In digital banking, customer experience has always been about convenience, speed, and security. But as user expectations evolve, these basic attributes are no longer enough. Customers increasingly expect banks to understand their context — not just what they are doing, but why they are doing it, and what they might need next.

AI makes this possible. By combining behavioral data, transaction history, and real-time signals, banks can move beyond generic personalization toward truly contextual experiences. Instead of sending broad offers or scripted notifications, they can anticipate needs, adapt to user intent, and deliver relevant solutions at the right moment.

This shift is not just a technological upgrade. It represents a new frontier in customer experience — one where banks transform from service providers into proactive partners in their customers’ financial lives.

At Markswebb, we’ve observed this evolution across dozens of mobile banking and investment platforms in Europe.

Contents

Most banks today focus on personalization at the surface level. They use customer segments, demographic profiles, or spending categories to recommend products and services. While these approaches create some relevance, they rarely capture the real-time context in which customers make decisions.

For example, a bank might offer a travel credit card because a customer purchased airline tickets last month. But without contextual awareness, the timing and value of such offers often feel generic or even intrusive.

At the same time, digital channels are saturated with notifications, promotions, and automated messages. Customers have become selective about what they engage with, rewarding only those experiences that feel immediately useful and relevant. This creates pressure for banks to move from static personalization to dynamic, context-driven experiences powered by AI.

In practice, only a few global banks have taken meaningful steps in this direction, mostly through pilot projects involving AI-based assistants, predictive credit offers, or intelligent fraud prevention systems. For most, contextual customer experience remains an aspiration rather than an embedded capability.

Artificial intelligence provides the tools to move beyond static personalization toward context-aware engagement. Unlike traditional systems that react only to past behavior, AI models can process multiple streams of data in real time:

By connecting these inputs, AI can identify not only what a customer is doing but also why they are doing it. For example, if a customer transfers money internationally late at night, AI can recognize urgency and adapt the experience — reducing steps in the flow, prioritizing speed, and offering tailored exchange rate information.

AI also enables anticipatory services. Instead of waiting for users to search for credit options, the system can detect early signals of financial strain (e.g., unusual overdraft frequency) and suggest pre-approved solutions before the problem escalates.

In this way, AI turns contextual awareness into a continuous dialogue, where the bank’s role shifts from passive responder to active financial partner.

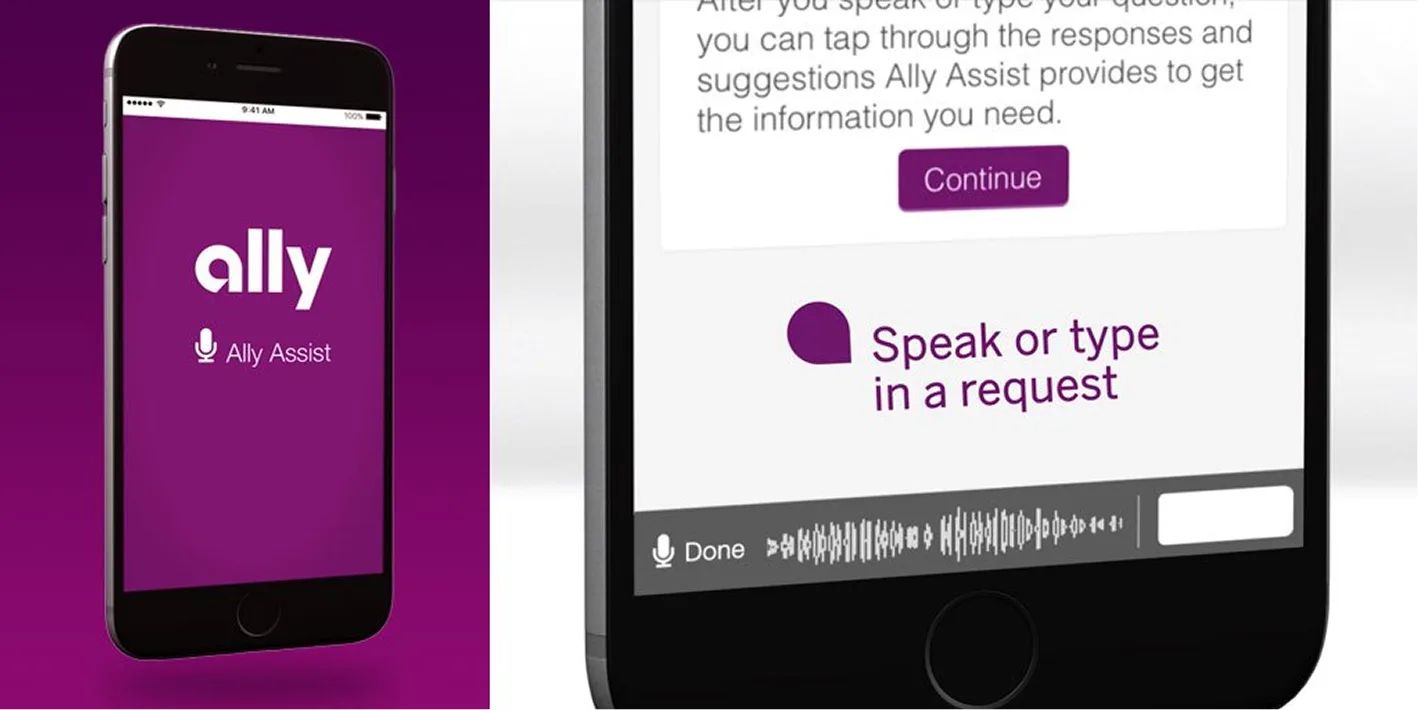

Why it matters: Gives customers quick access via voice or text and anticipates needs based on real behavior—boosting convenience and relevance.

Best practice: Ally Assist, available through the mobile app and Amazon Alexa, provides users with information on balances, payments, and transactions based on real behavior — the system “understands” what you need before you even ask.

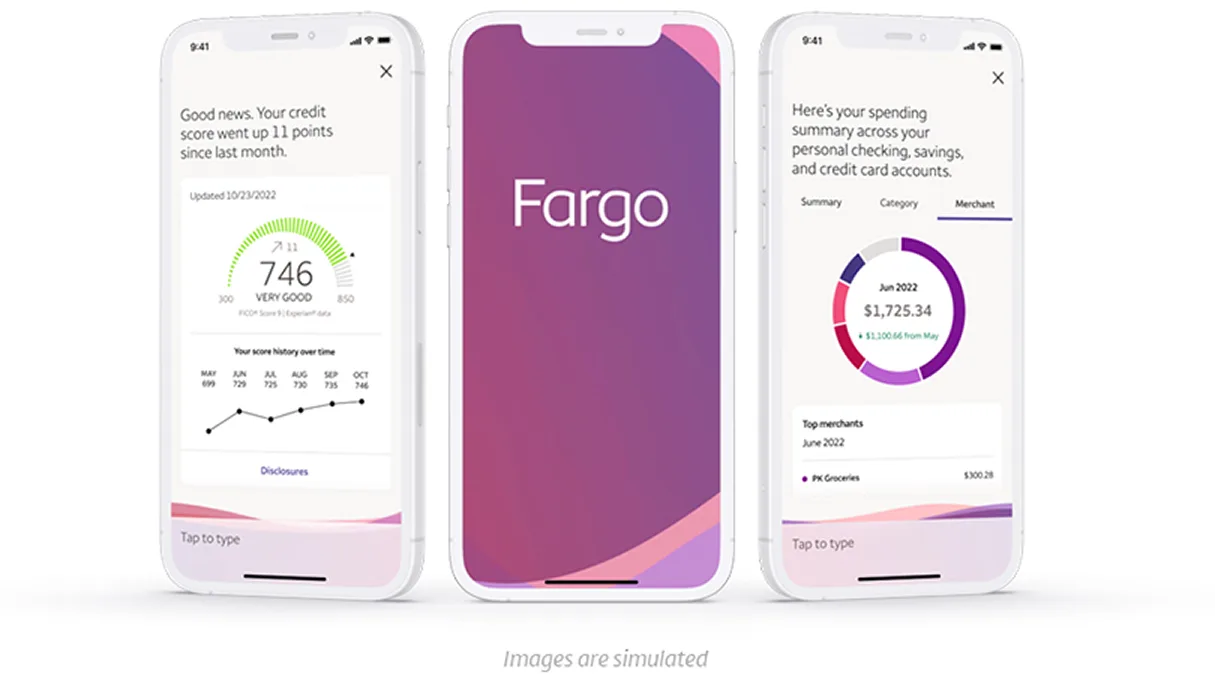

Why it matters: High-volume AI assistants must maintain accuracy and compliance while delivering personalized experiences.

Best practice: Wells Fargo’s AI assistant Fargo already handles more than 245 million customer interactions annually, delivering personalized and secure service at scale.

Why it matters: Customers overwhelmed by fraud reporting can benefit from faster, more intuitive AI-powered help—restoring trust and reducing friction.

Best practice: NatWest uses generative AI from OpenAI to enhance its Cora chatbot and the internal assistant AskArchie. As a result, customer satisfaction has increased by 150%, while urgent calls have significantly decreased.

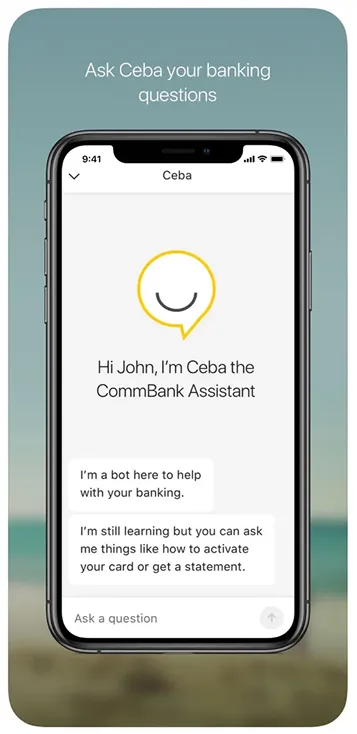

Why it matters: Natural language AI in chat and messaging frees customers from waiting and makes service accessible at the moment of need.

Best practice: The Commonwealth Bank of Australia processes around 50,000 messages per day with AI. The system provides context-aware responses in chat while simultaneously detecting and blocking suspicious transactions, enhancing both convenience and security.

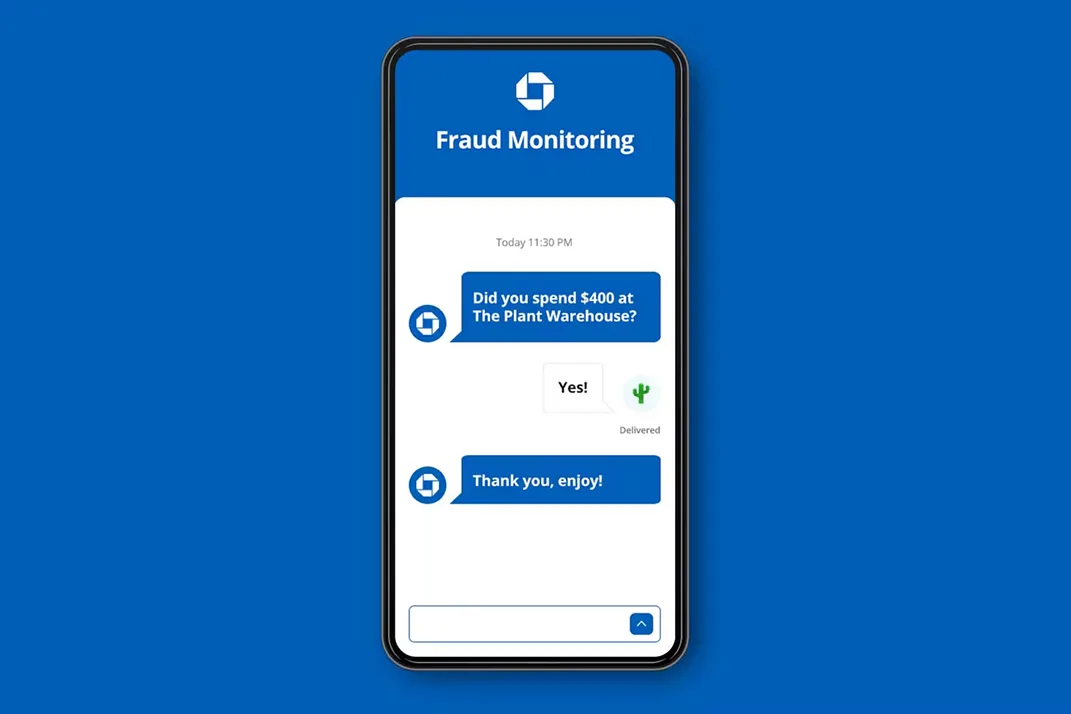

Why it matters: Simple, easy-to-understand notifications help users feel in control rather than threatened.

Best practice: JPMorgan Chase instantly sends alerts such as “Did you just authorize a $900 payment at X?” and allows customers to confirm or block the transaction with a single tap—delivering both security and a seamless experience.

Why it matters: Major life events such as buying a home, traveling, or pursuing education create new financial needs. AI helps anticipate these needs through transaction data and life-event signals.

Best practice: Research shows that banks applying micro-personalization tied to life events and personal goals achieve a 20–30% increase in cross-sales and boost customer satisfaction by more than 25%.

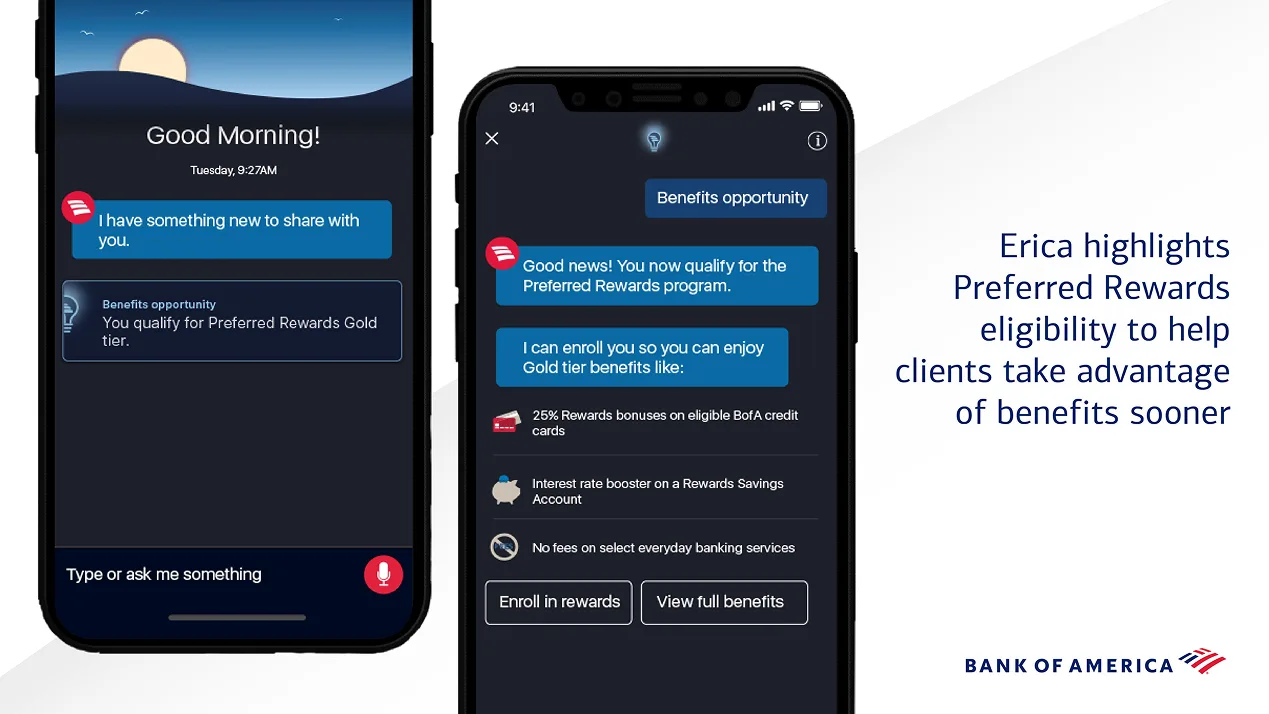

Why it matters: Customers benefit from timely, personalized alerts that help them avoid unexpected charges, stay informed, and feel supported—this builds trust and enhances the usefulness of digital banking.

Best practice: Bank of America's virtual assistant Erica has delivered over 1.7 billion proactive, personalized insights. It provides cash-back deal suggestions based on spending, weekly balance trend forecasts, notifications about eligibility for rewards, and investment guidance across nearly 50 topics. Over 18.7 million hours of interaction and a >98 % success rate in delivering relevant information significantly reduce pressure on call centers.

The future of AI-powered contextual customer experience in banking will be defined by three parallel shifts:

Looking ahead, AI will no just automate banking—it will redefine the emotional contract between banks and their customers. Trust will depend less on traditional reputation and more on whether the digital service feels intuitive, supportive, and contextually relevant at every touchpoint.

If you would like to gain access to more valuable best practices and see how they can be applied to your specific business challenges, you can reach out to us. At Markswebb, we provide a dedicated best practice research service that helps banks and fintechs discover, evaluate, and implement solutions proven to work in international markets.

AI-powered contextual customer experience marks a decisive shift in the role of digital banking. Instead of acting as transaction processors, banks are becoming intelligent companions—anticipating needs, guiding decisions, and embedding themselves into the daily lives of customers.

The opportunity is clear: when services feel timely, relevant, and transparent, customers respond with higher engagement, stronger trust, and long-term loyalty. Yet success will depend on how well banks balance advanced data-driven capabilities with ethical design and clear communication.

For decision-makers, the next frontier is not about adopting AI for the sake of efficiency, but about designing experiences where context creates value—where every interaction feels less like a service request and more like meaningful support.

We respond to all messages as soon as possible.

We’ve evolved dozens of successful financial services and are eager to prove that our expertise can be implemented in other industries and around the world. Have a look at our success stories!