Contents

Retail banking has long been designed around a single user: one person, one account, one interface. This model no longer reflects how people actually manage money today.

Households increasingly operate as financial units. Partners share everyday expenses and long-term goals, parents manage children’s spending, and adult children support elderly relatives. These scenarios are becoming part of daily financial behavior — yet they remain poorly supported by standard mobile banking experiences.

These gaps are consistently observed in Markswebb’s Mobile Banking Rank 2025, where cross-product analysis highlights how leading banks begin to adapt mobile banking UX to shared and family-based financial scenarios.

At the same time, financial responsibility is spreading across family members. Children receive cards earlier, teenagers manage allowances independently, and shared subscriptions and savings goals are becoming the norm. Users expect banks to support these dynamics natively, not through manual workarounds or external tools.

From the bank’s perspective, this shift is also structural. Competition for primary app status is intensifying, and growth increasingly depends on deeper engagement within existing households rather than individual acquisition alone. Family banking allows banks to expand usage horizontally — across multiple users — while staying within a single ecosystem.

As a result, family banking is emerging not as a niche feature set, but as a response to a fundamental mismatch between real-life financial behavior and the single-user logic embedded in most digital banking products.

For users, family banking is not perceived as a separate product or a special mode. It is expected to work naturally as part of everyday financial management — without forcing families to restructure how they use money.

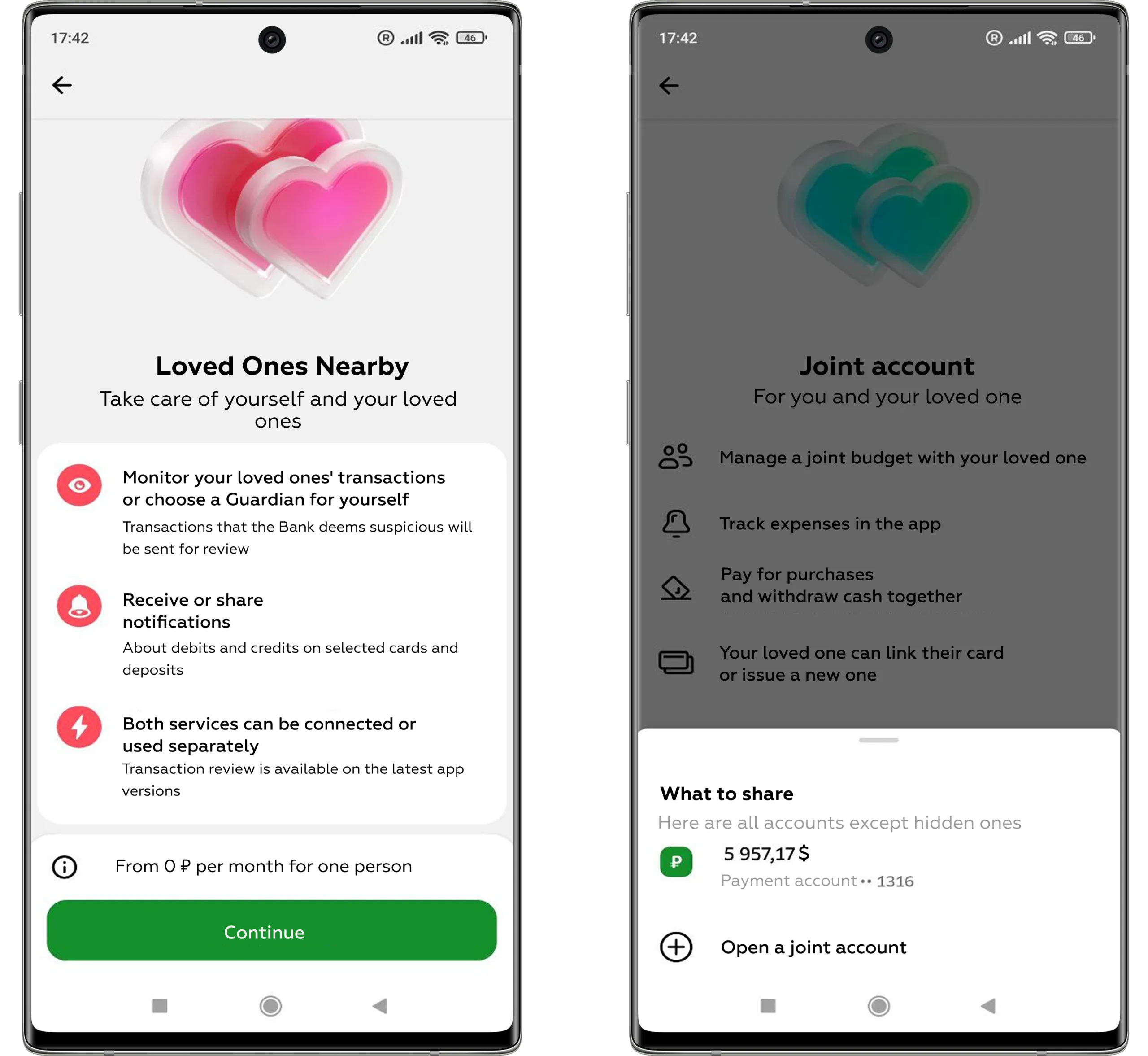

At the core of these expectations is shared visibility without loss of personal control. Partners want to see joint expenses and balances while keeping private accounts and spending separate. Parents want oversight of children’s finances without micromanaging every transaction. Teenagers expect autonomy, not a simplified or “childish” version of banking.

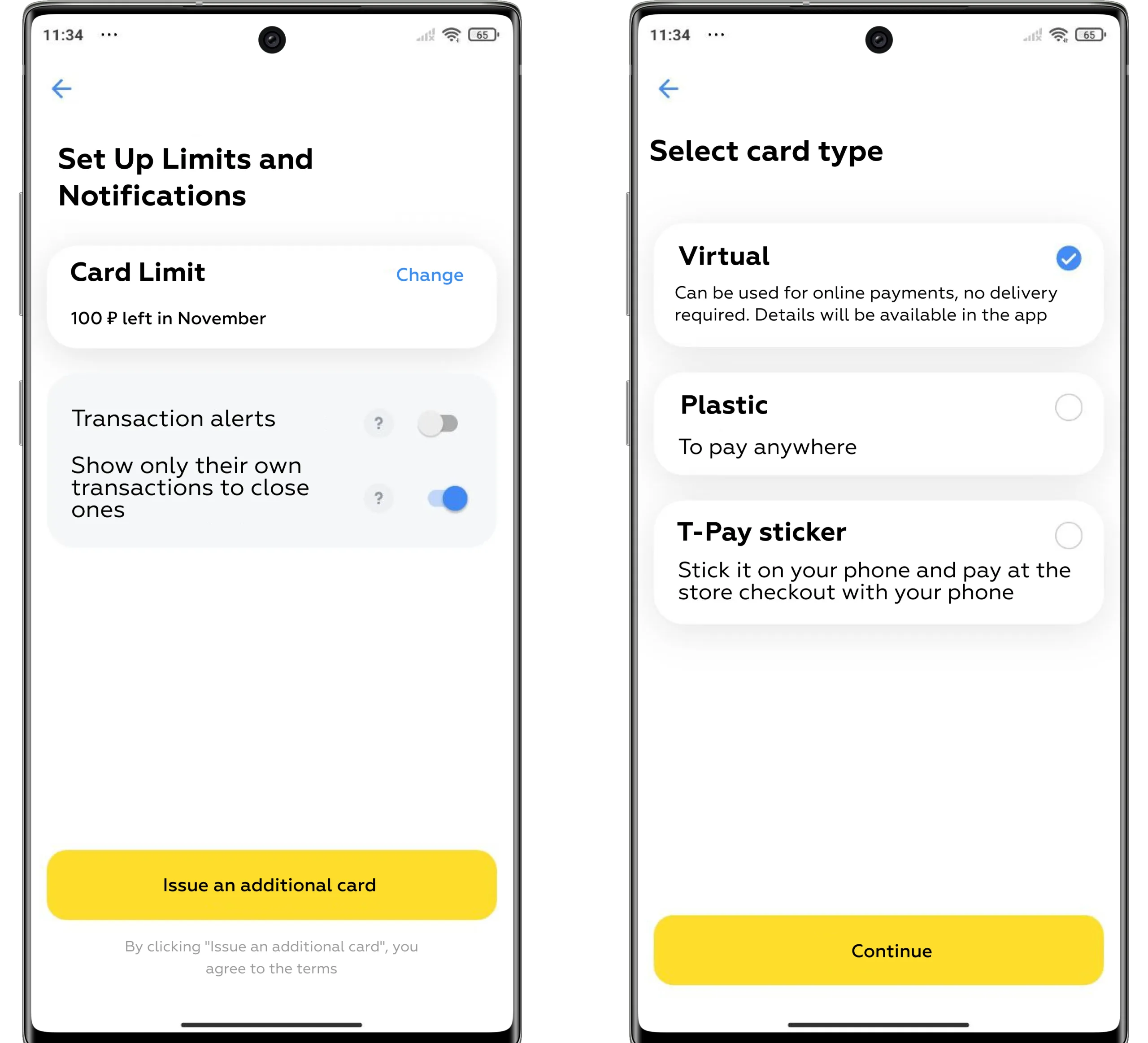

Another key expectation is flexible roles and permissions. Family members are not equal in responsibility, and their roles change over time. Users expect banks to support nuanced access models: spending limits instead of hard blocks, approval flows instead of full restrictions, and temporary permissions for specific scenarios.

Finally, users expect family banking to reduce coordination costs. Everyday situations — allowances, shared subscriptions, saving for a trip, covering household expenses — should be easy to set up, track, and adjust. When banks fail to support these scenarios, families compensate with external tools, fragmenting the experience and weakening the bank’s role in financial decision-making.

In practice, users are not asking for more features. They expect banking interfaces to reflect real family dynamics — where trust, responsibility, and independence coexist within a shared financial context.

Most mobile banking apps are still built around an individual account holder, with family-related features added as secondary layers. As a result, family scenarios are supported inconsistently and often create more friction than value.

Joint accounts, where available, usually rely on rigid access models. Family members are either granted full control or limited to basic viewing rights, with little room for nuance. This makes it difficult to reflect real-life responsibilities — especially in households where financial control is shared but not equal.

Children’s and teen products often exist as isolated solutions. Separate apps or simplified interfaces break continuity, forcing parents to manage finances across multiple environments while children fail to develop a gradual understanding of real banking behavior. Instead of learning within a shared financial context, younger users are placed outside it.

Another common limitation is the lack of separation between personal and shared finances. Users struggle to distinguish household spending from individual transactions, which complicates budgeting, planning, and accountability. Over time, this erodes trust in the app as a reliable tool for financial coordination.

When core family scenarios are poorly supported, users resort to workarounds: messaging apps for approvals, spreadsheets for tracking shared expenses, multiple cards with informal rules. These workarounds increase cognitive load and shift meaningful financial interactions outside the bank’s ecosystem — precisely where banks are trying to strengthen engagement.

Leading banks approach family banking not as an extension of account management, but as a set of shared financial scenarios. Instead of duplicating products for each family member, they redesign the experience around how households actually coordinate money.

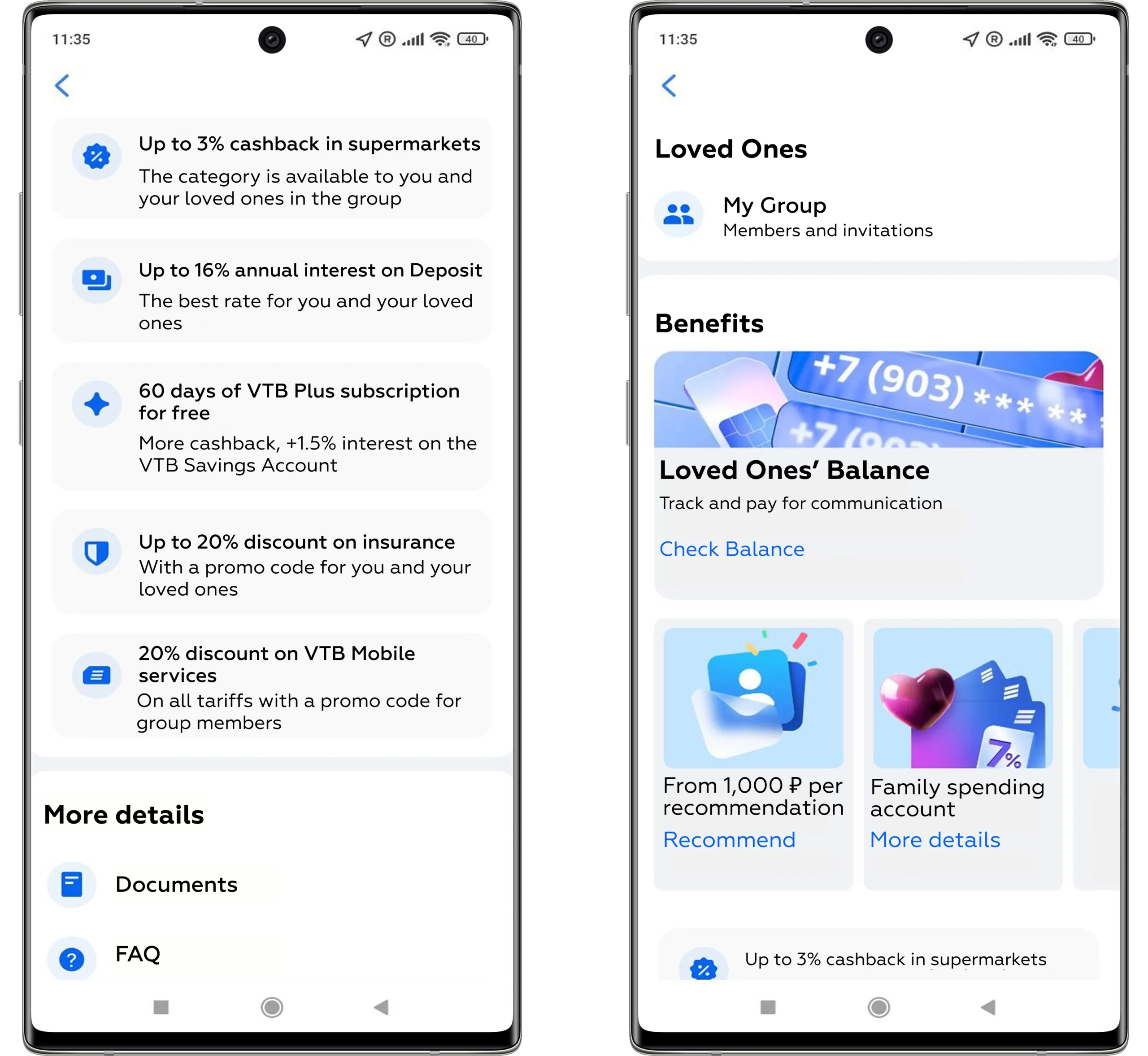

One common shift is the introduction of household-level views. These dashboards aggregate shared balances, goals, and recurring expenses, while still allowing each user to switch seamlessly back to their personal financial context. Visibility becomes role-based rather than universal, reducing both friction and conflict.

Another key change is the move toward granular permissions. Rather than granting or revoking full access, advanced solutions support spending limits, category-based controls, approval flows, and time-bound permissions. This allows responsibility to scale naturally — from supervised use to independent decision-making.

Education is increasingly embedded into everyday actions. Instead of separate learning modules, children and teenagers receive contextual prompts, spending insights, and feedback tied directly to real transactions. This turns routine financial activity into a learning experience without adding extra steps.

Technically, these experiences rely on modular design. The same core interface adapts to different family roles, reducing complexity while preserving consistency. For users, this creates a sense of one shared financial space — flexible enough to evolve as family dynamics change.

In mature retail banking products, family banking is not implemented through isolated features or separate modes. Instead, it emerges from design practices that support shared financial behaviour while preserving individual autonomy. Based on cross-product analysis and UX benchmarking, several recurring family-banking patterns stand out.

Lowering access barriers without forcing full onboarding

Advanced family banking solutions allow users to grant meaningful access to accounts without turning every participant into a fully onboarded client. Access can be provided without issuing physical cards or opening standalone products, enabling quick involvement in everyday scenarios such as shared spending or temporary support.

At the same time, visibility is deliberately scoped. Users may allow spending or balance access while restricting transaction history, ensuring privacy and trust remain intact within shared financial contexts.

Designing flexible access instead of binary control

Rather than relying on all-or-nothing permission models, leading interfaces support nuanced access structures. Users can share specific accounts or cards, connect notifications independently from transactional access, and adjust permissions as family roles evolve.

This flexibility enables assistance without loss of control — for example, allowing relatives to monitor balances or receive alerts without granting direct access to funds.

Using shared benefits to encourage ecosystem consolidation

Family banking is often reinforced through collective value. Improved product conditions, shared bonuses, and aggregated balance visibility motivate households to consolidate financial activity within one ecosystem.

These shared incentives also create natural entry points for promoting adjacent products, expanding usage without relying on aggressive cross-selling mechanics.

Embedding children’s financial products into the family context

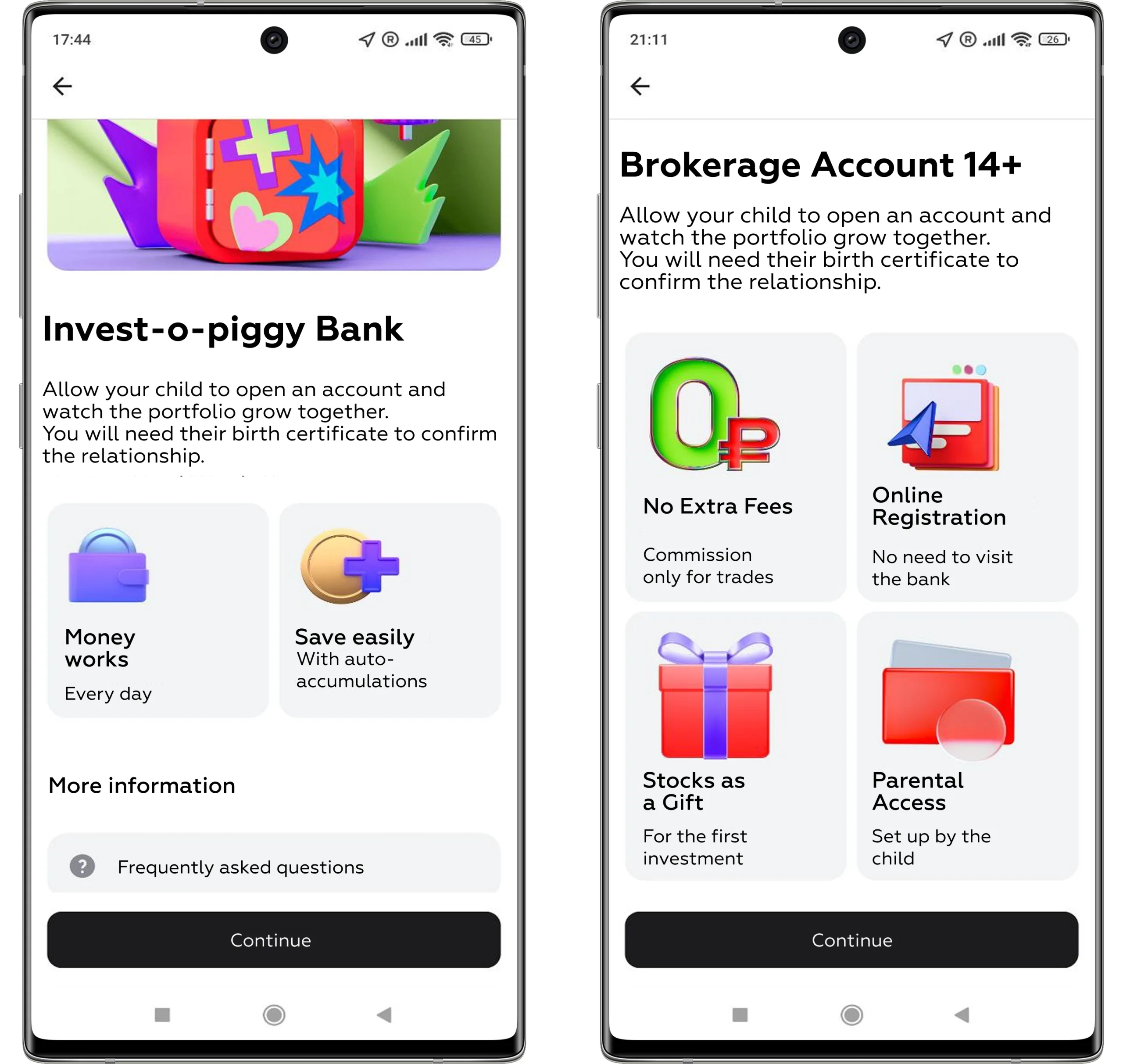

Children’s and teen solutions are most effective when designed as part of a shared financial environment rather than isolated products. Investment tools with flexible top-ups, brokerage accounts with parental access, and remote onboarding help children learn through real financial interactions.

For users, this creates a safe and continuous learning space. For banks, it drives early adoption of investment products and anchors long-term family loyalty within a single digital ecosystem.

Family banking reflects a broader transformation in retail banking UX — from individual product usage to shared financial coordination. As households increasingly manage money collectively, the limitations of single-user banking models become more visible, both for users and for banks.

Leading solutions demonstrate that family banking does not require separate interfaces or parallel products. It requires rethinking access, visibility, and responsibility as dynamic variables that change over time. When designed well, family banking balances trust and autonomy, enabling shared financial behaviour without compromising personal control.

From a business perspective, family banking strengthens retention by embedding the bank into everyday family routines. It expands engagement across multiple users, supports early relationships with younger customers, and opens new monetisation opportunities grounded in real value rather than feature overload.

Ultimately, family banking is not a niche capability. It is an indicator of product maturity — showing how well a bank can adapt its UX to real-life financial behaviour and scale from individual transactions to household-level financial ecosystems.

Contact us via WhatsApp, send an email, or fill out the form below to learn more.

We respond to all messages as soon as possible.

We’ve evolved dozens of successful financial services and are eager to prove that our expertise can be implemented in other industries and around the world. Have a look at our success stories!