Mobile banking apps has firmly become the default way people interact with their finances. In 2025, global mobile banking adoption continued to grow, with downloads increasing by around 5% year-over-year, reflecting sustained expansion of mobile-first financial behavior. As adoption saturates, competition is no longer about features — it’s about UX quality, clarity, and trust.

These shifts are shaping the key mobile banking apps trends for 2026, as leading banks move from static tools to intelligent financial platforms that guide users, automate decisions, and reduce cognitive load. This transition marks a fundamental change: banking apps are no longer just interfaces for transactions, but active participants in users’ financial lives.

Contents

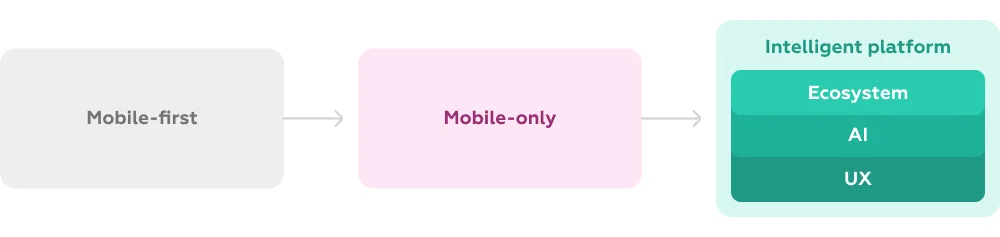

Mobile banking is entering a new phase of maturity. What was once a “mobile-first” strategy is rapidly evolving into mobile-only, as users increasingly abandon desktop channels and expect the full banking experience to be seamless on smartphones. In many markets, over 70% of interactions already happen via mobile, pushing banks to prioritize app performance, reliability, and simplicity above all.

At the same time, UX has become the key differentiator. Feature parity across banks is largely achieved, making usability, clarity, and speed the main drivers of customer satisfaction and retention. Poor UX now directly translates into churn, while intuitive flows and reduced cognitive load increase engagement and trust.

Finally, AI and ecosystem integration are reshaping the experience itself. Banking apps are moving beyond transactions toward proactive financial guidance — embedding budgeting, recommendations, and third-party services into a single interface. This shift reflects a broader transition from standalone tools to connected financial ecosystems powered by intelligent automation.

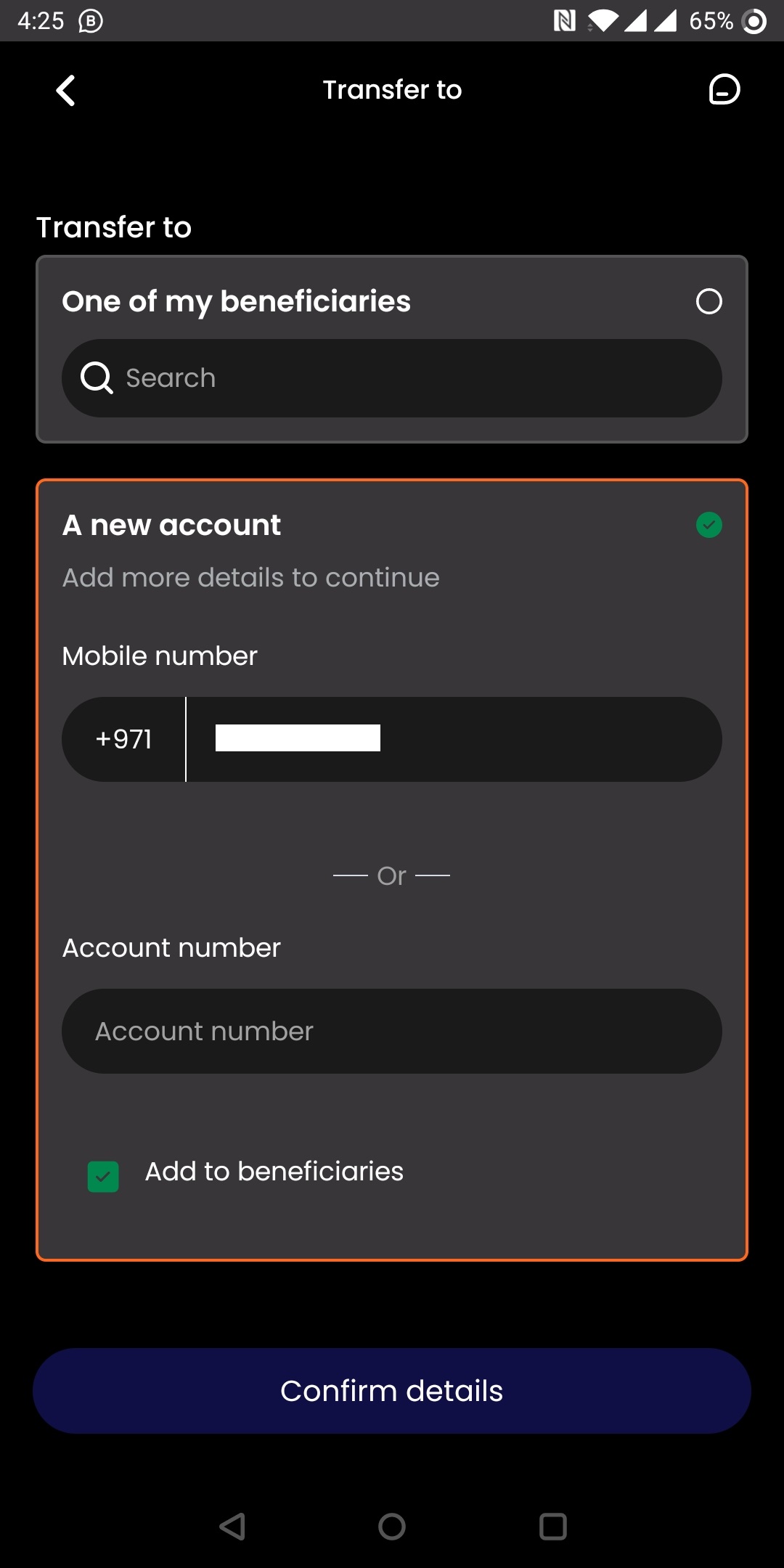

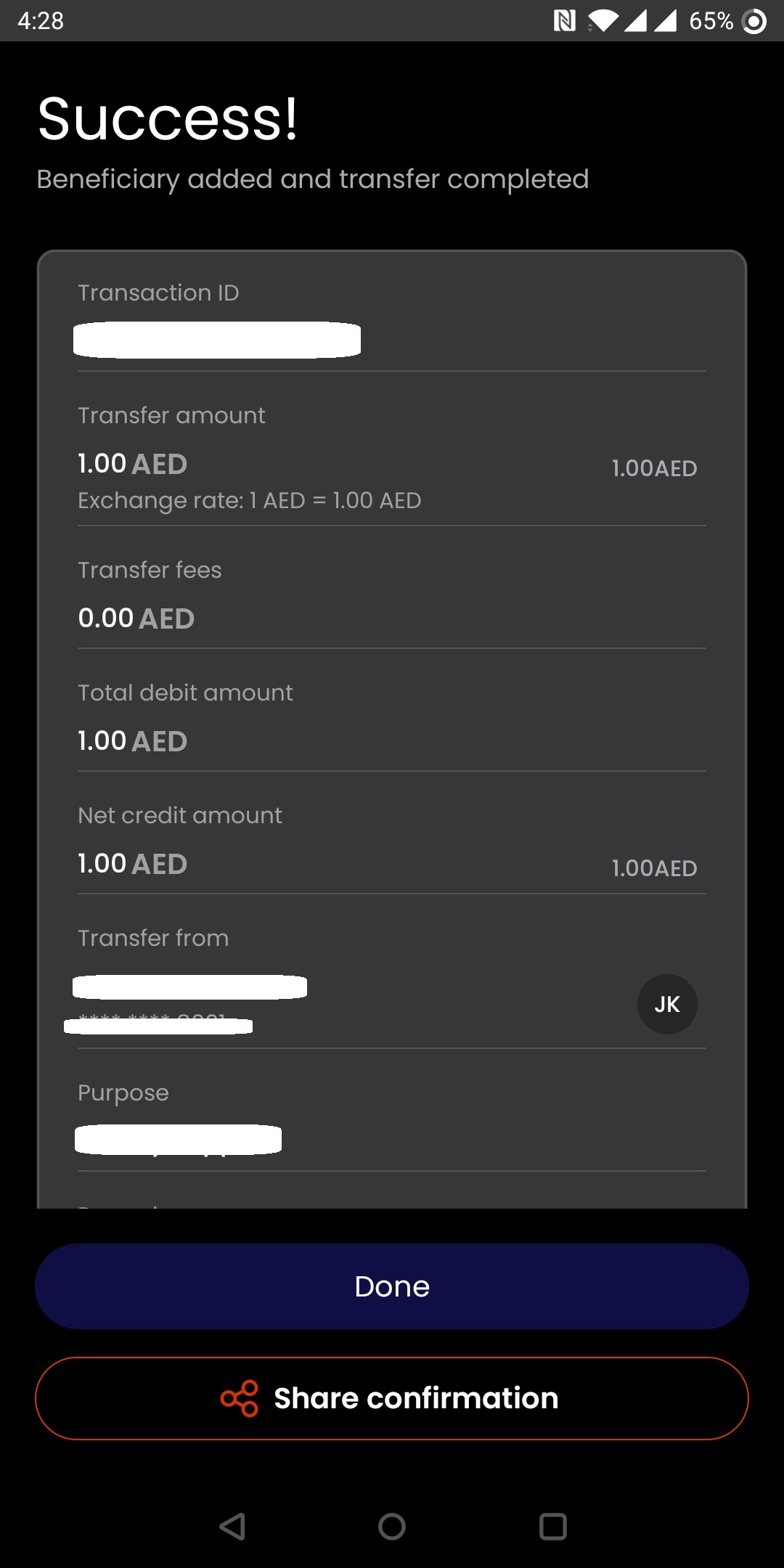

Problem:

In ADCB, adding a beneficiary for a simple intra-bank transfer requires entering the recipient’s full address — a detail users often don’t have readily available. This creates a critical blocker in time-sensitive scenarios, such as paying rent at the last minute. Instead of completing the task quickly, users are forced to pause the flow, search for missing information, or contact the recipient — increasing stress, delays, and the risk of failed payments.

Solution:

Leading banks reduce friction by designing flows around the actual transfer scenario, minimizing required data and providing fallback options when users lack certain information. Instead of rigid forms, they enable flexible identification methods and ensure that users can always complete the task — even under constraints.

Example:

Al Hilal Bank embeds beneficiary creation directly into the transfer flow and allows users to add a recipient using only a mobile number. This aligns with the real-life scenario where users often only have a phone contact. At the same time, the system keeps an alternative option to add a beneficiary via account number.

Problem:

WIO clients want to know exactly what their monthly subscription includes. Following standard expectations, they naturally check their account/card details or profile, but the app hides this essential information in Settings → Subscription details. This disconnect from users’ mental models creates search friction, often leaving them unable to find the details. Users either abandon their inquiry or contact support, which increases operational costs and erodes trust in the platform’s transparency.

Solution:

Top-performing apps treat transparency as a UX principle by surfacing critical information where users expect it, explaining service terms clearly, and enabling quick comparisons. This reduces uncertainty, empowers informed decisions, and strengthens trust.

Example:

Vivid Money displays the current plan directly in the user profile and allows users to access a carousel of all available plans via “Upgrade your plan” or “Plans.” Users can instantly compare features and manage subscriptions without leaving the context of their profile, creating a seamless, transparent experience that minimizes friction and support requests.

Problem:

Users often rely on support or additional steps to understand available financial options, check eligibility, or proceed with products like loans — creating friction and slowing down decision-making.

Solution:

Banks shift to self-service by embedding ready-to-use scenarios directly into the app: users see pre-approved options, clear conditions, and can act immediately without external help. This reduces effort and accelerates decisions, aligning with engagement-driven UX patterns highlighted in Markswebb’s research.

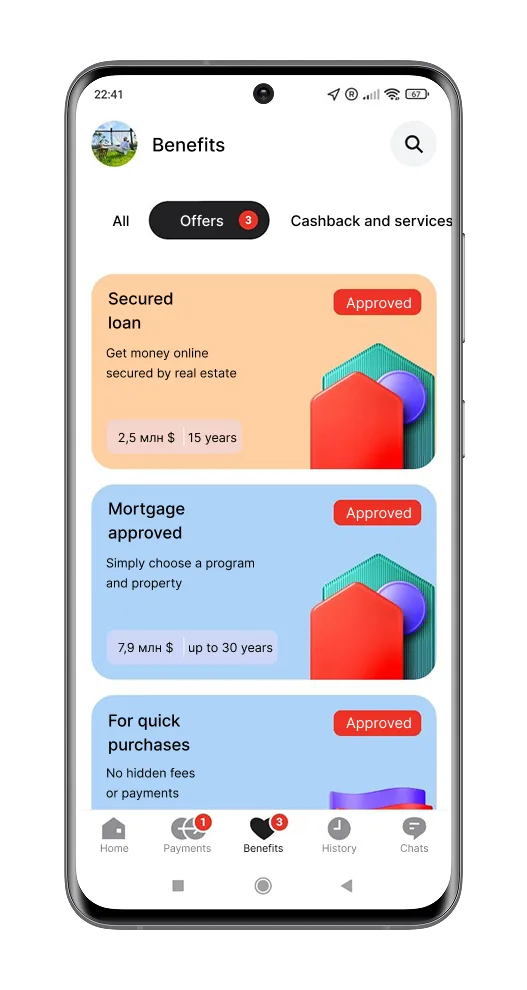

Example:

In the shown app from an Eastern European bank, financial products are presented as pre-approved offers with a visible status (“Approved”), key terms (amount, duration), and concise descriptions directly on the main screen. Users can instantly evaluate and select an option without contacting support, turning the app into a self-service decision environment.

Problem:

Traditional banking apps rely on static interfaces and predefined flows, requiring users to navigate menus, interpret financial data, and search for relevant information themselves. This limits engagement and creates friction, especially when users need guidance or have complex questions.

Solution:

AI — particularly large language models (LLMs) — enables conversational, context-aware financial guidance. Instead of navigating interfaces, users can express intent in natural language and receive personalized, adaptive responses. These systems can explain products, compare options, and guide decisions in real time, transforming the app from a passive tool into an interactive financial assistant.

Example:

Several banks are already integrating LLM-powered assistants into their apps, allowing chatbots to move beyond scripted replies toward multi-turn, human-like conversations. These assistants can explain financial products in simple terms, adapt tone to the user, and help choose between options (e.g. account types or plans), providing scalable and personalized guidance directly within the interface — an approach highlighted in Markswebb’s research on AI-driven personalization in digital banking.

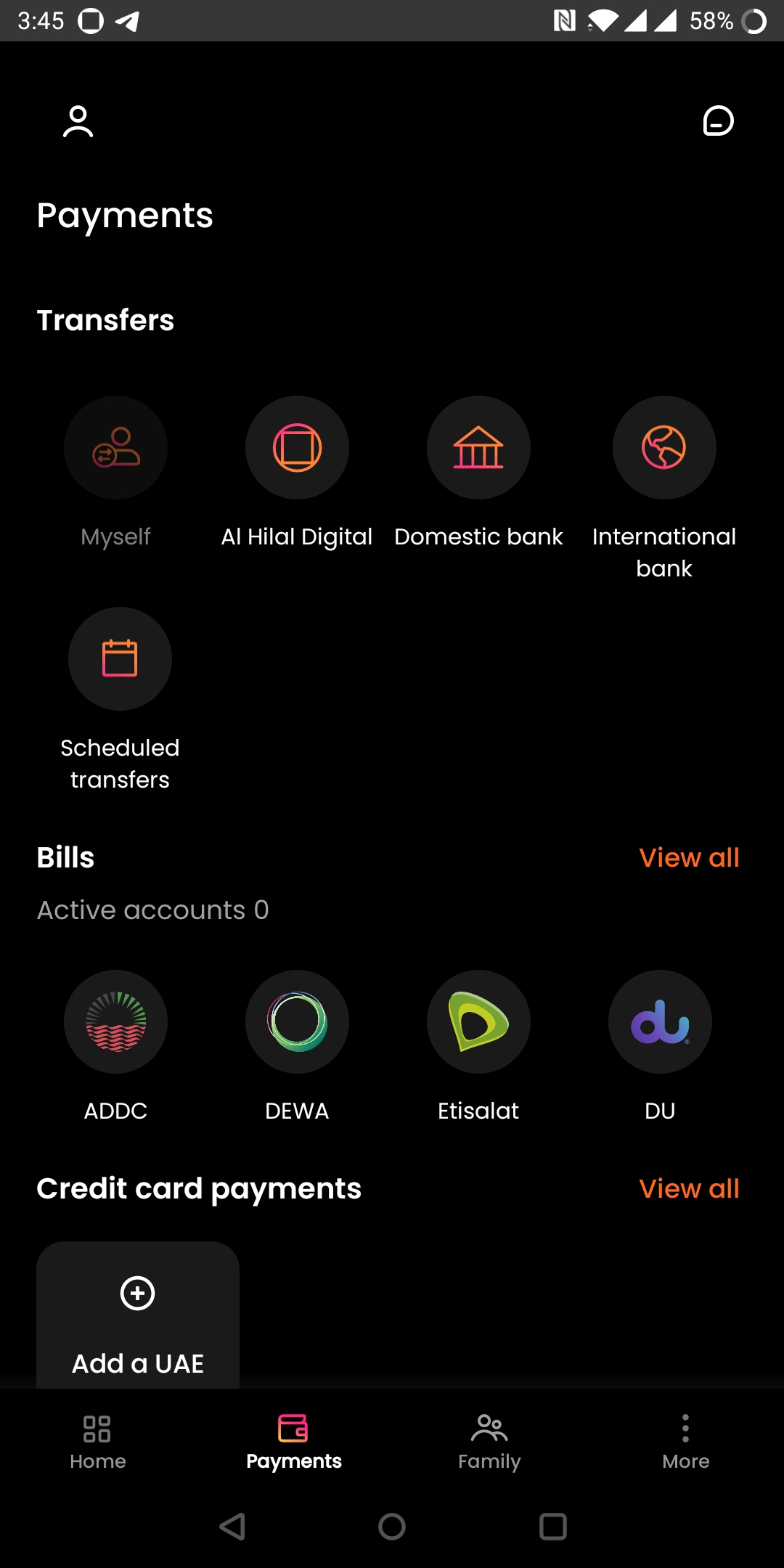

Problem:

In many banking apps, payments and related actions are still separated into dedicated sections. Users have to leave their current context, navigate to a “Payments” area, and reselect the scenario — breaking the flow and increasing friction, especially for frequent, routine tasks.

Solution:

Financial ecosystems evolve toward contextual, embedded experiences, where core actions like payments are integrated directly into the user’s primary task. Instead of navigating to a function, users complete actions where the intent naturally arises. This approach reflects the broader shift toward super apps, where multiple services are interconnected and workflows remain continuous—an idea also explored in Markswebb’s research on invisible finance

Example:

In the shown app from a European bank, payments are embedded into the property management scenario. Users can view expenses (utilities, services) and initiate payments directly within the same screen, without switching to a separate payment flow. This creates a seamless experience where the action happens in context, illustrating how ecosystem thinking transforms isolated features into continuous user journeys.

Problem:

Feature-heavy navigation makes it difficult for users to find what they need. Menus, tabs, and complex hierarchies increase time-to-task and cognitive load.

Solution:

Conversational interfaces — chat, voice, and AI copilots — shift interaction from navigation to intent-based actions. Users simply express what they want, and the system executes it.

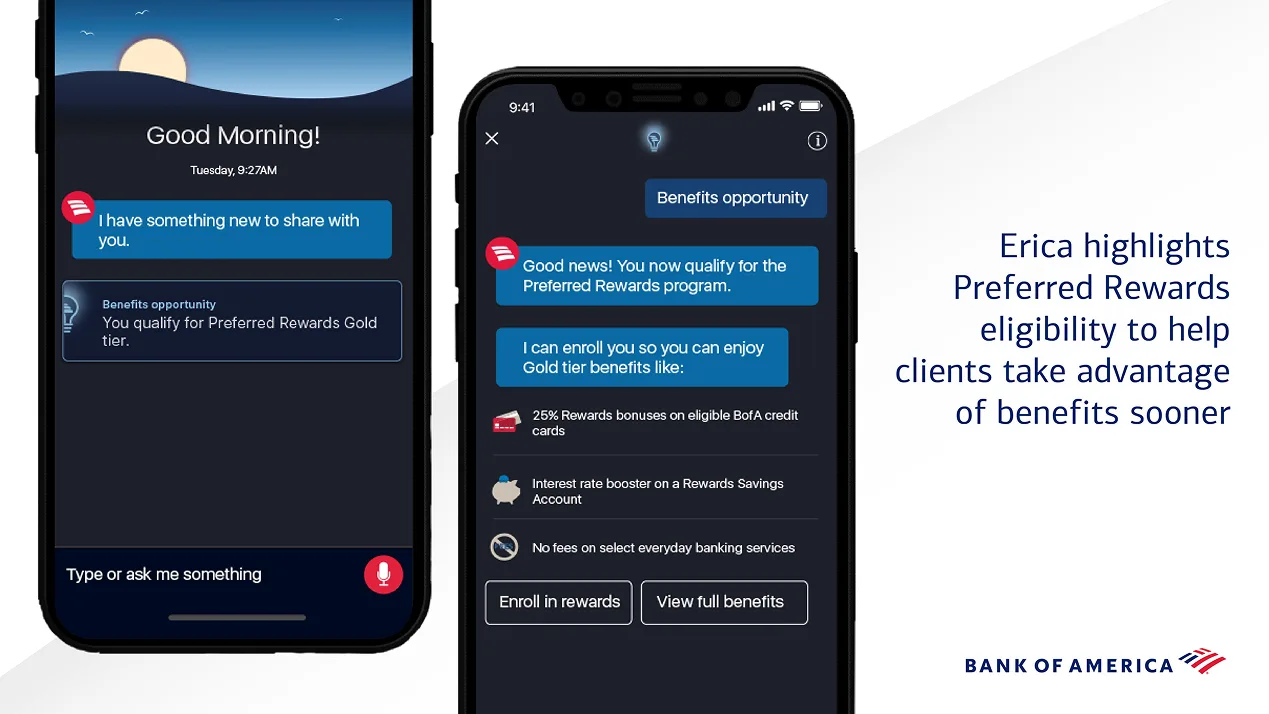

Example:

Bank of America Mobile Banking integrates the virtual assistant Erica, allowing users to check balances, track spending, and perform actions through natural language — reducing reliance on traditional UI navigation.

The evolution of mobile banking — from functional apps to intelligent financial platforms — fundamentally changes how banks compete. The winners in 2026 will not be those with the most features, but those who design better decisions, reduce friction, and build trust at scale.

UX is no longer a supporting function — it directly shapes financial performance. Every interaction inside the app influences whether a user completes a task, adopts a product, or abandons the flow.

Banks are increasingly measuring UX in business terms:

Well-designed flows don’t just “feel better”— they increase conversion, reduce operational costs, and unlock new revenue streams. In this context, UX moves from interface design to growth infrastructure.

In digital banking, trust is no longer built through brand perception alone — it is continuously validated through the interface.

Every unclear fee, delayed status update, or ambiguous message introduces friction and doubt. Over time, these micro-frictions accumulate into churn. On the other hand, apps that clearly communicate what is happening — before, during, and after each action — create a sense of control.

This shifts trust from an abstract concept to something tangible:

Banks that design for transparency don’t just improve UX — they increase retention, reduce support, and strengthen long-term relationships.

As user expectations are shaped by leading tech products, banking can no longer rely on slow release cycles and rigid systems. The ability to iterate quickly becomes a strategic advantage.

This includes:

In this model, the banking app is not a finished product but a constantly evolving system. Organizations that can ship, measure, and improve faster are better positioned to capture emerging needs and outpace competitors.

Traditional banking was episodic: users opened the app to complete a task and left. The new model is continuous—driven by insights, alerts, and integrated services.

Instead of waiting for user actions, apps now:

This increases frequency of interaction and transforms the app into a daily financial companion, not just a transactional tool.

Perhaps the most important shift is conceptual. Banking apps are no longer just interfaces—they are becoming decision-making systems.

AI enables apps to:

As a result, the role of UX expands: it is no longer only about navigation and layout, but about how the system thinks, guides, and acts on behalf of the user.

Ultimately, these trends signal a shift from digital banking as a service to digital banking as an experience.

Banks that embrace this shift will compete not on features, but on how effectively they help users manage their financial lives.

Adapting to the next wave of mobile banking requires a shift in how products are designed, built, and evolved. Incremental improvements are no longer enough—banks need to rethink the structure of their apps around user outcomes, not internal logic.

The first step is moving from feature-based thinking to journey-based design. Instead of optimizing isolated screens, teams should focus on complete user scenarios—what the user is trying to achieve from start to finish. This means reducing fragmentation, eliminating unnecessary steps, and ensuring that each flow leads to a clear, predictable result. In practice, it requires cross-functional alignment: product, UX, and technology working around shared journey metrics rather than individual features.

At the same time, meaningful differentiation increasingly depends on data and AI capabilities. Banking apps already collect vast amounts of behavioral and transactional data, but the competitive advantage comes from how effectively this data is used. Personalization, timely recommendations, and automation are not standalone features —they are the result of a well-integrated data layer combined with intelligent models. Banks that invest in this foundation can move from reactive interfaces to systems that anticipate user needs and reduce decision effort.

Equally important is the need to redesign UX around control and trust. As apps become more proactive and automated, users must feel confident in what the system is doing. This requires clear communication, transparent logic, and consistent feedback at every step. Users should always understand what will happen before they act, and what has happened after. In this context, trust is not an abstract value—it is built through hundreds of small, well-designed interactions.

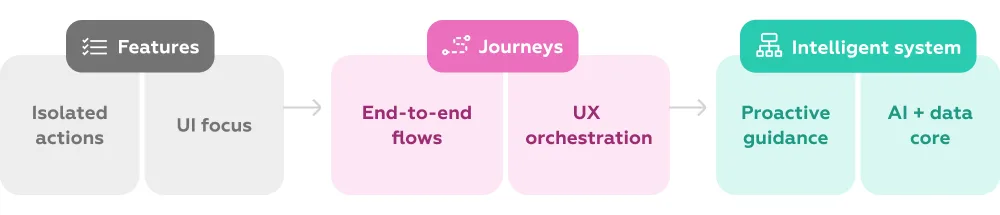

To bring these elements together, mobile banking strategy can be seen as a transition from fragmented functionality to an integrated, intelligent system:

This shift defines how banks will design, prioritize, and scale their products in the coming years. Those who align UX, data, and trust into a single system will be better positioned to deliver consistent value—and to adapt as user expectations continue to evolve.

Mobile banking is no longer just a digital channel—it is becoming the core financial platform where users manage, understand, and act on their money. As this shift accelerates, the role of UX expands from interface design to shaping the entire experience of financial decision-making.

What increasingly separates market leaders is not the number of features, but the maturity of their UX: how well they structure journeys, communicate clearly, and reduce user effort. At the same time, the gap between leaders and laggards continues to widen. While some banks evolve into intelligent, adaptive systems, others remain fragmented and reactive—creating a noticeable difference in user trust, engagement, and retention.

What are the latest mobile banking trends?

The key trends include scenario-based UX, transparency as a core principle, self-service models, AI-driven personalization, ecosystem expansion, and the rise of conversational interfaces. Together, they reflect a shift from transactional apps to intelligent financial platforms.

How AI is used in mobile banking apps?

AI is used to analyze user behavior, categorize transactions, provide spending insights, and deliver personalized recommendations. More advanced implementations include proactive alerts, automated actions, and conversational assistants that help users manage finances with less effort.

What makes a good banking app UX?

A strong banking UX is defined by clarity, predictability, and efficiency. Users should be able to complete key tasks quickly, understand what is happening at every step, and feel confident in the outcome. This includes intuitive navigation, transparent communication, and seamless end-to-end journeys that minimize cognitive load.

What is a financial super app?

A financial super app is a platform that combines multiple financial and related services—such as payments, transfers, savings, investments, and even lifestyle features—within a single interface. Instead of switching between apps, users can manage most of their financial activities in one place, increasing convenience and enabling more frequent, everyday engagement.

We respond to all messages as soon as possible.

We’ve evolved dozens of successful financial services and are eager to prove that our expertise can be implemented in other industries and around the world. Have a look at our success stories!