Know first!

Subscribe to our newsletter

Business mobile banking UX is no longer defined only by interface convenience — it increasingly reflects how well the app supports real business tasks from start to finish.

Business mobile banking is moving beyond basic digitalization. For small and microbusinesses, the mobile app is no longer just a channel for payments, balances, and statements — it is becoming a daily tool for managing operations, services, access, documents, and communication with the bank.

This shift creates a new question for banks: how to evaluate whether a mobile bank is still a transactional tool or already works as a full business platform.

Business Mobile Banking Rank 2026 was designed to answer this question. The study uses Markswebb’s scenario-based evaluation system to assess the current state of mobile banking for business, identify market trends, reveal UX gaps, and highlight practices used by leading products.

Contents

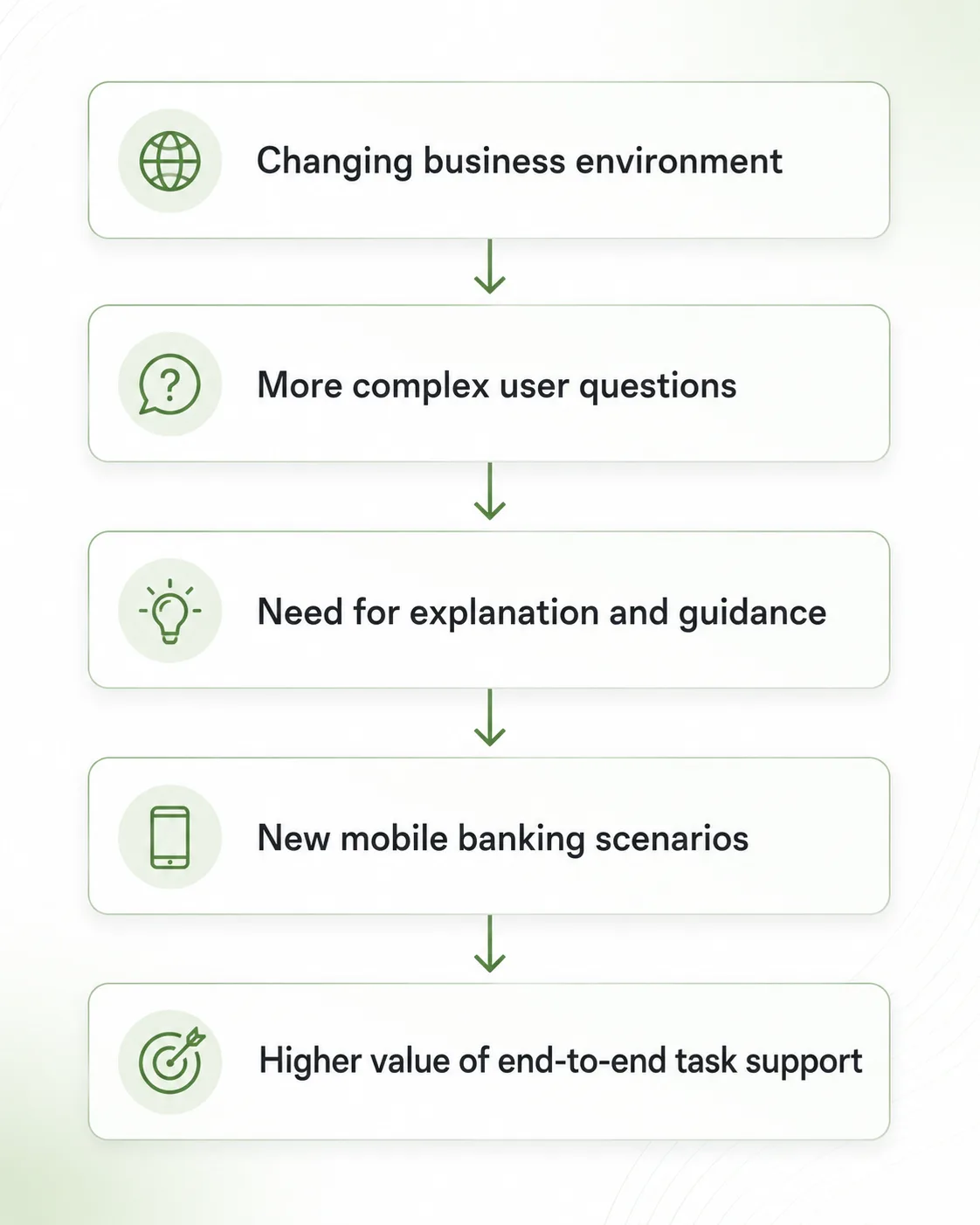

Several broader changes are reshaping what small and microbusinesses expect from mobile banking — and making business mobile banking UX a more important factor in digital service quality.

First, the level of digitalization continues to grow. Entrepreneurs increasingly expect to solve everyday business tasks in mobile channels, without switching to web banking, contacting support, or using separate services outside the bank. Payments, balances, cards, and statements are no longer enough to define a strong digital experience.

Second, changing tax and legislative requirements create more situations where business clients need guidance. A general update from the bank is not enough if the user still has to understand the consequences on their own. Entrepreneurs need to know whether a change affects their company, what risks it creates, and what they should do next.

Third, AI is changing expectations for digital service. But in business banking, its value is not in adding a separate chatbot. The stronger use case is assistance embedded into real tasks: search, forms, documents, product selection, tax-related decisions, and support.

Together, these changes make business mobile banking scenarios more complex — and raise the importance of business mobile banking UX as a way to guide users through end-to-end tasks, reduce uncertainty, and turn the mobile app into a stronger business management tool.

In this context, competitive advantage depends less on the number of available functions and more on the quality of end-to-end scenarios. Banks that help entrepreneurs understand changes, manage risks, find relevant services, and complete more tasks in the mobile channel can turn mobile banking into a stronger driver of engagement, transactional activity, product usage, and long-term client value.

Better scenario design can influence:

Business Mobile Banking Rank 2026 research looks at business mobile banking UX through practical user tasks: from everyday payments and account control to tax-related support, role management, credit products, and ecosystem services.

The benchmark includes 10+ important business banking products. This allows us to compare not only the overall user experience, but also the effectiveness of separate areas within business banking: payments, documents, products, support, access management, tax-related scenarios, and embedded services.

The evaluation is based on 140+ user scenarios and 790 binary criteria. Each criterion checks whether a specific condition is fulfilled in the user journey: for example, whether the function is easy to find, whether the flow can be completed in mobile, whether restrictions are explained, whether the next step is clear, and whether the scenario works consistently with real business needs.

This makes the research both a diagnostic tool and a source for backlog prioritization. It shows where mobile banks already support business clients well, where business mobile banking UX gaps create friction, and which improvements can increase engagement, transactional activity, product usage, or trust in the mobile channel.

Below are several examples of insights identified through this evaluation system.

Subscribe to our newsletter

This shift is visible in the growing number of services inside mobile banking apps: accounting tools, acquiring, deposits, credit products, currency operations, work with self-employed contractors, corporate cards, certificates, documents, and communication with managers or support teams.

The app becomes a place where the entrepreneur can solve business tasks without switching to web banking, contacting support, or looking for separate services outside the bank.

The most mature products are moving toward a mobile-only model. This makes consistency with web banking especially important: if a user can start a scenario in mobile but has to finish it elsewhere, the app still remains an auxiliary channel.

A service creates value when the client can move through the full task without friction:

The benchmark also shows that banks are increasingly using mobile channels to inform business clients about tax, legislative, and regulatory changes. A mobile bank may send a notification or link to an article, but the user is left to interpret the consequences independently.

The product informs, but does not guide. For an entrepreneur, the main question is not simply “What changed?” but “Does this affect my business, and what should I do next?” This is where business mobile banking UX should move beyond communication and become decision support.

A stronger scenario connects three levels:

The benchmark shows that AI practices in mobile banking for business are still developing. The most useful model is not “talk to an assistant,” but “get help at the right moment of the scenario.”

AI can create value when it helps the user:

For banks, this means that AI should be designed as part of product logic. The closer it is to payments, documents, taxes, limits, services, and support scenarios, the more useful it becomes for business clients.

The same shift is visible in specific interface practices identified in the benchmark. These examples show how leading products reduce uncertainty, improve navigation, and help users move from information to action.

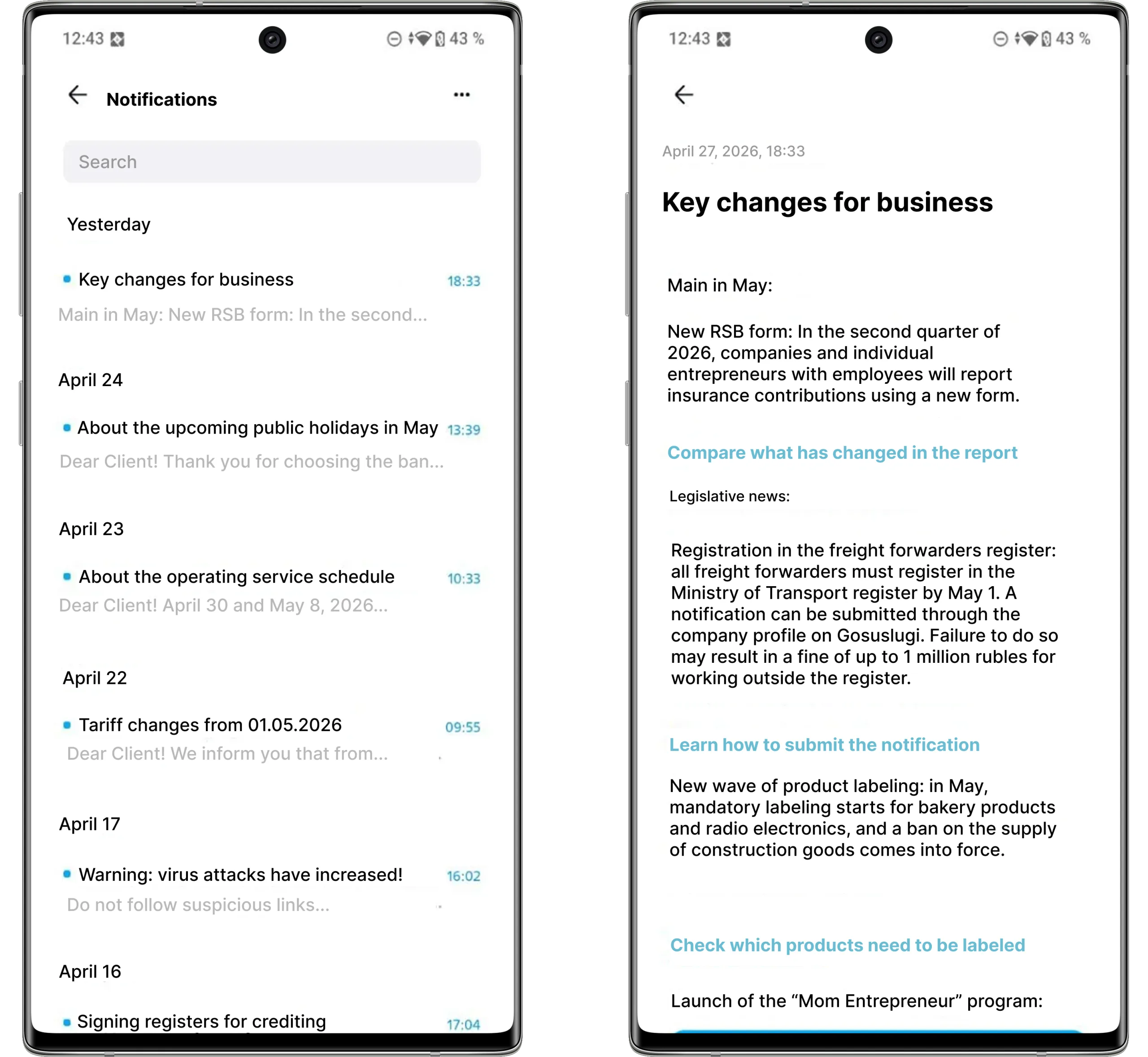

One of the benchmarked banks uses the notification section as an entry point for informing business clients about legislative and regulatory changes. On the main screen, the notification icon shows unread messages, helping draw attention to important updates. Inside the notification, the bank gives a structured summary of key changes and provides links to additional materials where the user can study the topic in more detail.

The value of this pattern is that the bank does not leave the entrepreneur alone with external changes. Instead of simply publishing news somewhere outside the product, it brings relevant information into the mobile banking flow and makes it easier for the user to understand what has changed.

However, the next step for banks is to connect such communication with action. The strongest version of this scenario would not only explain the change, but also guide the user to a relevant calculator, form, consultation, tax settings, or product scenario.

Insight: business users do not need more notifications — they need timely, relevant, and actionable explanations.

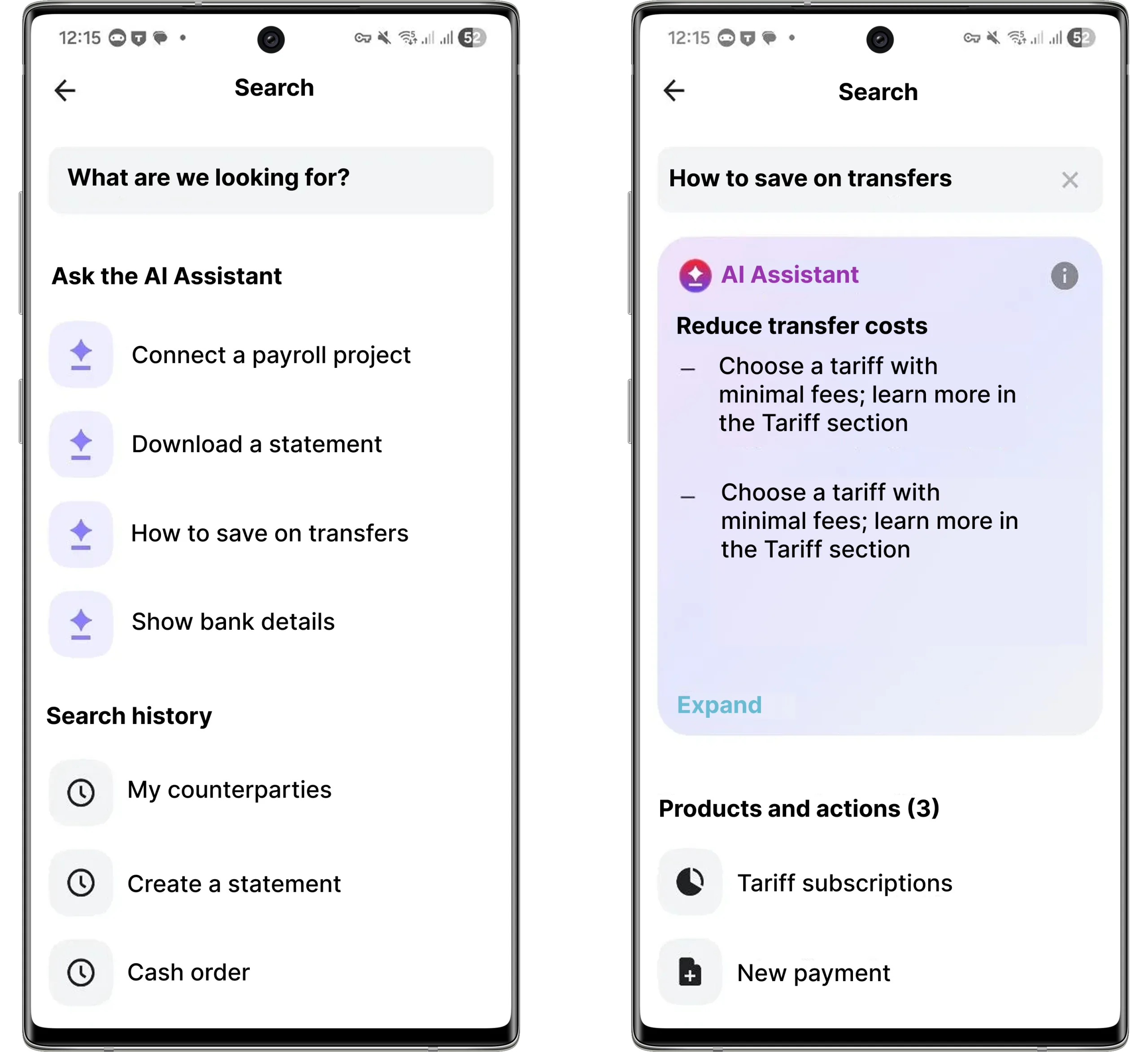

Another benchmarked bank integrates an AI assistant directly into the search experience. The user can enter a free-form question, and the system returns practical recommendations with direct links to relevant sections and actions.

This changes the role of search in business mobile banking. Instead of forcing the user to know the exact name of a section or function, the bank allows them to describe the task in natural language. For example, the user can ask how to reduce transfer costs, download a statement, or find a specific business service — and receive a guided answer.

The value of this pattern is especially high in business banking, where products are more complex than in retail banking and users often come with practical tasks rather than clear navigation queries.

Insight: AI becomes useful not when it exists as a separate chatbot, but when it helps users complete real business tasks inside existing scenarios.

As business banking becomes more digital, user expectations grow faster than basic functionality. Entrepreneurs already expect payments, balances, cards, and statements to work smoothly in mobile. The next question is whether business mobile banking UX can help them solve broader business tasks: choose a product, understand conditions, manage access, react to changes, or complete a service scenario without unnecessary friction.

This creates a direct business opportunity for banks. A mobile bank for business can include dozens of products and services — from payments, cards, deposits, and credit to acquiring, accounting, currency operations, documents, support, and ecosystem tools. Each of these areas can become a source of growth if the user can easily discover the service, understand its value, and activate it in the right context.

The strongest growth points usually appear where three factors meet:

Business Mobile Banking Rank 2026 helps banks compare business banking services by the quality of digital experience and identify growth points in their own product.

The research helps identify where competitors are creating stronger scenarios, what gaps in user experience can be turned into opportunities, and what market practices can be replicated to reduce time to market and uncertainty in product decisions.

The system helps banks:

As a result, the report becomes a benchmark and a practical tool for product decisions. It helps teams understand which scenarios matter most for business clients, where to prioritize improvements, and how to develop mobile banking as a stronger driver of engagement, transactional activity, product usage, and long-term client value.

Contact us via WhatsApp, send an email, or fill out the form below to learn more.

We’ve evolved dozens of successful financial services and are eager to prove that our expertise can be implemented in other industries and around the world. Have a look at our success stories!

From research and analysis to strategy and design, we help our clients successfully reach their customers through digital services.