As competition for customer funds intensifies, banks can no longer rely only on rates and promotions to drive growth. Increasing customer LTV in banking now depends on product logic, transparency, and the overall quality of the user experience.

To strengthen its savings proposition and identify new opportunities for LTV growth, one of the leading Eastern European banks partnered with Markswebb to explore how the market is evolving. In this case, customer LTV means the long-term value a client generates through retention, engagement, balance growth, and use of additional products.

Contents

Banks across Europe are actively experimenting with new approaches to customer retention, engagement, and ecosystem-driven growth — all of which directly influence customer LTV in banking. As more solutions enter the market, it becomes harder to distinguish between temporary experiments and shifts that are redefining user expectations.

The client approached Markswebb with several objectives:

As a result of the research, the bank received a practical framework for identifying and prioritizing customer LTV growth opportunities in savings products.

At Markswebb, trend analysis is approached as a product strategy task rather than simple market monitoring: its purpose is to show which market shifts can strengthen customer LTV in banking through better product logic, UX, and service design. Our trendwatching methodology helps companies identify emerging product, UX, and service patterns across European and global markets — and understand which of them are becoming sustainable competitive advantages.

In fast-changing categories such as savings and wealth accumulation products, trend analysis is critical for distinguishing short-term experiments from long-term shifts that genuinely affect customer value and customer LTV.

To achieve this, we analyze trends at the intersection of product logic, user experience, technology, and ecosystem scenarios — then translate observations into practical product opportunities through mechanics, journeys, and implementation patterns.

The Markswebb evaluation framework allows companies to:

At the beginning of the project, Markswebb experts defined the research scope and mapped the key customer journeys related to savings and accumulation products.

This approach allowed us to evaluate not only how financial services attract customer funds, but also how they retain and grow balances over time — one of the key drivers of customer LTV in banking — identifying where customer lifetime value is gained or lost, and which product decisions truly influence user behavior rather than simply improving interface aesthetics.

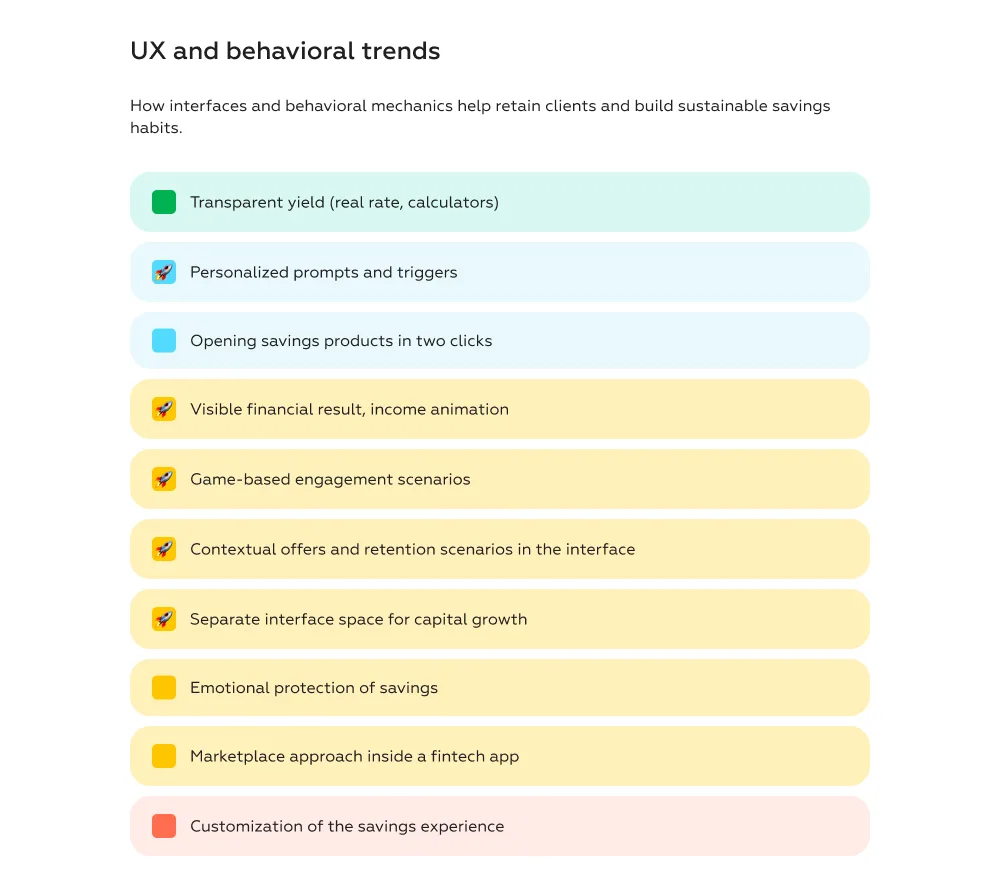

The research focused on journeys that have a direct impact on customer LTV in savings products:

The benchmark included leading European banks, digital banks, and fintech services, as well as multiple types of savings products — from traditional deposits to flexible savings and hybrid accumulation models.

This made it possible to capture not only the current maturity level of the market, but also the differences in product logic, engagement mechanics, and UX strategies across providers.

The first stage of the project focused on analyzing how savings products and related customer journeys are structured across the client’s ecosystem and the broader European market.

We examined how banks design savings propositions, which mechanisms they use to attract and retain customer funds, and how interaction logic is built throughout the product lifecycle. The analysis covered not only rates and conditions, but also behavioral mechanics, engagement patterns, and long-term retention approaches that influence customer LTV in banking.

Using mystery shopping and real product onboarding flows, Markswebb researchers reconstructed the full customer journey — from product discovery and selection to activation and ongoing usage.

Particular attention was paid to existing customer scenarios in order to understand how financial services encourage recurring interactions, retain balances over time, and build habitual engagement with savings products.

We analyzed the core journeys directly connected to LTV growth, including:

Special focus was placed on how product limitations, rules, and conditions affect the user experience and influence long-term customer behavior.

The collected observations were then combined with desk research and expert interviews to connect product decisions with actual user behavior and their impact on customer lifetime value.

This stage allowed us to move beyond describing isolated features and identify sustainable market trends that influence retention, engagement, and monetization metrics.

The next step was transforming fragmented observations into a system that could be applied at the product strategy level.

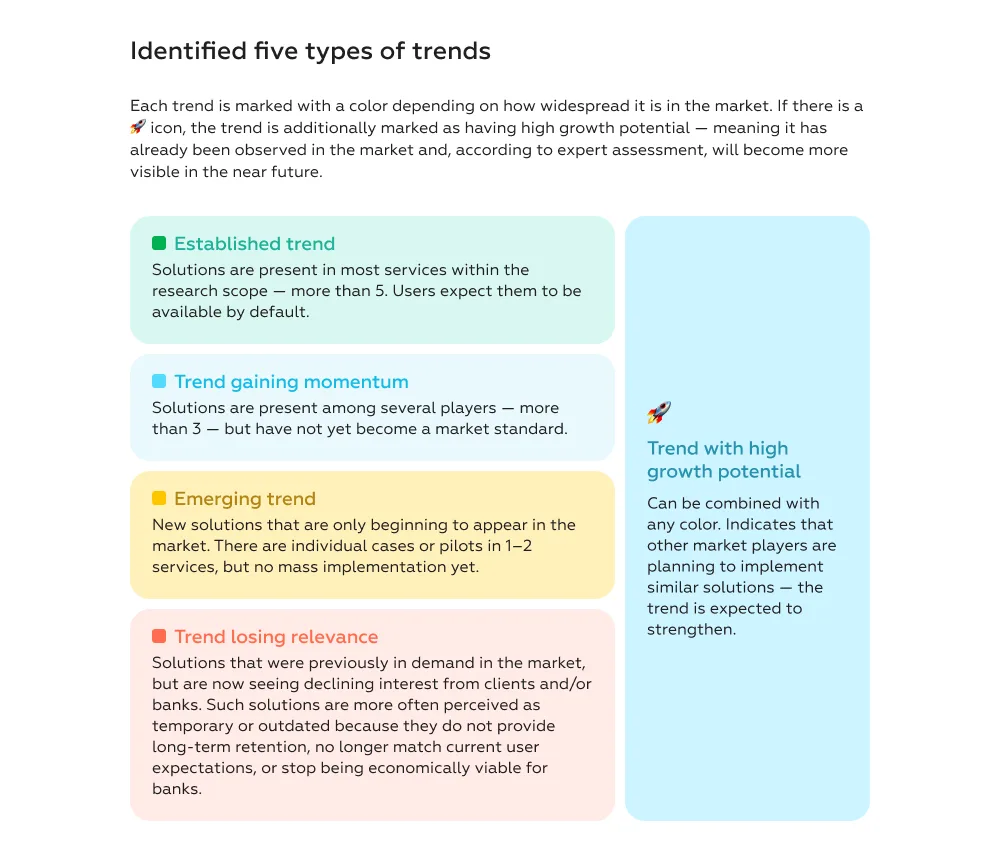

At this stage, Markswebb experts evaluated the role each trend plays in current market competition and assessed how critical it is for influencing key business metrics.

This typology framework helps product teams distinguish between solutions that already affect competitiveness today and trends with stronger potential to increase customer LTV in banking over time.

Such an approach makes it possible to understand where products already need to meet established user expectations — and where banks still have the opportunity to differentiate and define new market standards.

Importantly, the framework connects interface-level changes with deeper shifts in product logic, ecosystem integration, and service architecture.

To make the system actionable, all identified trends were grouped into four categories:

As a result, the client received a structured framework that helps:

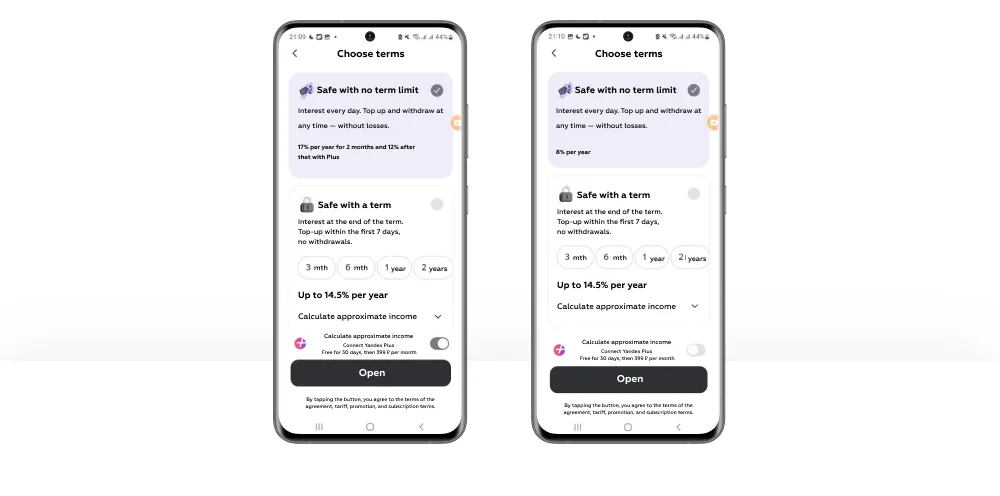

One of the most sustainable trends in the savings market today — and an important mechanism for improving customer LTV in banking — is the shift from fixed interest rates toward dynamic profitability models, where the final yield depends on customer behavior.

Instead of offering a single static rate, financial services provide a base interest rate that can increase when customers complete certain actions or meet predefined conditions.

Banks combine a standard savings rate with a system of activity-based bonuses. Customers can increase profitability, for example, by:

As a result, the profitability model becomes dynamic and behavior-driven — controllable both for the bank and for the customer.

This approach makes savings products feel more transparent and manageable. Customers clearly understand which actions influence returns and can improve profitability without switching to more complex or higher-risk financial instruments.

The model also increases the sense of control and engagement, turning passive savings into an interactive financial product.

For banks, dynamic rate models create a mechanism for encouraging high-value customer behavior, including:

This is especially important for customers who actively compare profitability across providers and are willing to redistribute funds in search of better conditions.

Based on extensive market expertise and product research experience, Markswebb developed a prioritization framework for the identified recommendations.

The framework evaluates initiatives across two dimensions:

These recommendations are connected to trends with strong growth potential.

Such solutions are already moving beyond isolated experiments and beginning to scale across the market. Customer expectations around these mechanics are gradually forming, making them strategically important for future competitiveness.

These recommendations relate to trends that are still emerging.

While they are not yet widely adopted or fully standardized, individual implementations already demonstrate measurable value and may become future growth opportunities as the market evolves.

Markswebb trendwatching is designed to reduce uncertainty and accelerate product decision-making in rapidly evolving markets.

Rather than reacting to isolated competitor releases, teams gain a structured understanding of broader market evolution and can make decisions based on systemic analysis instead of short-term signals.

In this project, the approach helped the client:

As a result, the team received not just a collection of ideas, but a practical framework explaining how specific product decisions can translate into measurable business growth and higher customer LTV in banking.

Looking to identify the trends that will shape your market? Contact us via WhatsApp or email to discuss your product challenges.

Every year we conduct up to 15 studies of digital services. These are industry benchmarks that reflect the state of the market and trends.