Know first!

Subscribe to our newsletter

For customers today, a mobile bank is not merely a digital convenience — it is the primary gateway to financial management. Mobile banking delivers everyday banking tasks such as transfers, payments, account insights, and financial planning directly in users’ hands. Yet even as core functionality becomes widespread across providers, the quality of digital experience remains a key differentiator in a mature market where competition is shifting from feature quantity to how seamlessly services integrate into users’ everyday lives.

In the 2025 wave of Markswebb’s Mobile Banking Rank research, we see that mobile banking is no longer just a channel for isolated transactions; it is evolving into a lifecycle service that supports users through multiple phases of financial decision-making — from onboarding and money management to long-term planning. This shift challenges banks to offer experiences that go beyond mere availability of features and instead deliver clarity, ease, and relevance in every interaction.

However, despite this strategic importance, many digital experiences still show inconsistencies in usability, transparency, or depth — suggesting that even leaders have room to grow in meeting rising customer expectations and reducing friction across key flows such as payments, onboarding, and account servicing.

In this study, all mobile banking experiences are compared using Markswebb’s proprietary evaluation system — a structured, rigorous framework designed to turn UX data into actionable insights. Rather than relying on subjective impressions or isolated opinions, this system evaluates digital experience through a consistent set of measurable criteria:

The system consists of hundreds of criteria that describe both what customers can do in the digital service and how well they can do it — in other words, both functional capabilities and the interface qualities that shape real user experience. This creates a single frame of reference for direct, objective comparison across services. By design, the system minimizes subjectivity because all criteria are binary (met / not met), ensuring consistency across evaluations.

For Mobile Banking Rank 2025, the evaluation system includes approximately 900 criteria across two key dimensions:

In practice, the system functions as a comprehensive checklist used for an expert desk-based review: researchers model real customer scenarios and evaluate each criterion against actual service behavior. These expert assessments are complemented by moderated usability tests with target users to integrate real behavioral insights into the scoring.

This year’s research also incorporated a series of expert interviews with mobile banking product leaders, amplifying our understanding of platform constraints, team challenges, and emerging trends in digital banking experience.

The evaluation output is a detailed matrix listing hundreds of parameters that show where services provide full support and where functional or usability gaps remain. Because the dataset is extensive and multifaceted, Markswebb analysts perform deep interpretation and synthesis — forming the backbone of the full research report.

Each web version receives a score calculated as the sum of met criteria multiplied by their respective weights. Final scores reflect not only what capabilities are present but also how effectively and efficiently customers can complete tasks — a direct measure of real-world digital experience quality.

This approach transforms UX evaluation into a strategic management tool. Banks can not only identify where their services lag but also understand why customers abandon key flows and which improvements will deliver the greatest impact on engagement, retention, and revenue.

The strength of our system lies in its ability to replace assumptions with evidence. Instead of relying on personal opinions or isolated feedback, banks receive results grounded in a consistent and measurable framework — highlighting both short-term quick wins and long-term development priorities.

Using a standardized evaluation system turns a UX audit or benchmark into actionable work. We assess every step of the customer journey — onboarding, daily payments, transfers, deposits, support — using the same criteria as Mobile Banking Rank 2025, enabling true comparability across scenarios and over time. You get a clear map of where your service meets user expectations, where friction occurs, and a prioritized list of fixes ranked by impact and effort, anchored to real UI/UX best practices.

For competitive analysis, the same system shows exactly how you rank against peers in each flow — revealing what to adopt, what to redesign, and where to create new value. Outputs include scorecards, risk/opportunity heatmaps, and a backlog-ready task list tied to product metrics (conversion, time-to-complete, retention, support load). In short, the system replaces opinions with comparable data and a clear plan that improves outcomes.

Because the system is standardized and repeatable, results can be compared year-over-year, enabling banks to track progress in UX maturity and evaluate the effectiveness of their digital transformation strategies.

The central insight from Mobile Banking Rank 2025 is that, while mobile banking services continue to mature, important experience gaps remain between leading digital offerings and what customers expect from a seamless everyday channel. Even where some progress has been made year-over-year, key scenarios such as onboarding, money management, and self-service remain unevenly delivered across the market.

One of the most notable patterns in the 2025 ranking is the persistent disparity in basic personal finance flows. The data shows that while most banks support core transactional scenarios such as balance checks and simple transfers, more advanced money-management utilities — automated savings triggers, round-ups, or simple optimizations — remain limited on many platforms. This reduces the overall value delivered to users who increasingly expect banking to do more than just move money.

Usability testing underscores why these gaps matter: customers expect fluid guidance and clear, lightweight interactions for money optimization — and when flows feel disjointed or manual, confidence and engagement drop.

Another chronic deficit highlighted by the ranking is onboarding and early engagement flows. Despite improvements in foundational functionality, many web banking flows still feel “reduced” compared to native experiences:

This translates to slower adoption of valuable capabilities, reinforcing the perception that web is supplemental rather than an equal primary channel.

The ranking also reveals structural constraints and implementation gaps that widen experience differences:

These gaps are not solely due to browser limitations — they also reflect inconsistent prioritization of input-simplification patterns and deeper task facilitation on web platforms.

There are, however, encouraging signs of improvement in secondary yet strategic domains. The gap between web and native in areas such as profile and settings management, personal-data updates, and notification preferences narrowed compared with previous waves. Investments in these flows suggest that banks recognize the importance of comprehensive account control across channels.

Conversely, push notifications remain an acute weak point: web capabilities for proactive alerts are significantly weaker than native — a persistent disadvantage that limits timely communication and user oversight, especially for users who rely on real-time cues for money movement.

The business implication is clear: banks that treat web as an equal customer channel — investing in distribution, onboarding, friction-free capture, and high-value money-management utilities — stand to improve engagement, reduce support burden, and strengthen customer loyalty.

The strategic takeaway from Mobile Banking Rank 2025 is that native experiences still lead in fluidity and device-level affordances, but the mobile web can reclaim large parts of the gap with focused investments. When implemented well, web banking stops being a fallback and becomes a credible, high-value channel in its own right — one that supports both everyday tasks and deeper financial engagement.

Subscribe to our newsletter

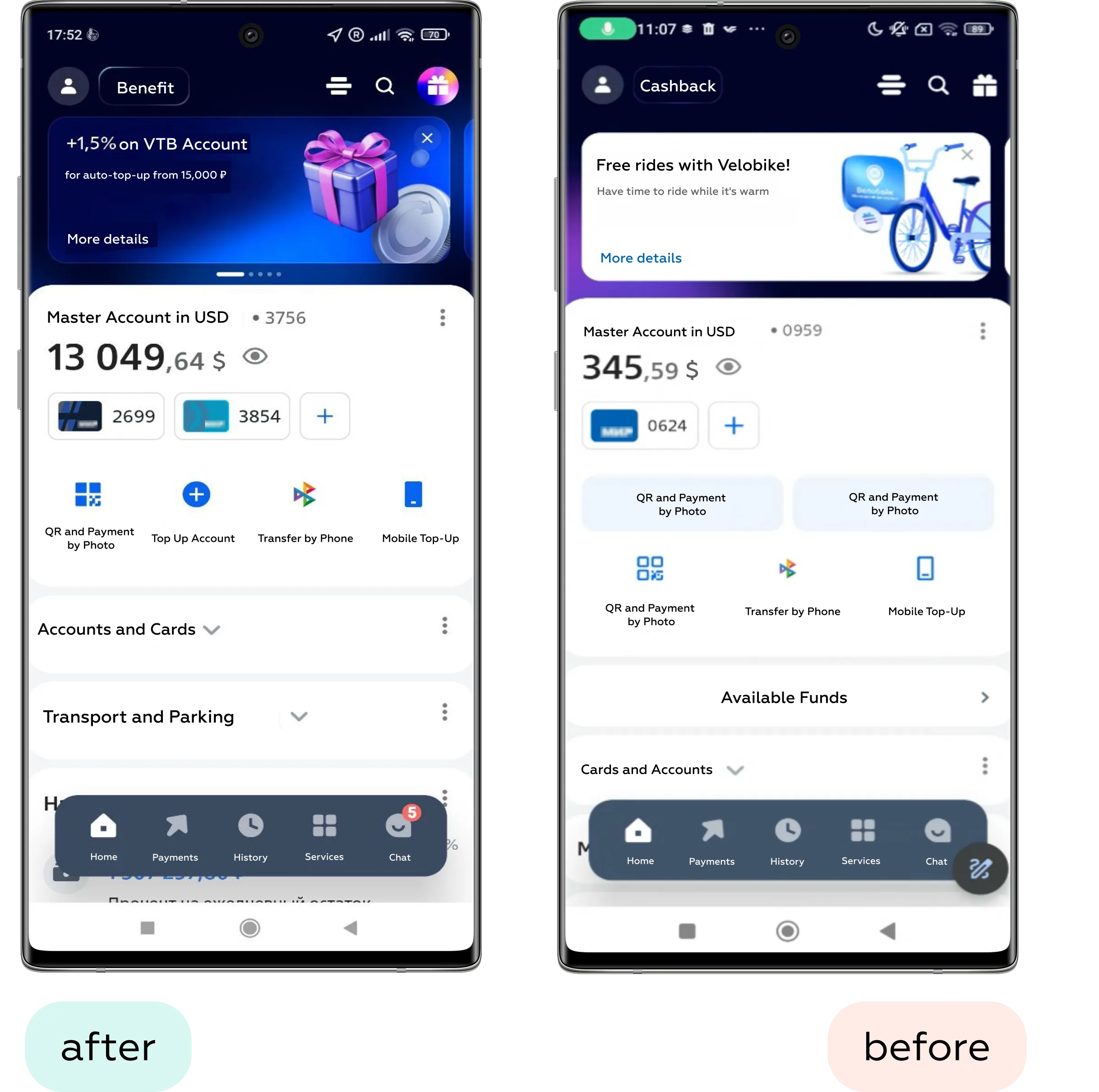

In this section, we’ve selected practical interface solutions highlighted across the Mobile Banking Rank 2025 research — patterns and implementations that help improve usability, efficiency, and customer satisfaction in mobile banking web experiences. The full study includes dozens more best practices that teams can adapt to their own products.

Many leading web banking interfaces bring high-frequency tasks — such as transfers and payments by QR or phone number — onto the main screen, compensating for the lack of native gestures like long-press for quick actions. This reduces the number of taps to start a task and helps users begin common operations without navigating deep menus.

Auto-savings and savings automation are highlighted as differentiators in the 2025 ranking. Some banks allow users to configure savings flows based on previous transaction behavior and flexible rules, giving more control and relevance to personal finance goals. These flows can also include clear feedback on progress toward targets and optional triggers that tie into everyday spending.

3. One-tap delivery of cards and documents

In leading web experiences, customers can order a physical card or request document delivery in a single, clearly visible flow — without navigating through multiple menus. Delivery options, timing, and addresses are shown upfront, and previously used details are prefilled. This reduces friction in a high-value scenario and increases conversion for paid or premium services.

Some mobile web banking services integrate real-estate scenarios directly into the interface — allowing users to explore properties, estimate mortgage payments, or track housing-related steps without leaving the bank’s ecosystem. By embedding these high-involvement journeys into the mobile web, banks reduce friction in complex decision-making, provide clearer cost and payment context, and shorten the path from exploration to action. In usability tests, such thematic sections feel especially valuable and reinforce the perception of the bank as a long-term financial partner rather than just a tool for everyday transactions.

Some banks extend their web banking experience to support children’s cards and accounts, allowing parents to issue cards, set limits, and monitor spending. These flows are designed to be simple and transparent, reinforcing trust and positioning the bank as a long-term financial partner for the entire family. Even when functionality is basic, clear explanations and easy setup significantly improve adoption.

Each of these interface solutions contributes to smoother, faster, and more confident user journeys — from everyday transfers and savings automation to product exploration and task discovery. By adopting similar practices, web banking teams can raise the perceived quality and real usefulness of their digital services.

Mobile Banking Rank 2025 demonstrates that the mobile web is becoming a strategic channel in its own right, but UX maturity remains uneven across the market. Some banks already treat the mobile web as an equal to native apps, delivering seamless onboarding, transparent transactions, and reliable self-service. Others still consider the web a secondary channel, resulting in inconsistent design, hidden friction, and limited functionality.

The ranking highlights that customers expect the same level of convenience and clarity on the web as they do in native apps. When the mobile web experience falls short, banks risk losing engagement, increasing support load, and weakening customer trust — even if their app performs well.

Markswebb’s evaluation system provides a reliable framework to:

Investing in UX for mobile web is not just a design decision — it is a business strategy. Banks that adopt best practices, reduce friction, and increase transparency can unlock measurable benefits: higher conversion in payments and transfers, stronger retention through deposits and savings, and lower churn thanks to trust-building support flows.

Contact us via WhatsApp, send an email, or fill out the form below to learn more.

We’ve evolved dozens of successful financial services and are eager to prove that our expertise can be implemented in other industries and around the world. Have a look at our success stories!

From research and analysis to strategy and design, we help our clients successfully reach their customers through digital services.