investing and the estimated number of retail investors.

The figures below are based on the best available public estimates, as comparable Europe-wide statistics are limited. “Adults investing” refers to adults holding at least one investment product, while absolute investor numbers are approximate and should be interpreted as order-of-magnitude estimates rather than precise counts.

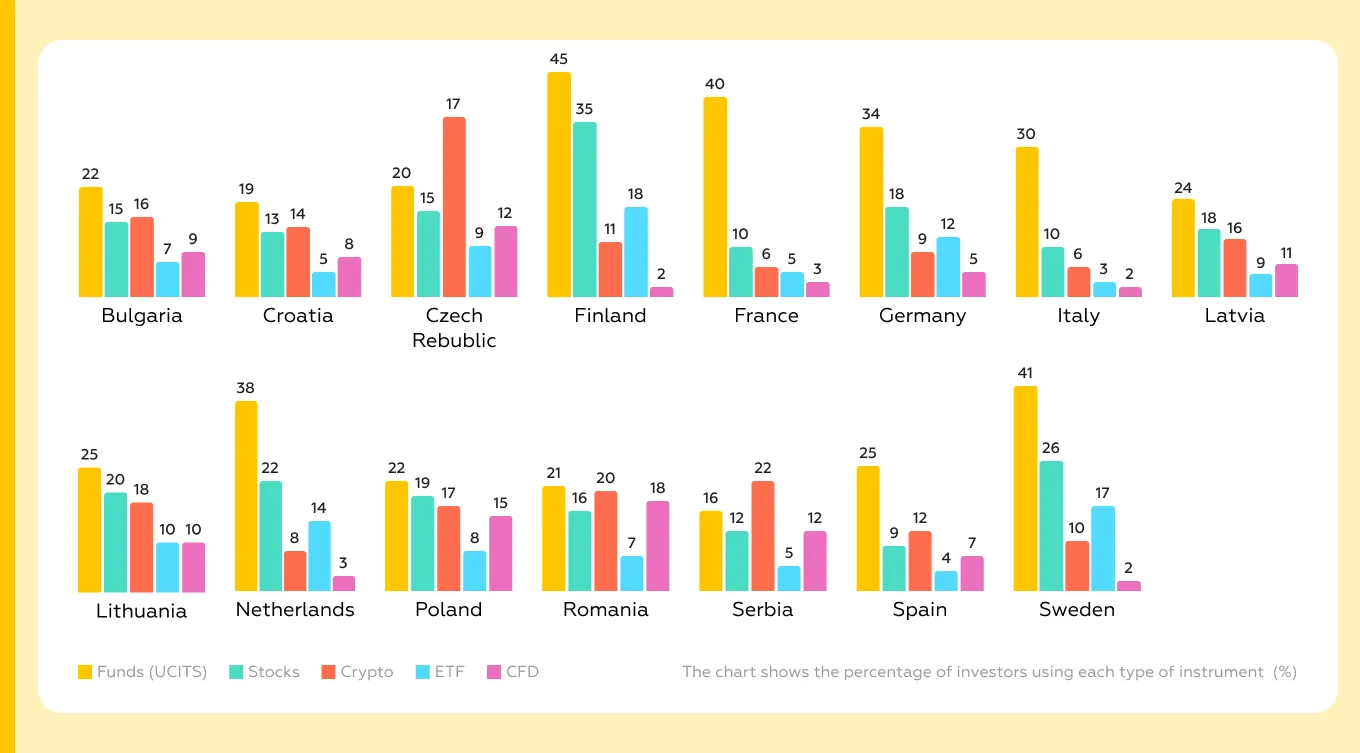

The structure of investment instruments shows how mature and autonomous different European markets are.

In more conservative, bank-led markets, investors still rely heavily on managed products. Mutual funds remain the dominant instrument: they account for an average of 37% in Western Europe and 25% in Southern Europe. This reflects a more guided investment model, where users are more likely to trust banks, advisors, and packaged investment solutions.

In more autonomous markets, the picture is different. Direct stock investing and ETFs are much more common, especially in Northern Europe, where these instruments together account for 45% of investor portfolios. In Southern Europe, by contrast, stocks and ETFs make up only 15%, showing a lower level of self-directed investment behavior.

Eastern Europe stands out for a higher share of speculative instruments. Crypto assets and CFDs together average 30% across Eastern European markets, compared with 11% in Western Europe and 12% in Northern Europe. This pattern reflects a combination of lower entry barriers, more speculative investor behavior, lighter regulation, and a weaker presence of legacy financial institutions in some markets.

For digital investment services, this means that product architecture should reflect the dominant investment behavior in each region. Markets with high stock and ETF penetration need autonomy-first platforms: transparent pricing, easy comparison of instruments, strong analytics, and low-friction execution. In regions where speculative instruments are more common, services need stronger onboarding, clear risk explanations, and protective layers that help users understand the consequences of their decisions before they invest.

There is no single investment model in Europe — preferences vary significantly across regions. The key difference lies not in the instruments themselves, but in how they are combined and the roles they play within a portfolio.

to explore the full ranking tables and compare how leading European investment platforms perform across different investment scenarios

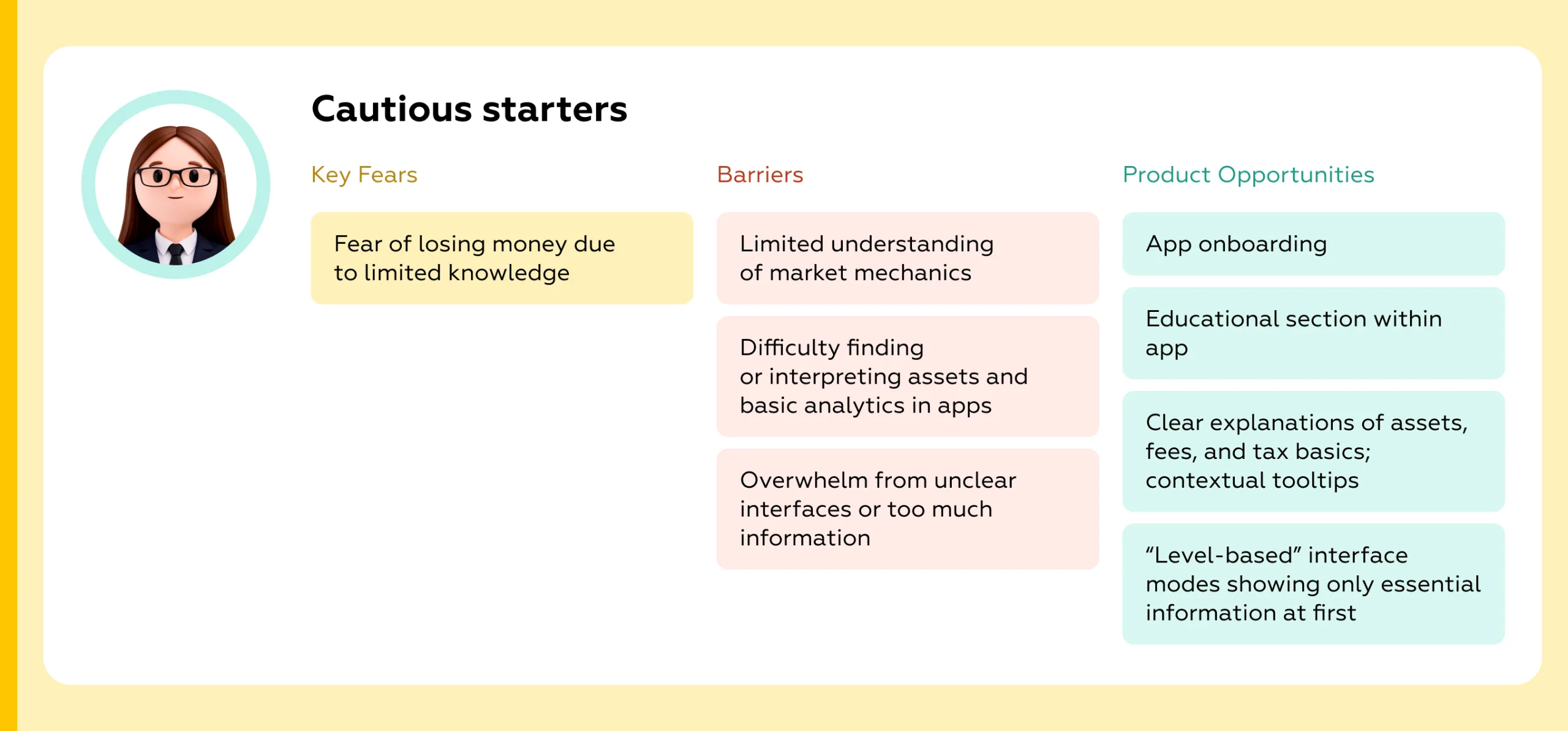

Based on in-depth interviews, we found that investor behavior in Europe consistently falls into four distinct segments:

1. Cautious Starters Perceive the market as complex and are highly sensitive to mistakes

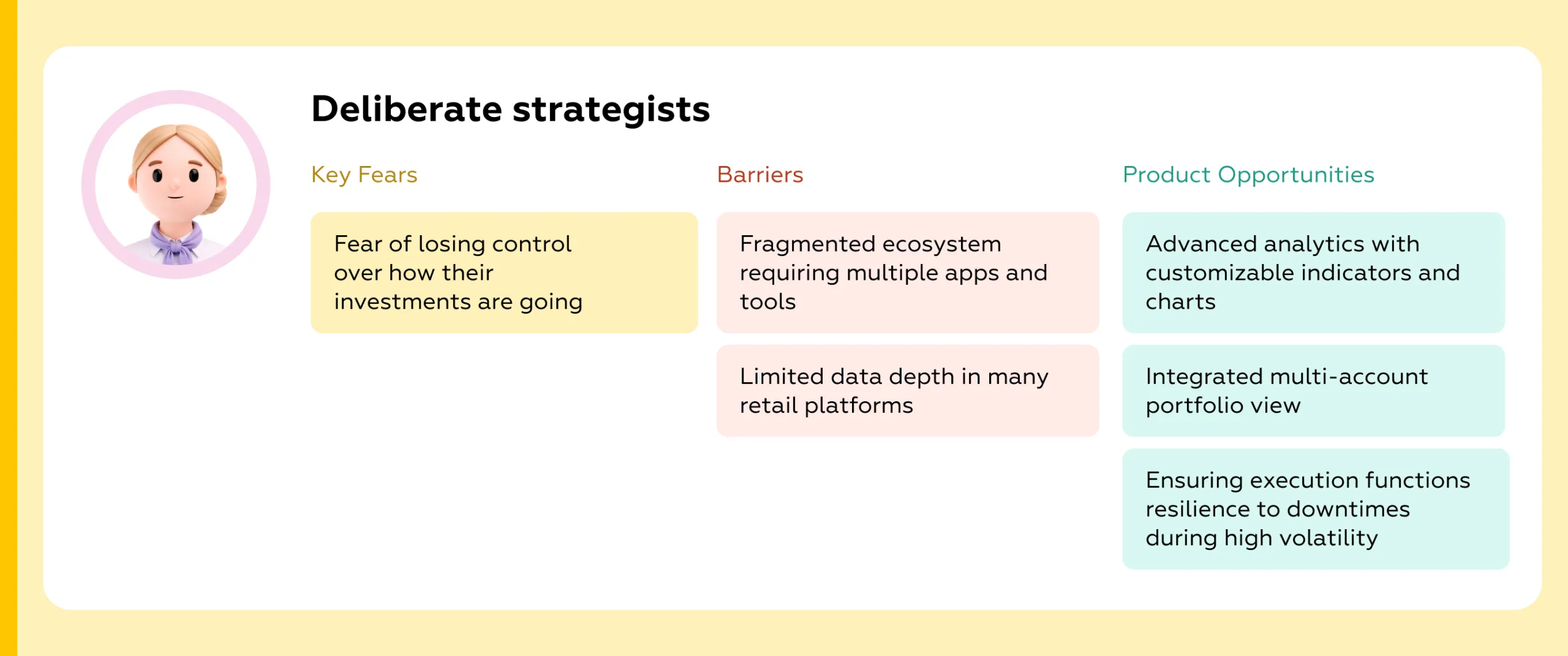

2. Deliberate Strategists Make thoughtful, well-informed decisions

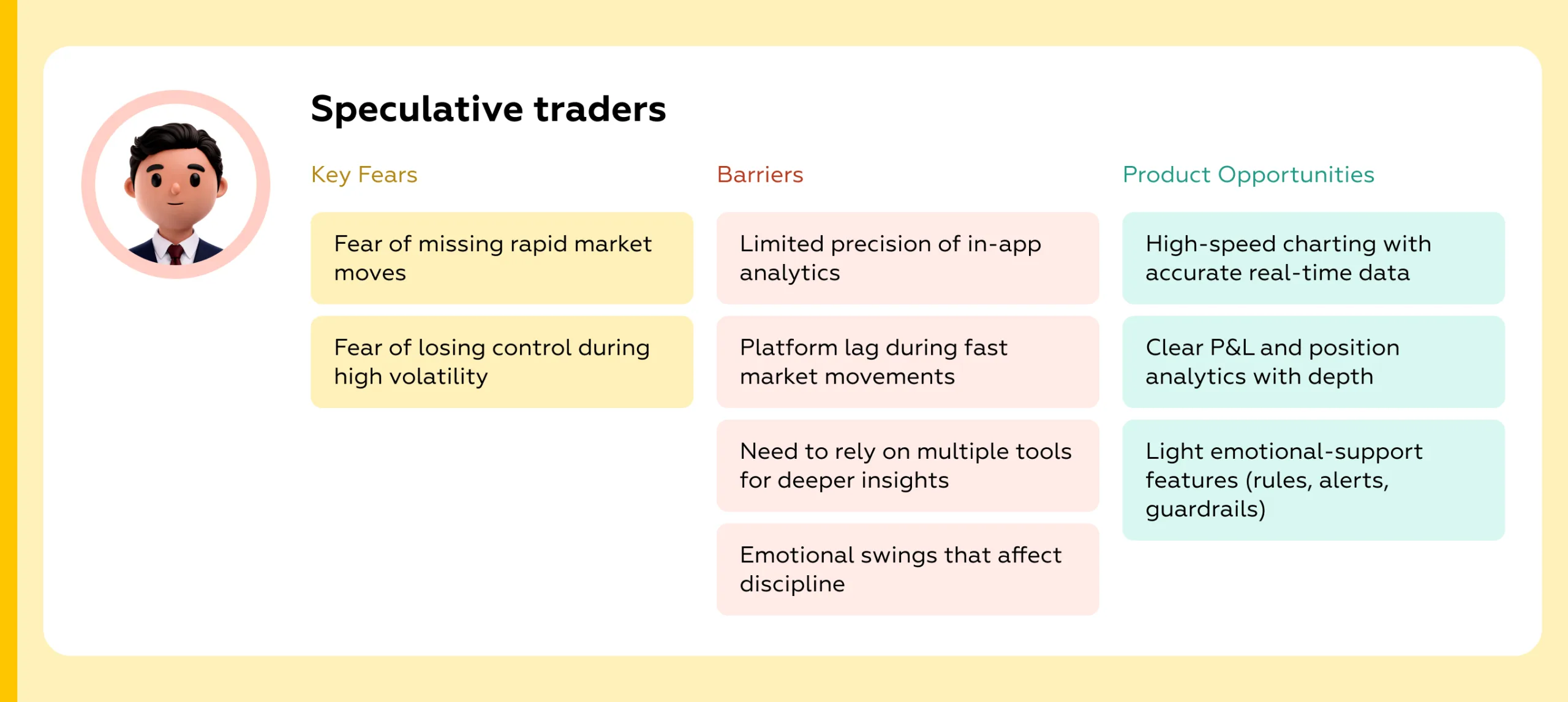

3. Speculative Traders Seek speed and flexibility to react quickly to the market

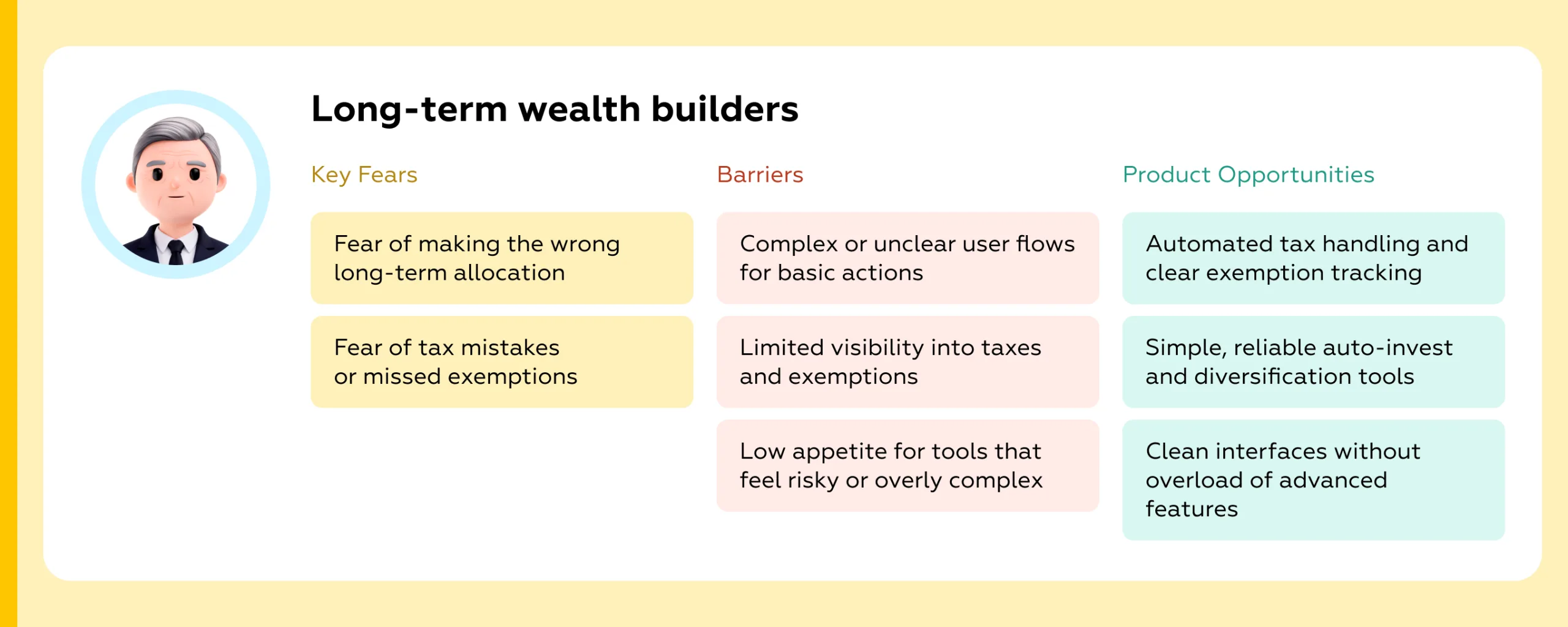

4. Long-term Wealth Builders Grow capital steadily with minimal stress

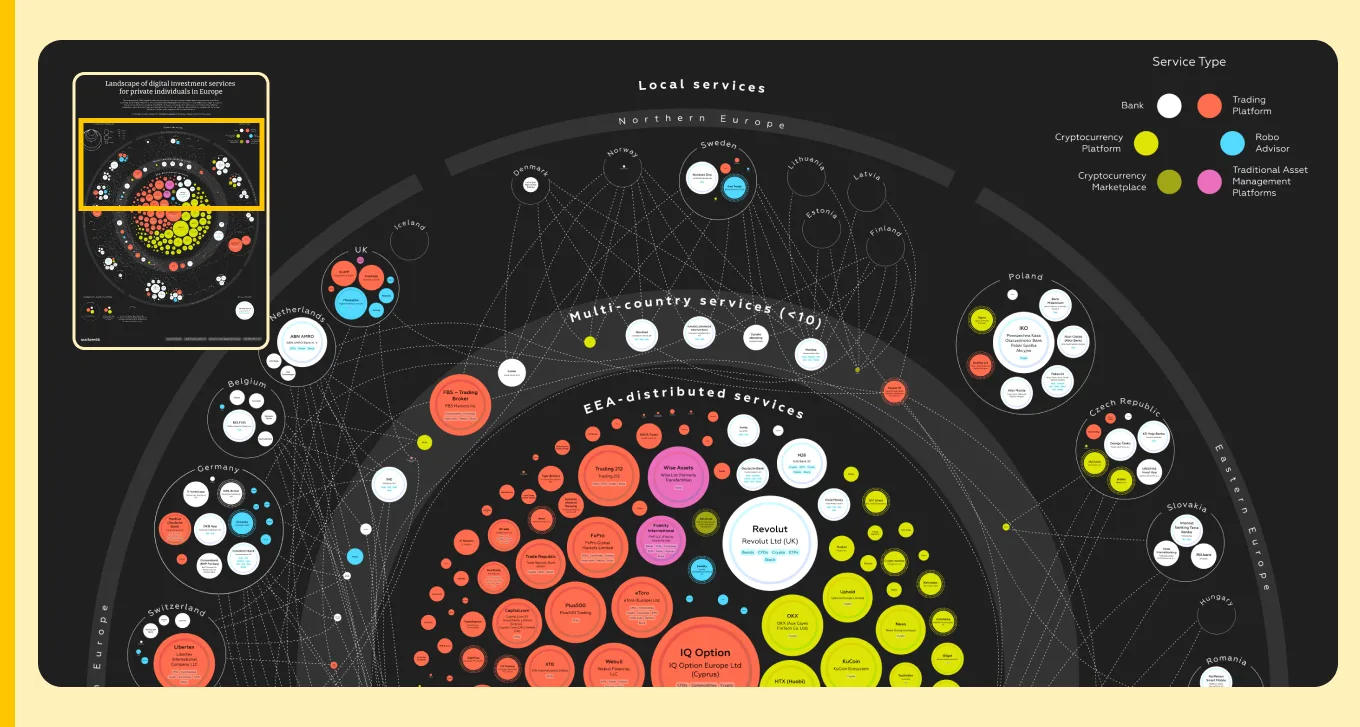

To understand how the European digital investment market is structured, Markswebb compiled a dataset of 316 investment services operating across Europe. The dataset covered each platform’s geographic presence, product architecture, market positioning, and functional capabilities. More details on the market map and the full structure of the dataset are available here.

This made it possible to compare services systematically and identify how investment platforms are distributed across markets, which models scale most effectively, and where the market is already saturated or still leaves room for growth.

The analysis showed that pan-European platforms are increasingly gaining an advantage over local players in scale and geographic coverage. However, local bank-led ecosystems still remain important in markets where investment behavior is more conservative and users rely more heavily on trusted financial institutions.

The most scalable models are usually linked to speculative and self-directed investing. Trading platforms, CFD services, and crypto platforms dominate the pan-European layer because they can expand across borders faster than traditional bank-led investment products.

The crypto ecosystem is especially cross-border by nature. It depends less on local banking infrastructure and more on digital distribution, mobile onboarding, and low-barrier access to assets.

At the same time, the market is moving toward hybrid financial ecosystems. Players such as Revolut and Trade Republic combine banking, investing, savings, and crypto in one environment. This creates a new competitive model where investment services are no longer isolated products, but part of a broader everyday financial platform.

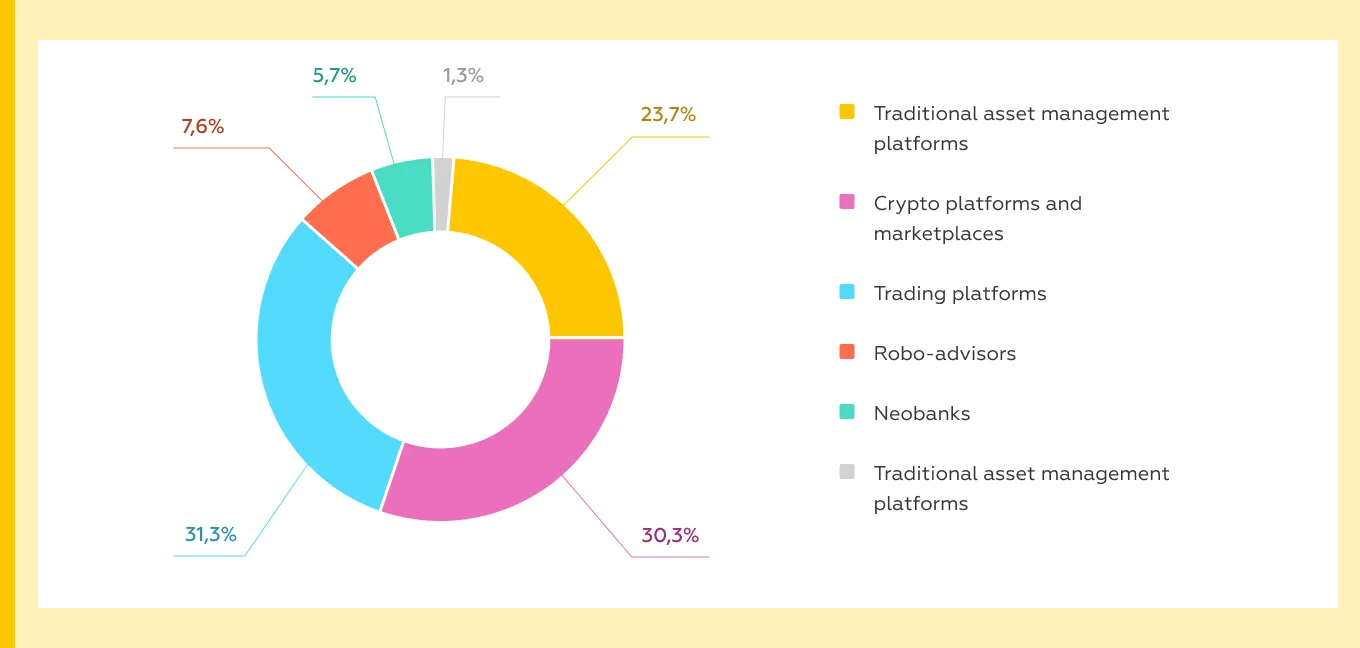

By provider type, the European digital investment market is structurally tripolar: banks, crypto platforms, and trading platforms form three comparable segments.

Banks remain the main providers of conservative long-term products, such as funds, ETFs, and bonds, but rarely move into highly volatile instruments. Crypto platforms are no longer a niche: by number of services, they now compete with banks and are especially strong in markets where ETF access and robo-advice are less developed. Trading platforms occupy the space between these two poles, serving active investors and speculative demand.

At the same time, robo-advisors and traditional digital asset-management services remain underrepresented, accounting for less than 10% and around 1.3% of platforms respectively. This points to a structural gap in Europe’s digital layer for long-term investing.

The supply side of the European digital investment market is strongly tilted toward short-term and high-volatility investing. Speculative trading platforms account for roughly 43% of all services — almost twice as many as conservative long-term investment platforms — and dominate across all European regions.

This means that Europe’s digital investment infrastructure is currently better developed for active trading than for patient, accumulation-driven investing. Users looking for fast market access, high-risk instruments, and speculative opportunities face a much broader choice than those focused on long-term wealth building.

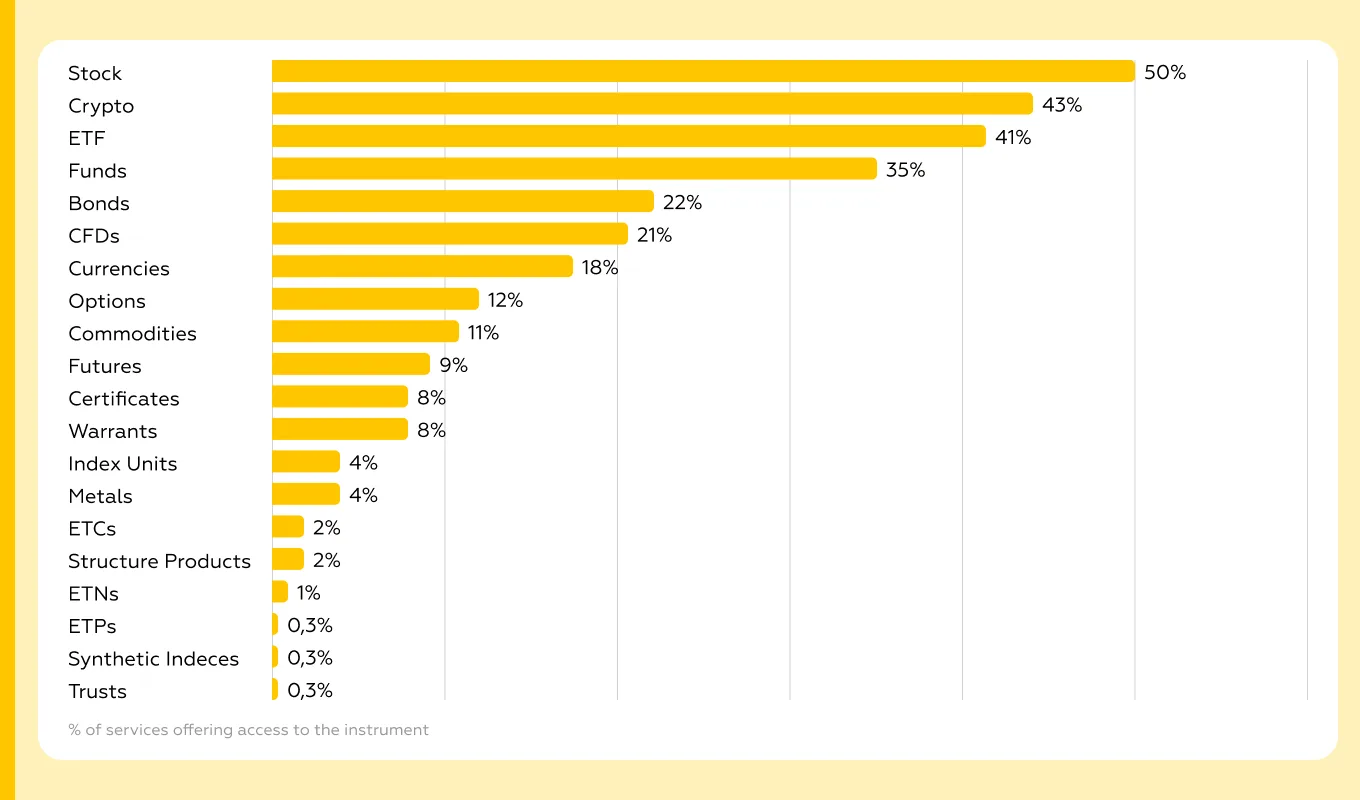

At the product level, the market has converged around a mainstream combination of stocks, ETFs, and crypto. More than half of platforms offer some version of this mix, making basic instrument variety a weak differentiator.

At the same time, investor behavior is more complex than most platform architectures. Interviews showed that users often combine ETFs, stocks, crypto, bonds, and sometimes real-estate exposure, but few services support these assets in one integrated environment.

This creates an opportunity for platforms that can offer true multi-asset portfolio support: unified portfolio views, cross-asset analytics, allocation guidance, risk visibility, and tools for managing both speculative and long-term investments in one place.

We compiled a dataset of 316 investment platforms operating across 32 European countries. It reflects the real structure of the digital investment landscape — from traditional banks to crypto platforms.

From this dataset, we selected 20 largest investment apps in Europe and assessed their UX using two evaluation systems: one for speculative investing and one for saving-oriented investing, reflecting the two major investment strategies.

This provides a clear benchmark of where your product stands, what competitors do better, and which improvements will drive the most impact.

Speculative trading platforms account for roughly 43% of all services — almost twice as many as conservative long-term investment platforms. They dominate across all European regions, with the strongest concentration in Western Europe. Mixed-strategy services are also present, but their share is lower than that of platforms built mainly around speculative investing.

This means that Europe’s digital investment infrastructure is currently better developed for trading than for patient, accumulation-driven investing. Users who want fast access to markets, active portfolio management, and high-risk instruments face a much broader choice of platforms than those focused on long-term wealth building.

At the product level, the market has largely converged around a mainstream combination of stocks, ETFs, and crypto. More than half of platforms offer some version of this instrument mix, which makes basic product variety a weak differentiator. Simply adding popular asset classes is no longer enough to stand out.

At the same time, there is a clear gap between investor behavior and platform architecture. Interviews showed that users often build mixed portfolios that combine ETFs, stocks, crypto, bonds, and sometimes real-estate exposure. However, platforms rarely support this full range of assets in one integrated environment.

This creates a significant opportunity for services that can move beyond fragmented access to individual instruments and offer true multi-asset portfolio support: unified portfolio views, cross-asset analytics, allocation guidance, risk visibility, and tools that help users manage both speculative and long-term investments in one place.

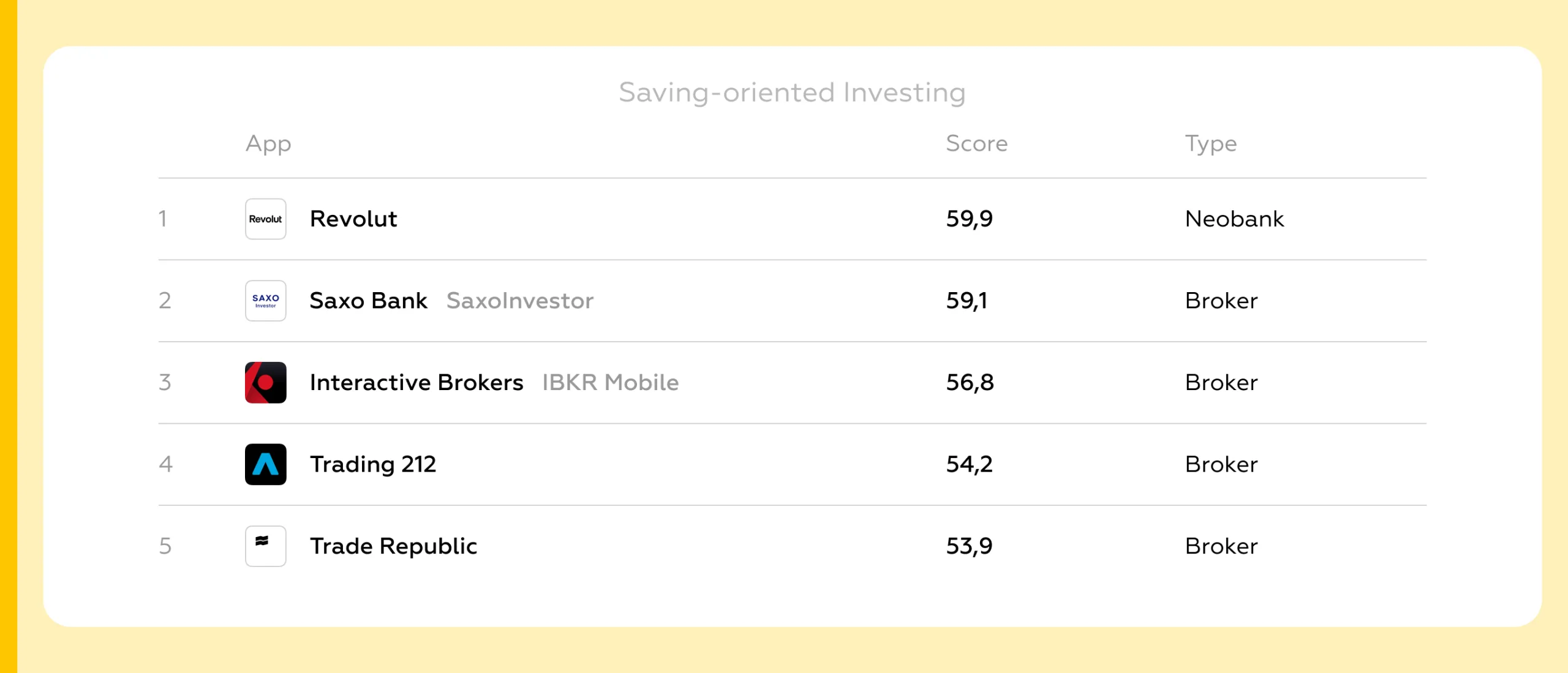

The leaders of the savings rating have developed basic capabilities

Key differentiators include complete cost transparency and sophisticated order management. Leaders also:

Top 5 European Savings Investment Services:

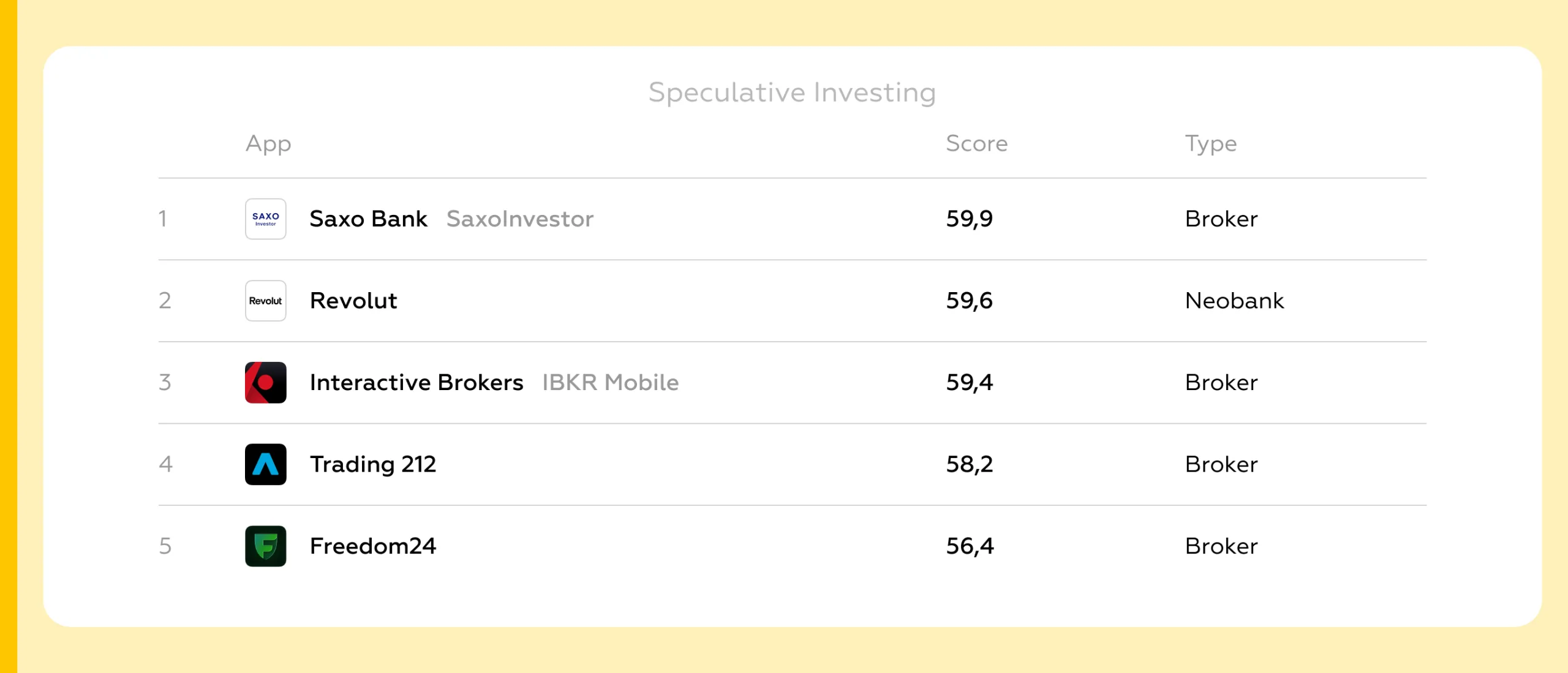

Leaders in the speculative segment provide complete cycle coverage

This group consists almost entirely of independent brokerage platforms, with only one exception.

These apps offer advanced investor calendars, specialized market news sections, and sophisticated analysis tools for both individual assets and the portfolio as a whole.

In addition, users have access to multidimensional portfolio structure analytics, enabling more informed decisions when rebalancing.

Also leaders:

Top 5 European Speculative Investment Services:

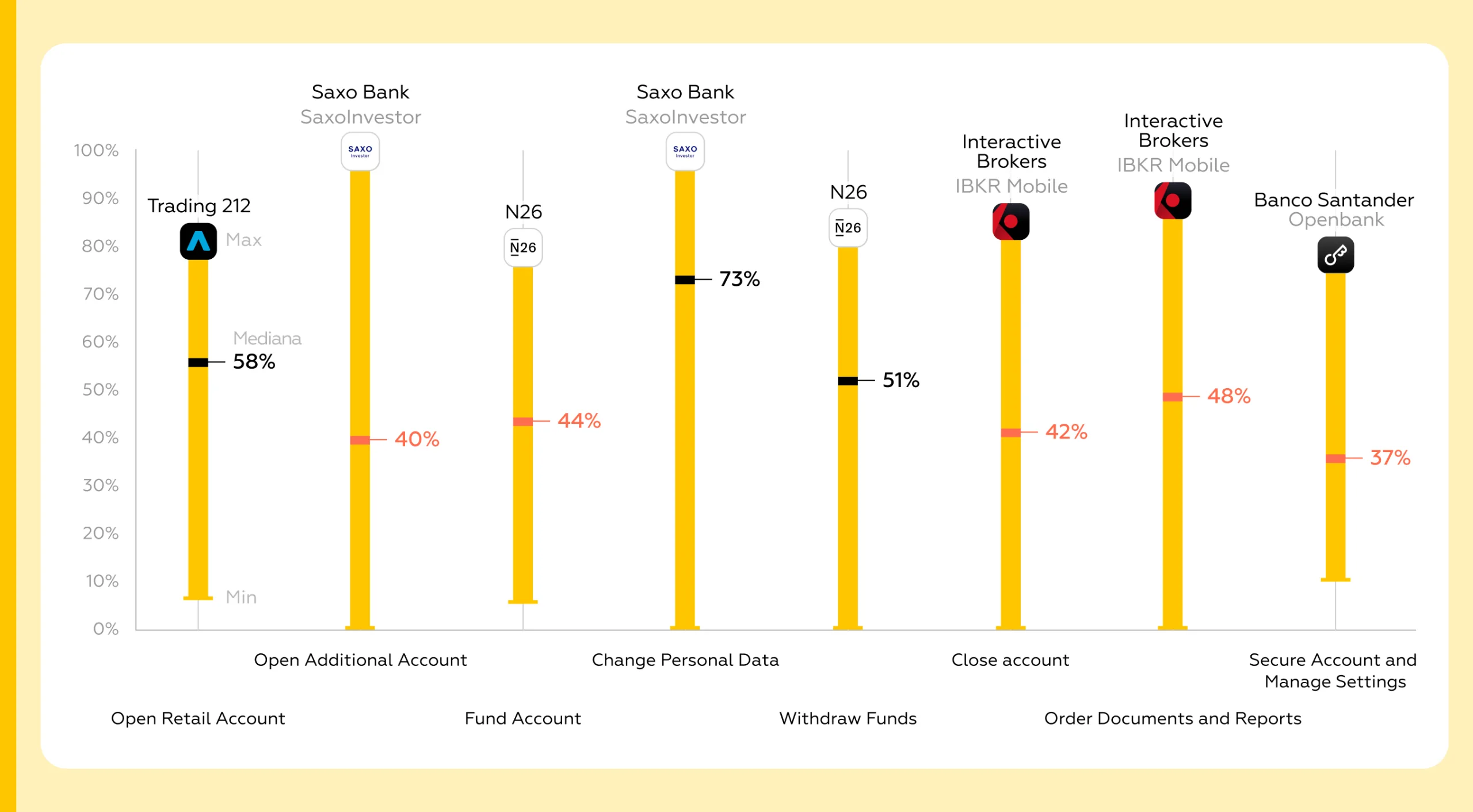

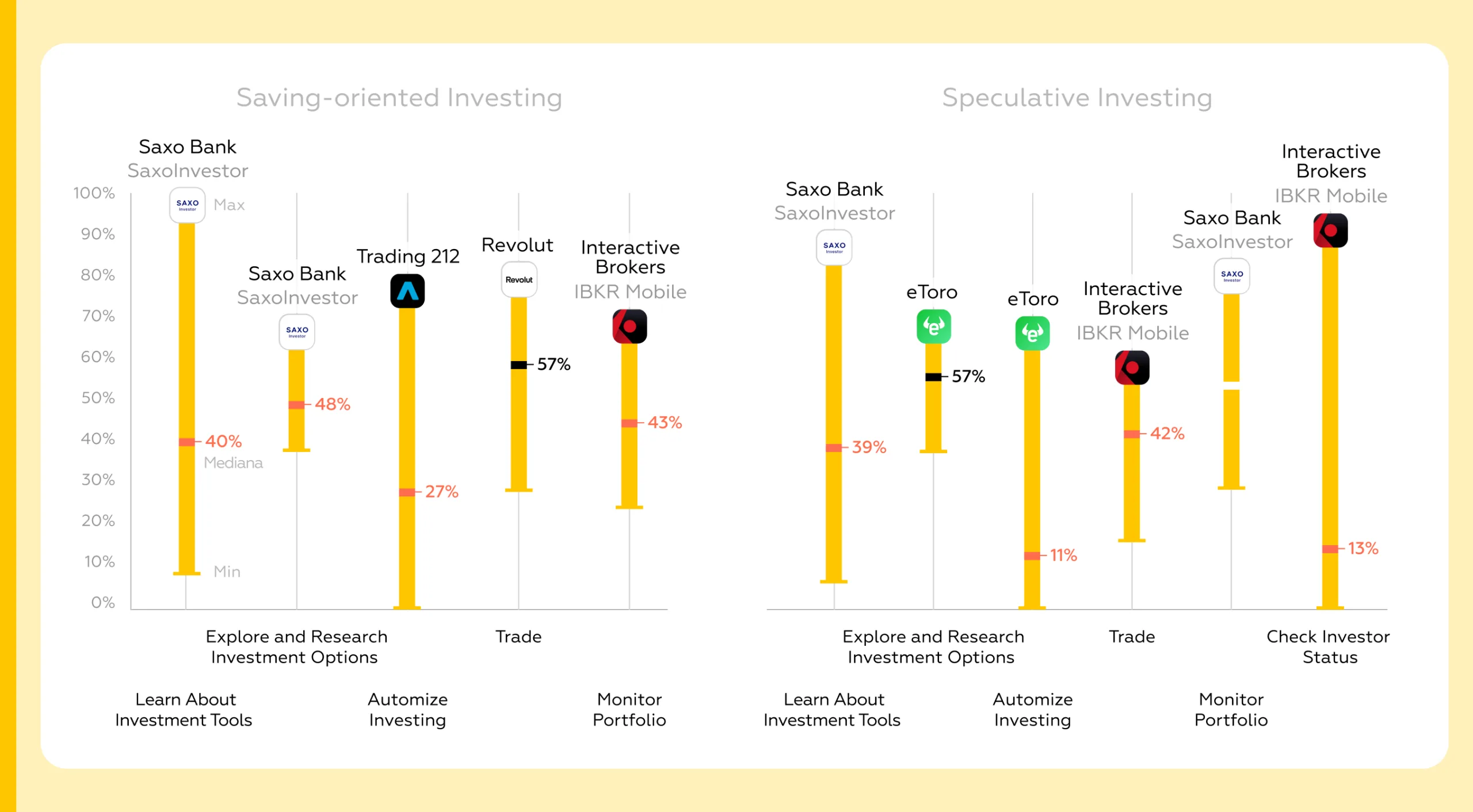

Across almost every core user task shared by both evaluation systems — regardless of whether the strategy is speculative or savings-oriented — we observe a wide variation in user experience, ranging from 0 to 100.

This variability highlights a lack of consistency across the market and the absence of a stable baseline experience.

Services rarely reuse best practices, and even fundamental processes — such as account opening or withdrawals — differ significantly between platforms or may be missing entirely within the app.

Tasks related to discovering and researching investment instruments, executing trades, and monitoring portfolios show relatively high minimum scores across both evaluation systems.

However, almost no platform exceeds the 80% level, while the median remains around 50%.

The market effectively solves core tasks, but overall development has reached a plateau. There are no services that can be considered a benchmark in analytics, trade execution, or portfolio management.

The State of Digital Investment in Europe study helps you quickly identify growth opportunities, shorten R&D cycles, and make informed decisions based on real data from the European investment market.

The public results in this report are only a small part of the insights we gathered during our research.

The full report provides:

For product teams, this offers the opportunity to act faster and more accurately, shorten the R&D cycle and accelerate the launch of new competitive offerings.

To explore European investor profiles across different strategies, get a comparative analysis of investment services by user task blocks, and adopt the best practices from the market.

Markswebb studied the European digital investment market in five stages: mapping the market, reviewing statistical data, interviewing retail investors, auditing investment apps, and analyzing the results.

We combined several types of research: open market data, interviews with investors, and a detailed review of how major investment services work in practice.

The study builds on Markswebb’s proprietary evaluation framework and long-term expertise in digital service research. The research measures digital experience not through opinions or surface-level feature comparisons, but through the actual ability of services to support investor decisions, reduce friction, and help users complete key tasks.

Markswebb experts and analysts identified 316 platforms operating in 32 countries, including banks with investment functionality, brokerage apps, neobrokers, robo-advisors, crypto platforms, and other services that allow users to invest digitally.

We then used this database to examine how the market is structured in different parts of Europe. The analysis showed which service models are most common in each country, how investment products vary by region, and where competition is already intense versus markets that still offer space for growth.

This stage created the foundation for identifying the main service categories, regional differences, and growth opportunities in the European investment market.

To understand the demand side of the market, we reviewed open statistical sources on European retail investors. The analysis focused on how investor profiles differ across countries and regions in terms of age structure, risk attitudes, institutional trust, access to financial instruments, and preferred investment formats.

We also analyzed how the mix of instruments varies by country, including the role of shares, funds, bonds, savings products, crypto assets, and other investment options. This helped us understand which markets are more focused on long-term wealth accumulation, where speculative behavior is more visible, and how local regulation, digital maturity, and financial habits shape investor needs.

Markswebb researchers conducted 32 in-depth interviews with retail investors from Germany, Spain, Poland, and Sweden. These countries were selected to capture different European investor contexts and compare behavioral patterns across mature, mobile-first, conservative, and more actively trading markets.

Participants were segmented by investment behavior and portfolio size. The sample included savings-oriented investors, speculative investors, and balanced investors, with portfolio ranges from €5–10K to €50K+.

The interviews helped us understand how users choose investment services, what tasks they perform most often, which barriers prevent deeper product adoption, and what they expect from digital investment platforms. These insights informed the structure of the two UX evaluation systems used in the audit.

For the in-depth benchmark, Markswebb selected 20 major European investment services using strict criteria: international coverage, real-asset dealing, large retail reach, and mobile availability. The research is based on Markswebb’s proprietary evaluation system, which uses binary criteria to assess whether a service supports a specific user task or not. This approach allows us to calculate an independent digital experience score from 0 to 100 points both for individual user scenarios and for the overall quality of a digital investment service.

Researchers accessed each app as retail users and completed scenario walk-throughs across two evaluation systems: one for savings-oriented investing and one for speculative investing.

The savings-oriented investing checklist included 361 criteria. It focused on scenarios related to long-term and regular investment behavior.

The speculative investing checklist included 341 criteria. It covered scenarios typical for active trading behavior.

All findings were documented with screenshots and screencasts.

After the audit, checklist results were processed to calculate two platform ratings.

The scoring system reflects how well each service supports user tasks across different investment strategies. Criteria were grouped by task category and weighted according to the importance of each scenario for a specific investor behavior model.

At this stage, audit results were also interpreted together with insights from investor interviews. This helped connect measurable UX gaps with real user expectations, behavioral patterns, and barriers to deeper product adoption.

Based on the audit data, Markswebb identified common UX problems, documented best practices, and assessed how well key user tasks are supported across the market. The final analysis shows where services already meet user expectations, where they lose users in critical scenarios, and which product improvements can create growth opportunities.

We’ve evolved dozens of successful financial services and are eager to prove that our expertise can be implemented in other industries and around the world. Have a look at our success stories!

From research and analysis to strategy and design, we help our clients successfully reach their customers through digital services.