Contents

For years, fintech products competed by making basic operations easier: faster transfers, smoother onboarding, clearer card screens, simpler product applications. But in mature digital banking markets, these improvements are quickly copied. Users no longer reward a bank for having an app that works. They expect it.

This creates a new product question: what makes a user return when the core experience is already digital, fast and familiar?

For digital banking customer retention, the next advantage comes from helping users act with more confidence. The product should explain what matters now, connect separate actions into clear journeys and support the customer before a problem turns into a request.

Markswebb research across digital banking, SME banking, investment apps, savings products and insurance services shows that retention increasingly depends on four capabilities:

This article explores recurring UX problems behind weak customer engagement in digital banking and shows best practices that help banks build retention after the basic experience has become “good enough.”

The cost of this shift is practical. When users treat a banking app as a utility, the product gets fewer return moments, fewer cross-sell opportunities and less space to shape financial behavior. Even a small improvement in retention can have a strong business effect: Bain & Company’s widely cited research shows that a 5% increase in customer retention can increase profits by 25% to 95%.

A mature banking app cannot be only a transaction interface. If the product waits until the user opens it with a specific task, it loses opportunities to create frequency, prevent problems and show value.

Retention grows when the app becomes proactive: it notices a relevant moment and brings the user back with a useful reason.

In SME banking, proactive mechanics are especially valuable around taxes, limits, incoming payments, cash flow and document deadlines. For example, Markswebb identified practices where banks show progress toward tax or revenue thresholds, warn about upcoming limits and guide entrepreneurs to the next action before the issue becomes urgent.

In insurance and broader fintech trendwatching, the same logic appears in risk alerts, renewal reminders, prevention flows and personalized prompts tied to the user’s actual product.

The product should create return moments around meaningful financial events, not around generic notifications.

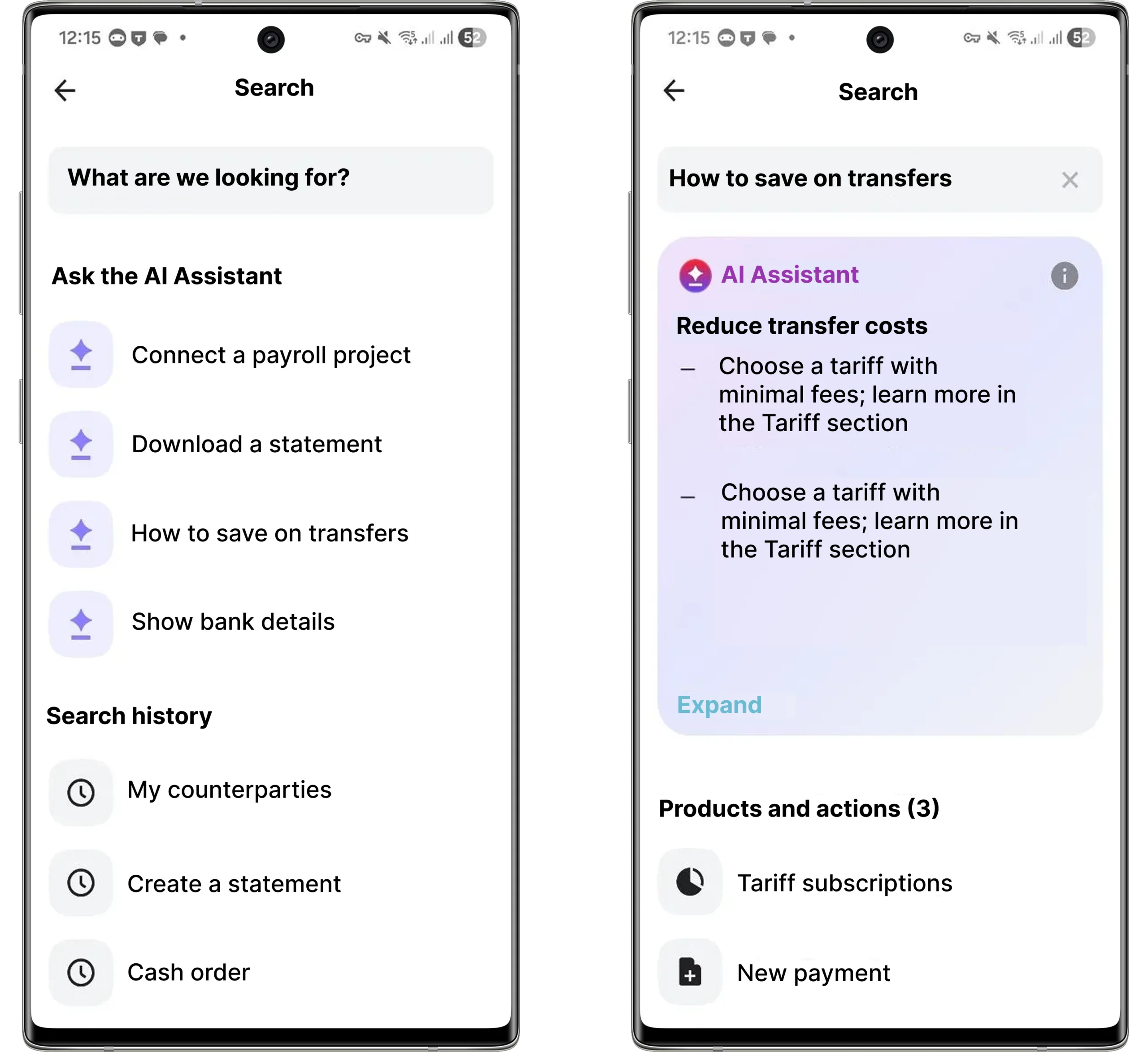

In mature fintech products, conversion and retention often break not because the user cannot complete an action, but because they do not understand whether the action is worth taking.

This is especially visible in investments, deposits, credit products, insurance and SME services. Users need context: expected benefit, cost, risk, restrictions, timing and alternatives.

In European investment apps, leading services do more than provide access to assets. They help users compare instruments, understand portfolio structure, assess risk and connect actions with long-term goals. In savings and deposits, strong practices explain yield, conditions and the effect of user behavior on the final result.

Retention grows when users feel that the product helps them make better decisions, not simply complete more transactions.

Many fintech apps have strong individual features but weak continuity between them. A user can pay, open a product, contact support or read a notification, but these actions often remain disconnected.

When journeys are fragmented, the product becomes a utility. The user opens it only when necessary and leaves as soon as the task is complete.

Markswebb projects repeatedly show that stronger products connect steps into a scenario: from notification to explanation, from explanation to action, from action to status tracking, from status tracking to support if needed.

In business banking, this is critical for payments, documents, employee access, limits, cash operations and foreign trade scenarios. In support, the key issue is whether the chatbot or assistant keeps context and transfers it to a human without forcing the user to repeat the problem.

A retention-oriented product does not optimize screens separately. It connects them into journeys that reduce repeated effort.

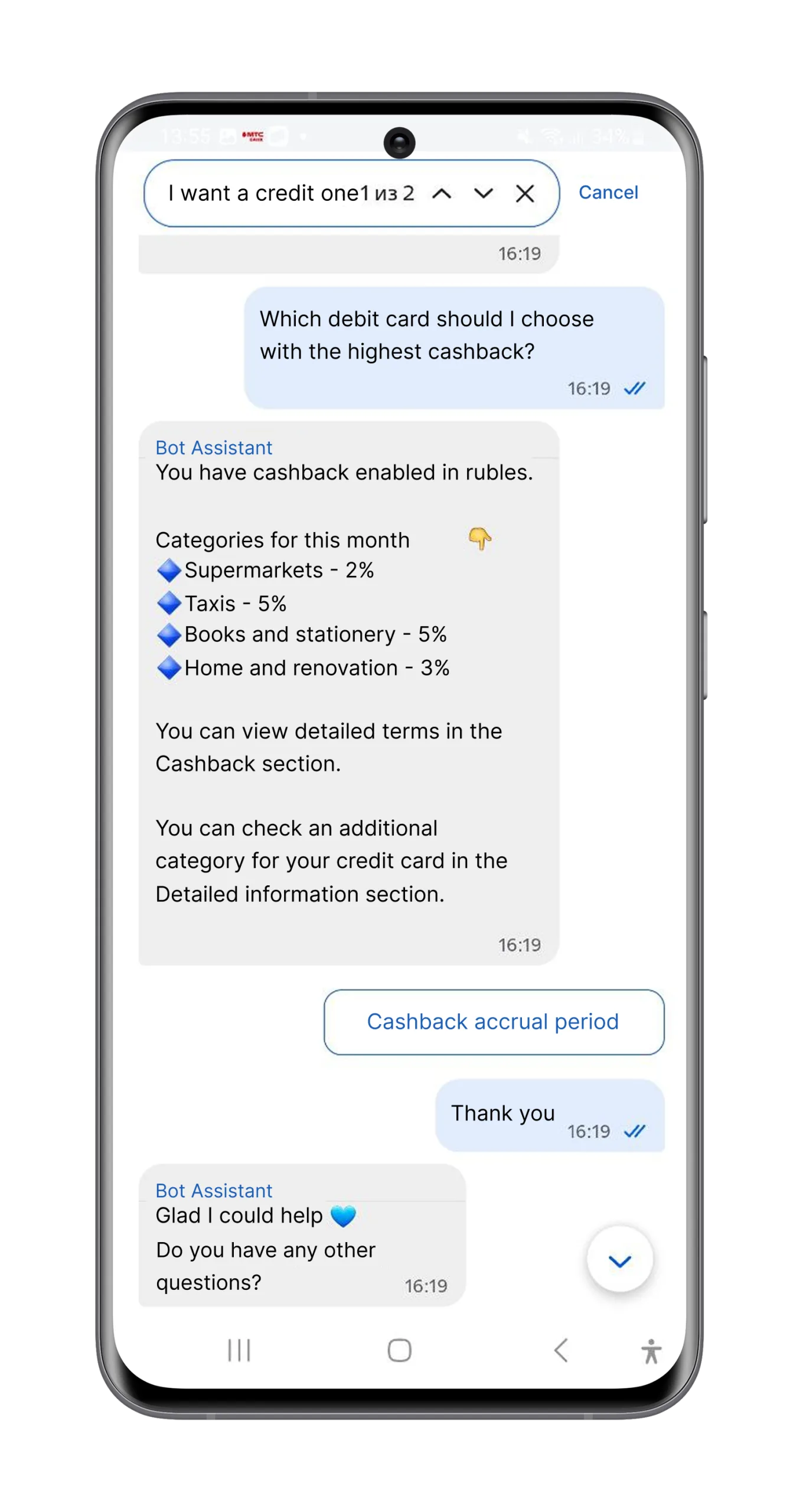

Fintech products collect enough data to personalize the experience, but many still use personalization mainly for offers. This can increase short-term conversion, but it does not always build trust.

In financial products, personalization must feel useful and explainable. Users are more likely to return when recommendations are linked to their situation and framed as help, not pressure.

In SME banking, personalization can be based on business type, tax system, revenue, connected products and current tasks. In investments, it can reflect the user’s portfolio, horizon and risk profile. In insurance, personalization can appear through product-specific reminders, family scenarios, risk prevention and renewal logic.

The strongest personalization does not ask the user to buy more. It helps the user understand what matters now.

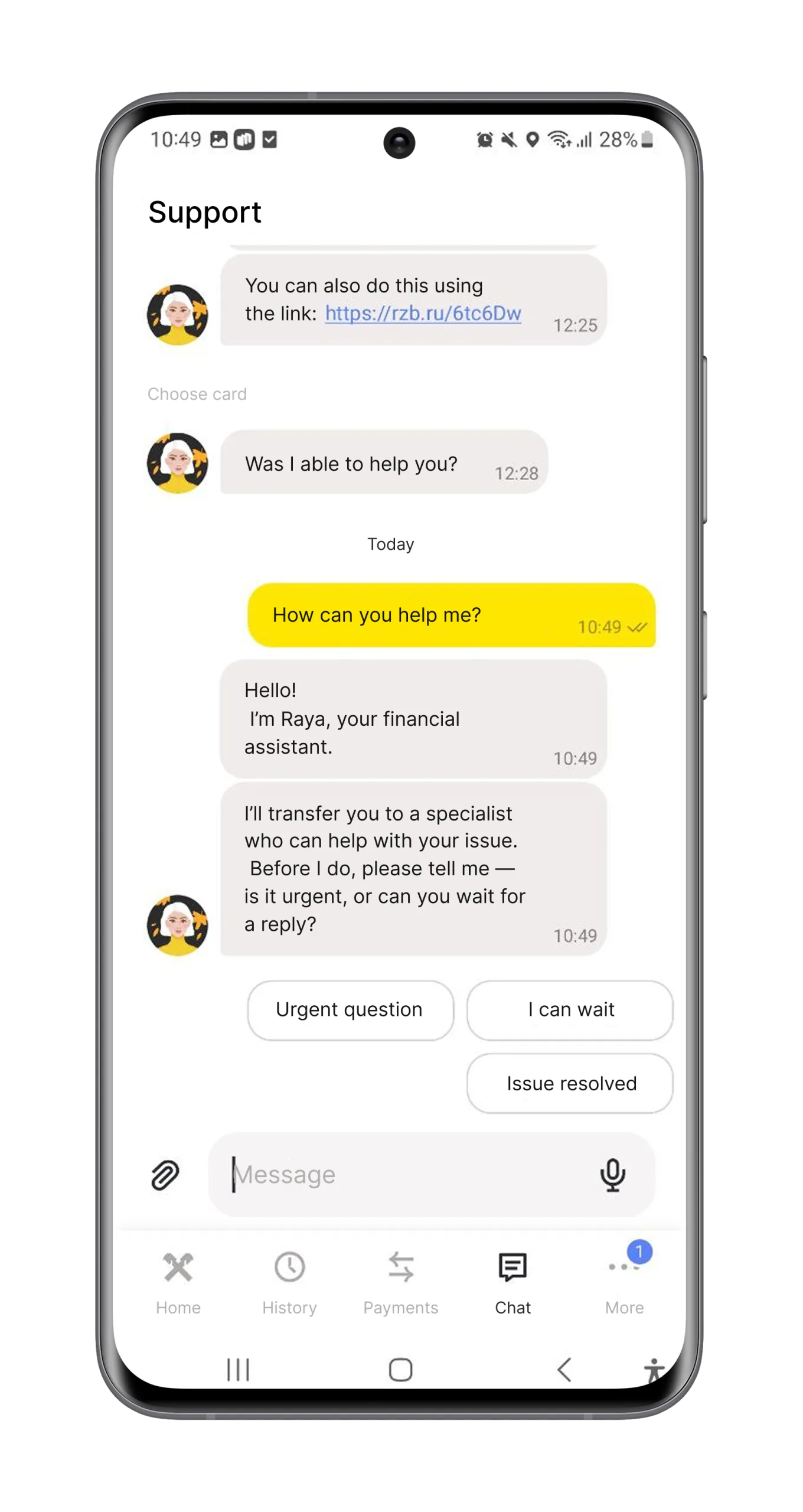

When basic UX is good, support moments become even more important. Users remember not only whether the app worked, but what happened when something went wrong.

A weak support journey can destroy trust quickly: the user repeats the issue, resends documents, waits without status, or receives generic answers that do not solve the problem.

Markswebb can show that support quality in digital banking depends on task completion, context preservation, escalation logic and transparency. The strongest practices reduce the need for support, but also make support more effective when it is needed.

Support is not separate from retention. It is one of the moments where the product either confirms trust or loses it.

When digital banking UX becomes a commodity, fintech products need a different retention strategy. The goal is no longer just to remove friction from basic actions. The goal is to make the product more useful between transactions.

The strongest products create reasons to return because they:

Markswebb research across Eastern European digital banking shows that the next competitive layer is not more functionality. It is the ability to turn financial complexity into clear, timely and confident user action.

Get in touch via WhatsApp or email to build a practical UX roadmap for customer engagement and retention.

We respond to all messages as soon as possible.

We’ve evolved dozens of successful financial services and are eager to prove that our expertise can be implemented in other industries and around the world. Have a look at our success stories!