Gen Z — those born roughly between 1997 and 2012—are entering their peak years of financial independence. While their average wealth is still lower compared to millennials or older generations, their influence on financial markets is growing rapidly. From micro-investing apps and commission-free trading to crypto and alternative assets, Gen Z is shaping the demand for a new kind of investment experience.

Unlike previous generations, this cohort is mobile-first, skeptical of traditional finance, and highly attuned to digital experiences. For investment platforms, that means the expectations are higher: fast, transparent, and engaging services are no longer a “nice to have” but a baseline requirement.

Designing for Gen Z investors is not just about attracting a younger audience. It is about preparing for the next decade of wealth building—when their income, savings, and investment power will expand significantly.

Contents

1. Financial behavior

Gen Z investors often start small. They experiment with micro-investing, fractional shares, and alternative assets such as crypto. Their time horizons tend to be shorter than those of older generations, and many prioritize quick returns over long-term strategies. At the same time, values matter: ESG and socially responsible investments are increasingly part of their portfolios.

2. Digital habits

This is the first mobile-native generation. They expect seamless digital journeys, intuitive navigation, and instant access across devices. Long registration forms, unclear onboarding, or clunky interfaces quickly lead to churn.

3. Education and trust

Financial literacy varies widely across Gen Z. Many enter investing with limited knowledge, so they value platforms that provide built-in education: from bite-sized tutorials to contextual hints and simulated portfolios. Trust is fragile—opaque fees or hidden risks can permanently damage a platform’s reputation with this audience.

4. Social and community dimension

Gen Z is heavily influenced by peers, online communities, and social media. They look for spaces to discuss strategies, share achievements, and learn from each other. For them, investing is not just about financial gain but also about belonging and participation.

1. Simplicity and speed

Gen Z expects investment platforms to feel as effortless as their favorite social apps. This means clear navigation, minimal friction during onboarding, and fast execution of core actions such as deposits, trades, or withdrawals. Every extra tap or delay risks losing their attention.

2. Integrated learning

Education cannot be separated from the experience. Contextual tooltips, guided tours, and interactive explainers help Gen Z investors build confidence while staying in the flow. Gamified learning elements—like quizzes, badges, or demo portfolios—turn complexity into engagement.

3. Radical transparency

Hidden fees and unclear conditions are deal-breakers. Gen Z values clarity around costs, risks, and performance metrics. Visual explanations—such as infographics of fees or plain-language risk alerts—create trust and reduce hesitation.

4. Social and gamified layers

Investing for Gen Z is also about community. Features such as leaderboards, progress tracking, and the ability to share milestones with friends encourage ongoing engagement. Integrating social proof—ratings, comments, or collaborative challenges—helps replicate the dynamic of online communities within the app.

5. Personalization

Gen Z expects platforms to recognize their preferences. From tailored investment recommendations to customizable dashboards and alerts, personalization drives both retention and satisfaction.

Real-world cases show how these UX patterns are applied in practice. Leading apps don’t reinvent finance — they redesign the way users experience it.

1. Robinhood – Fractional shares (Lowering entry barriers)

Why it matters: For Gen Z, limited capital is a major barrier to starting their investment journey. If the minimum entry point feels too high, they simply won’t engage.

Best practice: Robinhood allows users to buy fractions of stocks with as little as one dollar. This lowers the threshold for participation, turning investing into something accessible rather than exclusive. The simplified purchase flow keeps the process fast and intuitive.

2. Revolut – In-app explainers (Integrated learning)

Why it matters: Many Gen Z investors lack formal financial education. When faced with complex products like crypto or commodities, they need guidance in the moment.

Best practice: Revolut integrates short explainers and contextual prompts directly into the trading interface. These act as mini-lessons, clarifying risks and product details without interrupting the flow. Learning becomes part of the experience rather than a separate track.

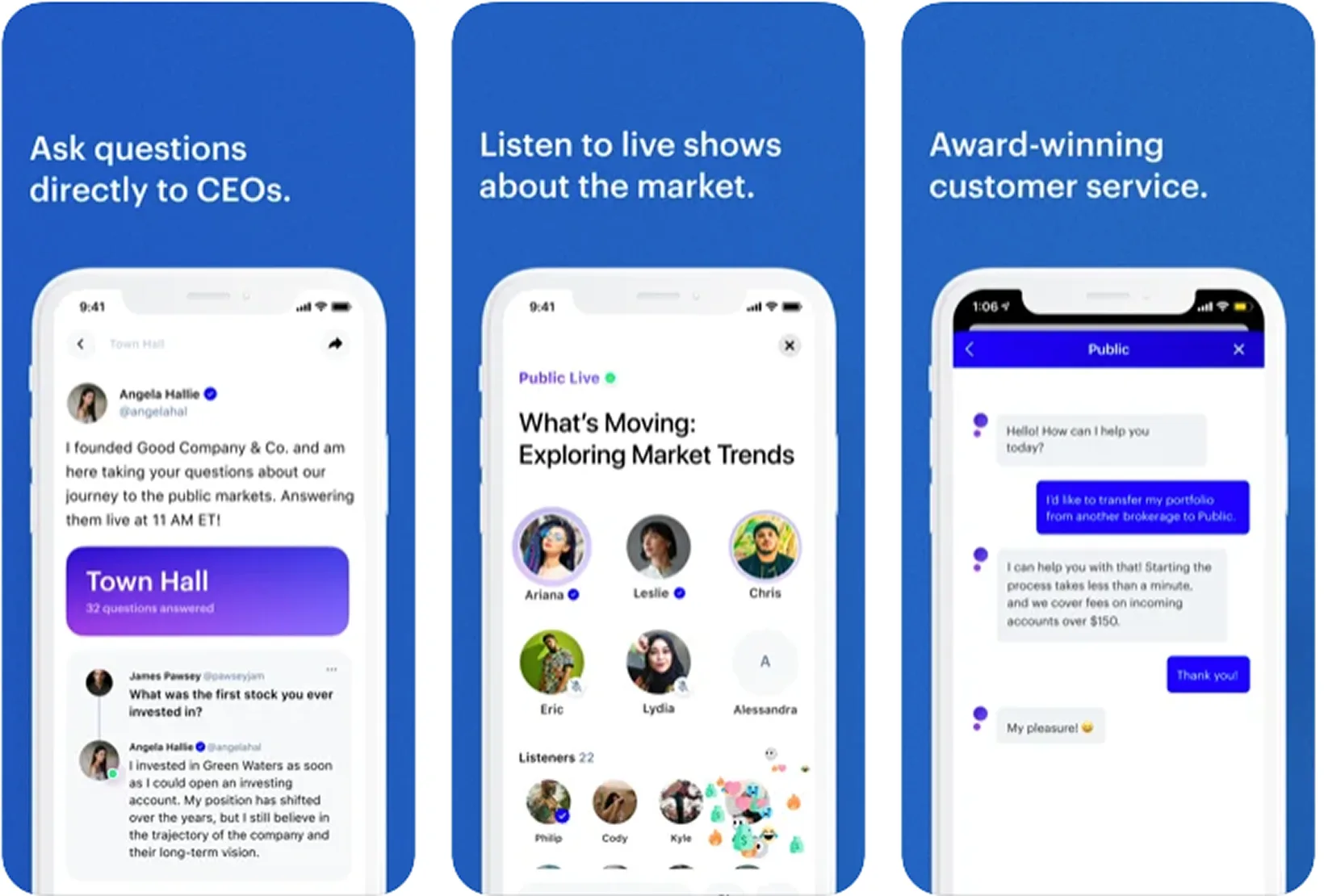

3. eToro – CopyTrading (Community-driven investing)

Why it matters: Gen Z looks for peer validation and shared learning. Traditional investment apps that isolate users fail to tap into this social mindset.

Best practice: eToro allows users to follow and copy the portfolios of experienced investors. This social layer creates a sense of community, builds trust, and helps beginners learn through observation. Investing becomes interactive and social rather than individual and intimidating.

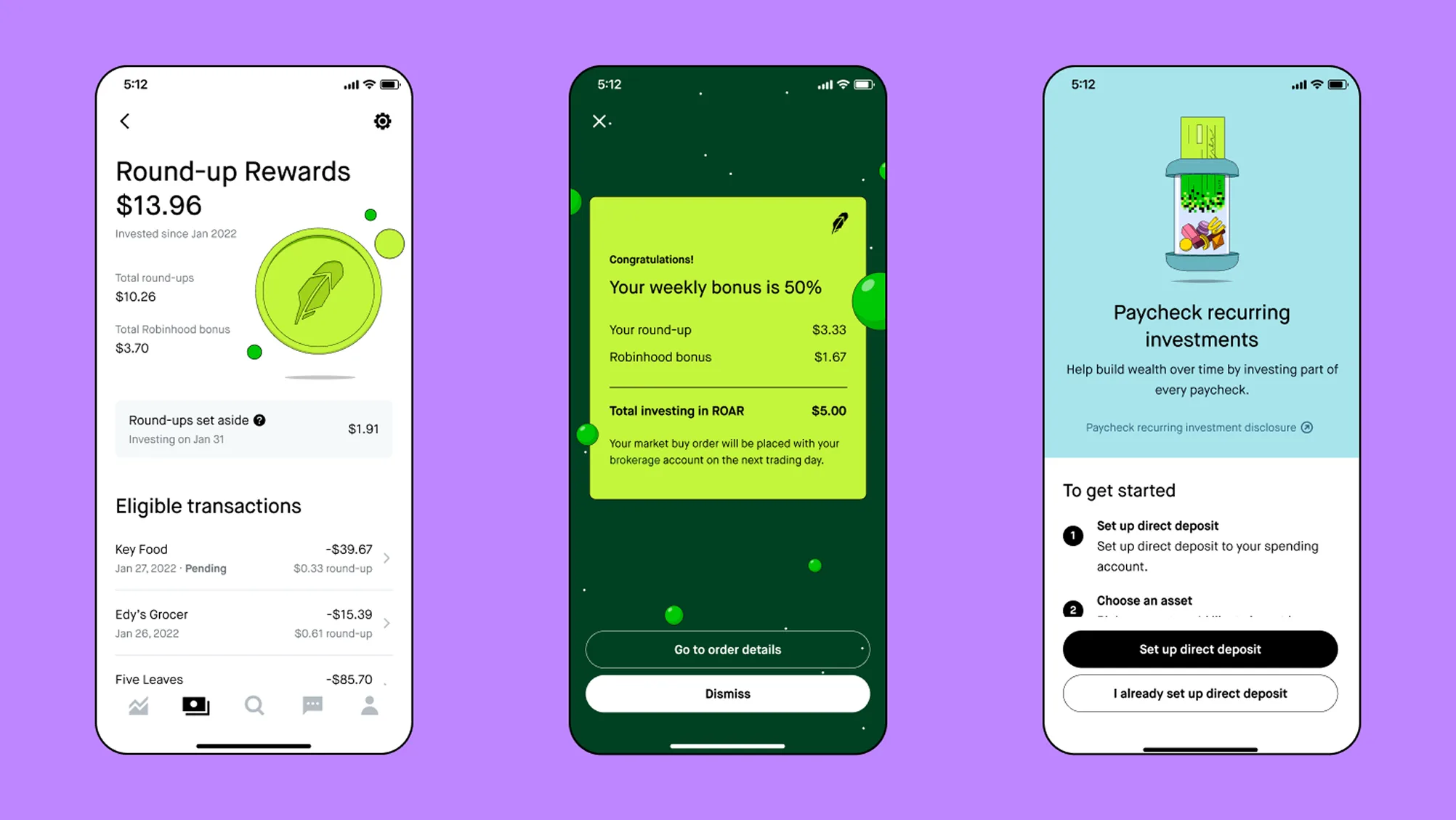

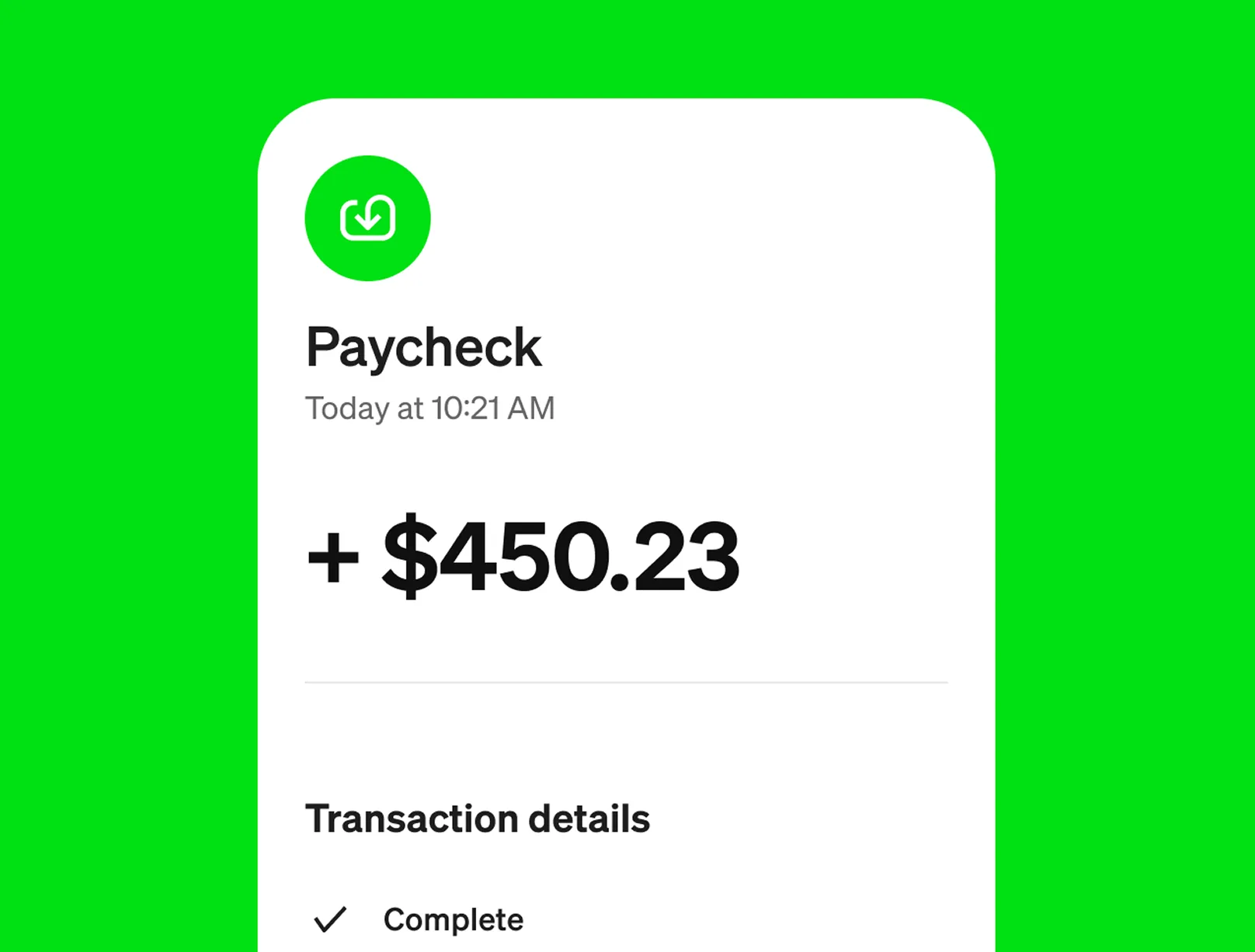

4. Cash App – Round-ups and auto-invest (Micro-investing habits)

Why it matters: Gen Z prefers low-friction, habitual ways to grow their wealth. Asking them to commit large sums upfront can discourage participation.

Best practice: Cash App enables users to automatically invest spare change from everyday purchases or set up recurring micro-investments. This aligns with Gen Z’s preference for incremental progress and creates positive financial habits over time.

5. Public.com – Transparent pricing (Radical trust-building)

Why it matters: Gen Z is highly skeptical of hidden costs and opaque commissions. Any lack of clarity risks eroding trust permanently.

Best practice: Public.com eliminated payment-for-order-flow revenue and communicates clearly how it sustains its business. The app also explains risks in plain language and uses visual design to highlight cost transparency. This open model directly addresses Gen Z’s demand for authenticity.

1. Overloading with information (Cognitive fatigue)

Why it matters: Gen Z expects clarity and focus. Interfaces that present too many charts, stats, or complex flows at once can overwhelm rather than empower.

What to avoid: Platforms that mimic professional trading terminals without simplification. This creates steep learning curves and deters long-term use.

2. Hiding fees and risks (Eroding trust)

Why it matters: Transparency is a non-negotiable. If fees, spreads, or risks feel hidden, Gen Z users won’t just churn—they will actively distrust the brand.

What to avoid: Small print disclaimers or fee structures buried deep in terms and conditions. Once trust is broken, recovery is nearly impossible with this audience.

3. Ignoring community and social features (Missed engagement)

Why it matters: For Gen Z, investing is not purely transactional. They seek validation, peer learning, and shared experiences. Without community features, engagement remains shallow.

What to avoid: Apps that position investing as a solitary task, without opportunities to learn from or connect with others.

4. Treating gamification as gimmick (Superficial engagement)

Why it matters: Gen Z responds well to progress tracking and gamified learning—but only if it adds real value. Poorly designed gamification risks trivializing financial decisions.

What to avoid: Flashy badges or casino-like animations that encourage impulsive behavior. This approach can backfire, leading to regulatory scrutiny and user backlash.

5. Neglecting personalization (Generic experience)

Why it matters: Gen Z expects digital services to adapt to them, not the other way around. A one-size-fits-all interface feels outdated.

What to avoid: Generic dashboards, irrelevant product offers, and alerts that don’t match user behavior. Without personalization, retention suffers.

Gen Z is reshaping the investment landscape. They are entering the market with limited capital but strong digital expectations, and their influence will only grow as their income and savings expand. For financial services, the challenge is not just to attract this audience today, but to build platforms that will remain relevant as Gen Z transitions from novice investors to long-term wealth builders.

The winners will be those who design experiences that are simple, transparent, and engaging—blending education, community, and personalization into the core of the product. Those who fail to adapt risk losing not just a segment of users, but the future of the market.

At Markswebb, we analyze how leading investment and asset management apps evolve to meet new expectations. Through studies such as our Asset Management Apps Rank 2025 and tailored research projects, we deliver benchmarks and actionable insights that help product teams design services aligned with the needs of the next generation of investors.

If you want to explore how to adapt your service for Gen Z investors, get in touch with us.

We respond to all messages as soon as possible.

We’ve evolved dozens of successful financial services and are eager to prove that our expertise can be implemented in other industries and around the world. Have a look at our success stories!