Contents

European investors are no longer a niche group — they are a broad, behaviorally diverse audience shaped by macroeconomic pressure and growing digital autonomy. Inflation and declining trust in pension systems are pushing more users toward digital investment products and services, accelerating the shift from passive saving to active investing.

For many investors across Europe, this shift is as much behavioral as financial. Users expect digital investment products and services to support real-life decisions — not just provide access to assets. This growing complexity of the market is also reflected in tools like the EU Digital Investment Map, which shows how fragmented and diverse the European investment landscape has become.

With lower barriers to entry and platforms like Revolut and Interactive Brokers embedding investing into everyday routines, the audience now ranges from beginners to experienced users.

For product teams, designing for an “average user” is no longer viable. Today’s investment users are fragmented and highly context-driven, making behavioral understanding critical for building competitive digital investment products and services.

The behavior of the European investor has shifted from passive financial management to active, continuous interaction with financial tools. This is not just a change in preferences — it is a change in how financial decisions are made on a daily basis. As a result, investment platforms are no longer evaluated only by functionality or market access. They are judged by how well they support real user actions: entering the market, making decisions under uncertainty, and managing investments over time.

For a growing share of users, investing no longer begins with complex strategies or deep financial knowledge. It starts with simple, ready-made instruments that allow immediate participation in the market. This makes investing feel closer to saving — predictable, accessible, and repeatable.

For the European investor, this shift redefines expectations. Financial products are no longer divided into “simple” (savings) and “complex” (investments). Instead, all products are expected to provide a comparable level of clarity and ease of use.

For modern investing experiences, this means:

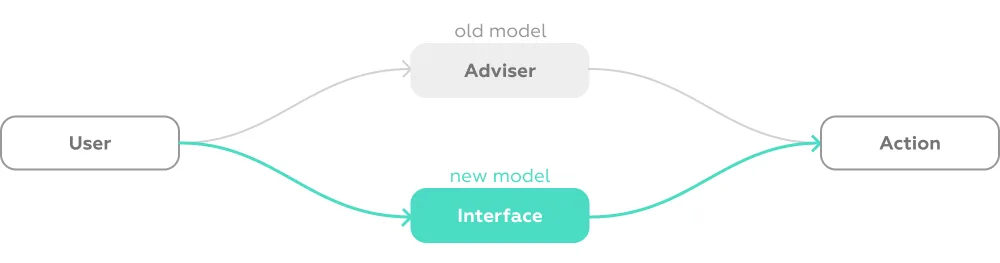

Modern European investors increasingly makes decisions independently, without relying on advisors or external guidance. This does not mean users are more confident — it means they expect the product itself to provide the necessary support

This fundamentally changes the role of investment platforms. The interface is no longer just a place where transactions happen — it becomes the primary environment where decisions are formed.

Users expect the product to:

If the product does not provide this support, users are forced to look elsewhere — or disengage entirely.

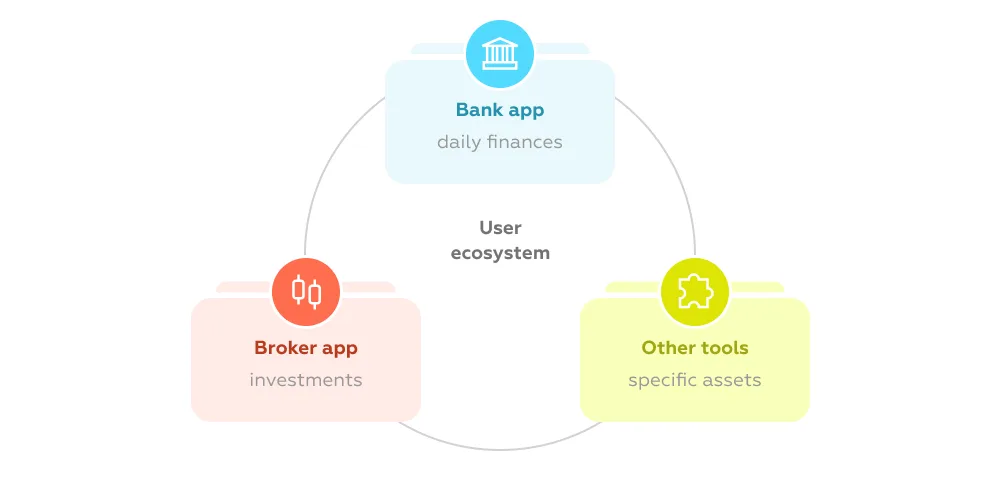

The European investor does not operate within a single ecosystem. Financial activity is distributed across multiple platforms, each solving a specific task: everyday banking, investing, or managing specific asset types.

This behavior creates a different competitive environment for investment apps. Users are constantly comparing experiences, even if they are not doing it consciously. Any friction, delay, or lack of clarity becomes immediately visible in contrast to other tools they use.

As a result:

Despite becoming more active, the European investor is not becoming more tolerant of complexity. On the contrary, expectations are shaped by simple, intuitive digital experiences outside of finance.

Users are willing to engage with financial products, but only if those products:

For digital investment products and services, this creates a clear constraint. Adding more features does not automatically increase value. If complexity is exposed too early or too broadly, it reduces engagement and creates hesitation.

The challenge is not to simplify the product itself, but to simplify how it is experienced — revealing complexity only when it becomes relevant.

The key shift is straightforward: the European investor does not need more functionality — they need better support in real scenarios.

They expect to:

For investing platforms, access to financial markets is no longer enough to differentiate.

The real competitive advantage lies in how effectively the product helps the European investing audience act — with clarity, confidence, and minimal effort.

The European investor is often grouped by age, income, or geography. But inside digital investment ecosystems, these labels quickly lose meaning. What actually shapes user behavior is not who the investor is — but how they think, decide, and act.

A behavioral lens reveals a more useful structure. Instead of static personas, we see distinct modes of interaction with financial products — each with its own expectations, pace, and tolerance for risk. These are not marketing profiles. They are patterns that directly translate into UX requirements.

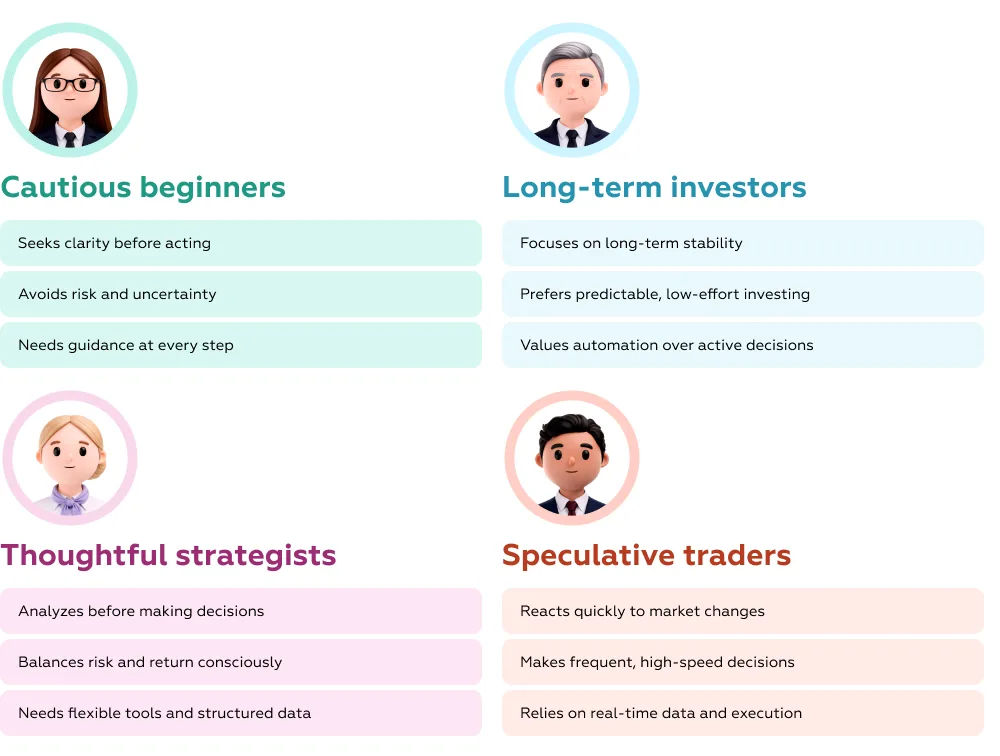

For this segment, investing starts with hesitation. These investors are not driven by opportunity, but by the need to avoid mistakes. Every step is evaluated carefully, and even small decisions can feel significant.

They tend to:

This changes how investing services should behave. The first experience is not about enabling action — it is about reducing doubt. Interfaces need to explain what is happening in plain terms, show outcomes before committing, and make every step feel safe and reversible.

If the product feels even slightly unclear at the beginning, these users do not explore further — they leave.

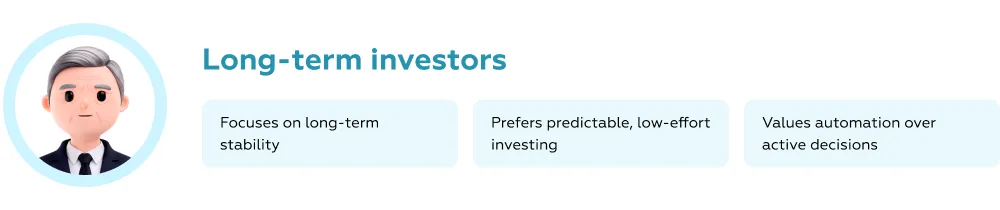

This group approaches investing with patience and structure. The investor here is not trying to react to the market, but to build a stable financial trajectory over time.

Interaction is less frequent, but expectations are no lower. These users want to feel that the product is working for them in the background, without requiring constant attention.

What matters most:

For digital investment services & products, this creates a different kind of challenge. The experience should not push for constant interaction, but it should still provide a sense of control. The product becomes a long-term companion, not a tool for immediate action.

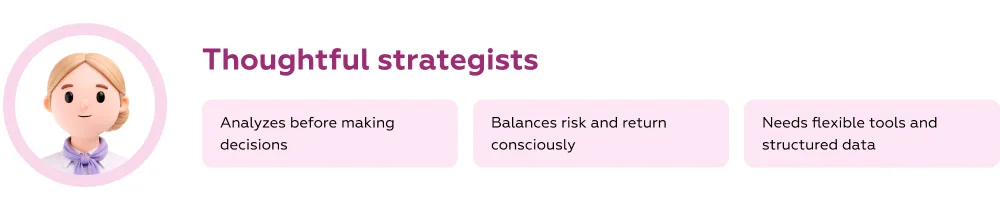

This segment sits in the middle — active, but deliberate. The investor portrait here is engaged in decision-making, but not impulsively. Actions are preceded by comparison, reflection, and an attempt to understand trade-offs.

These users move through the product with intent. They explore options, evaluate scenarios, and expect the interface to support thatprocess.

For fintech investment products, this means:

Too little information feels limiting. Too much feels chaotic. The product has to find a balance — offering depth without losing clarity.

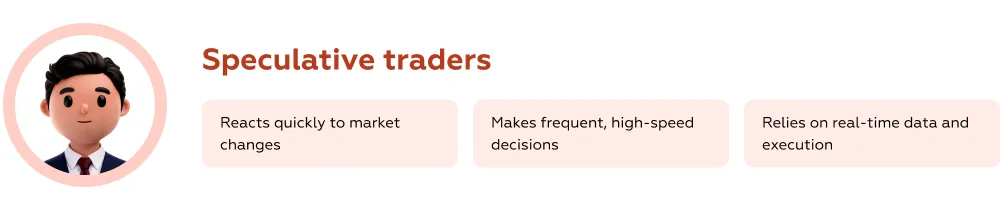

At the opposite end, the European investor in this segment is driven by speed and opportunity. Decisions are made quickly, often in response to market signals, and the product is used as a real-time execution tool.

Here, the experience is defined by momentum. Any delay breaks the flow, any friction becomes visible.

These users expect:

For digital investing platforms, performance becomes part of the experience. The interface should stay out of the way, allowing users to act without hesitation. Even small inefficiencies can push them to alternative platforms.

There is no single “default” European investor anymore. What looks like one audience from the outside is, in reality, a set of very different behavioral patterns.

Some users need reassurance before they act. Others need speed. Some expect guidance, while others expect control.

For digital investment products and services, this creates a fundamental constraint: a single, uniform experience will always fall short.

Products either adapt to these differences — or implicitly choose which segment they serve best.

In both cases, understanding behavior is no longer optional. It becomes the starting point for every product decision.

Behind the diversity of segments, the investor portrait is shaped by a common set of pressures. These are not isolated trends — they define how users think, what they expect, and why they act the way they do inside investing services.

Understanding these drivers is critical. They explain not only what users do, but why they hesitate, abandon, or stay engaged.

For many users, investing is no longer about growing wealth — it is about protecting it. The European investor increasingly treats investing as a response to uncertainty rather than an opportunity for gain.

This shifts the emotional context of interaction:

Inside digital investment products, this translates into a need for clarity. Users want to understand how their money behaves in real terms — not just returns, but outcomes under changing conditions.

Confidence in long-term institutional solutions is weakening. The investor in Europe is gradually moving from relying on external systems to building personal financial strategies.

This does not mean users feel more confident — it means they feel more responsible.

As a result:

For investment ecosystems, this creates a new role: supporting ownership. The product must make users feel in control, even when decisions are complex.

Investing is no longer a one-time learning curve. The European investor learns continuously, often in parallel with using the product.

But learning is not a separate activity. It happens inside the interface, during real actions.

This creates a specific expectation:

If learning requires leaving the product, the experience breaks. Digital investment need to embed knowledge into interaction itself.

Even experienced users experience uncertainty. The European investor in 2026 often operates under emotional pressure — reacting to market volatility, news, or personal financial concerns.

This affects behavior in subtle ways:

For services, reducing stress becomes as important as enabling action. The product should help users feel confident in their decisions, not amplify anxiety.

Regulatory complexity remains one of the least intuitive parts of the experience. The European investor often faces with unclear tax implications, reporting requirements, and region-specific rules.

This creates a disconnect:

For digital investment products and services, this is a hidden UX problem. If outcomes are unclear, trust erodes — even if the interface itself is well designed.

Simplifying how regulations are communicated becomes part of the product experience, not just a legal necessity.

Despite the growing sophistication of financial tools, the investor consistently prioritizes clarity over depth.

Users do not reject advanced features — they reject unnecessary complexity.

What they expect:

For investment platforms, this means that adding functionality without improving comprehension reduces overall value.

While ESG is widely discussed at the institutional level, it plays a secondary role for many users. The European investor today may express interest in sustainable investing, but rarely prioritizes it over performance, simplicity, or cost.

This creates a gap between positioning and behavior.

For digital investment products, the implication is pragmatic:

These patterns point to a single conclusion: the European investor operates under constant cognitive and emotional load.

They are:

The goal for investment sevices is not to provide more information or more functionality.

The goal is to reduce uncertainty.

A product that succeeds does three things well:

When this happens, the experience stops feeling like a risk — and starts feeling like something users can rely on.

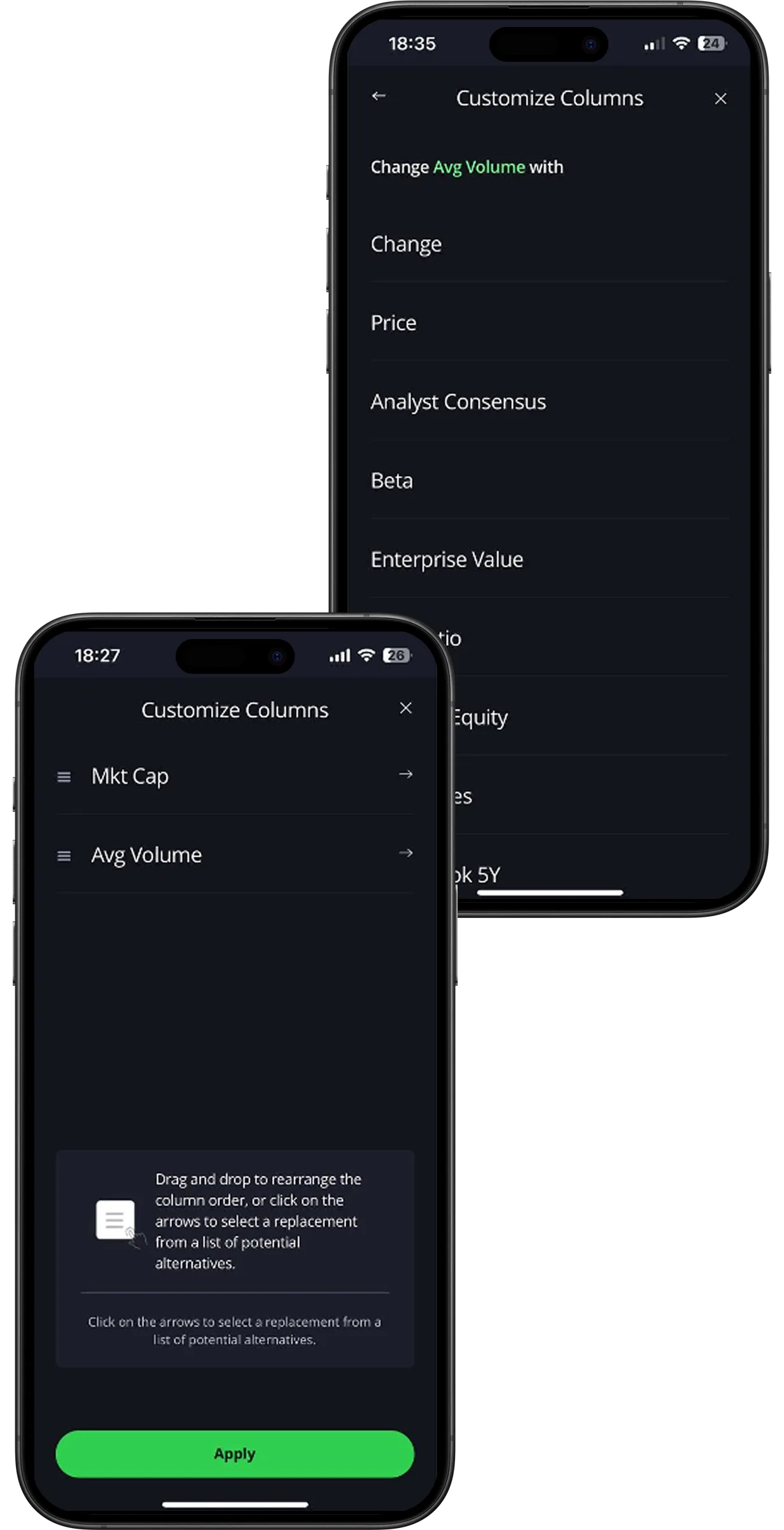

This segment expects more than access to data — they expect structure. The European investor here needs tools that turn information into decisions.

What matters is not how much data is available, but how usable it is.

Customizable analytics instead of static data

Platforms like eToro allow users to build their own analytical workspace — selecting metrics, rearranging columns, and saving configurations. This shifts the experience from browsing to active analysis.

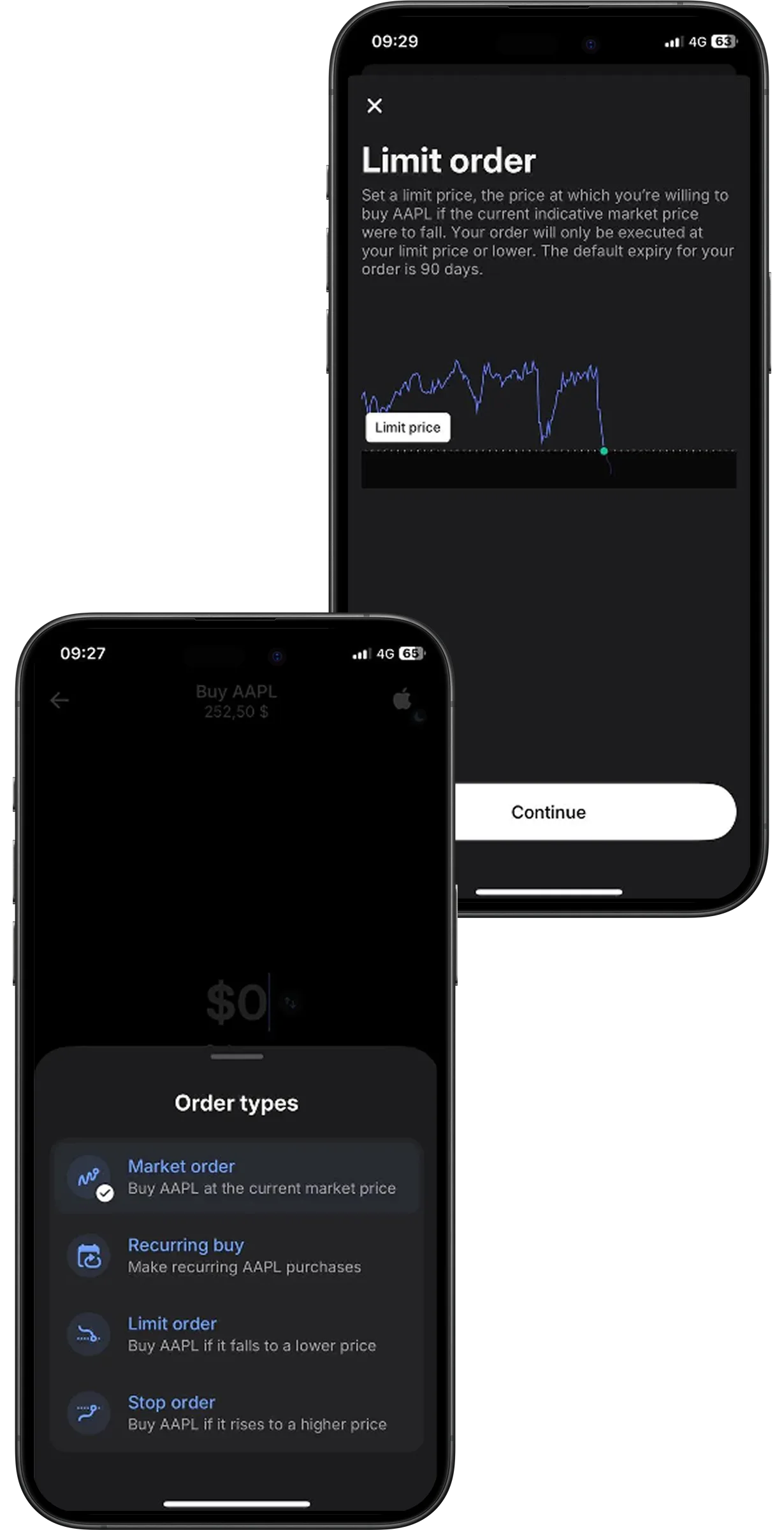

Embedded explanations at the moment of action

Revolut integrates short explanations of order types directly into the transaction flow. Users understand options instantly, without leaving the scenario.

Adding interpretation, not just data

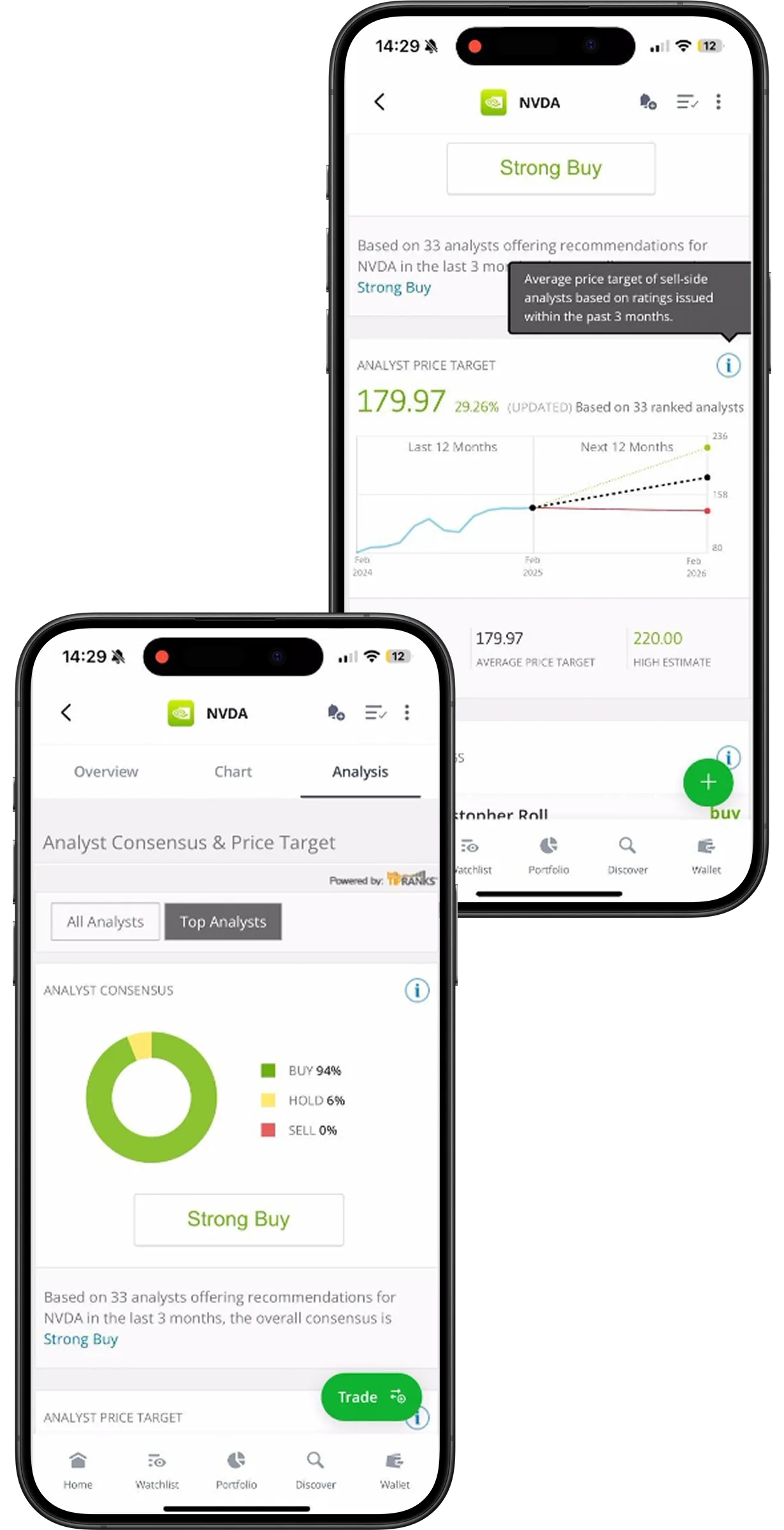

In asset views, eToro provides analyst consensus, recommendation distribution, and target price ranges. This helps users move from raw data to informed judgment.

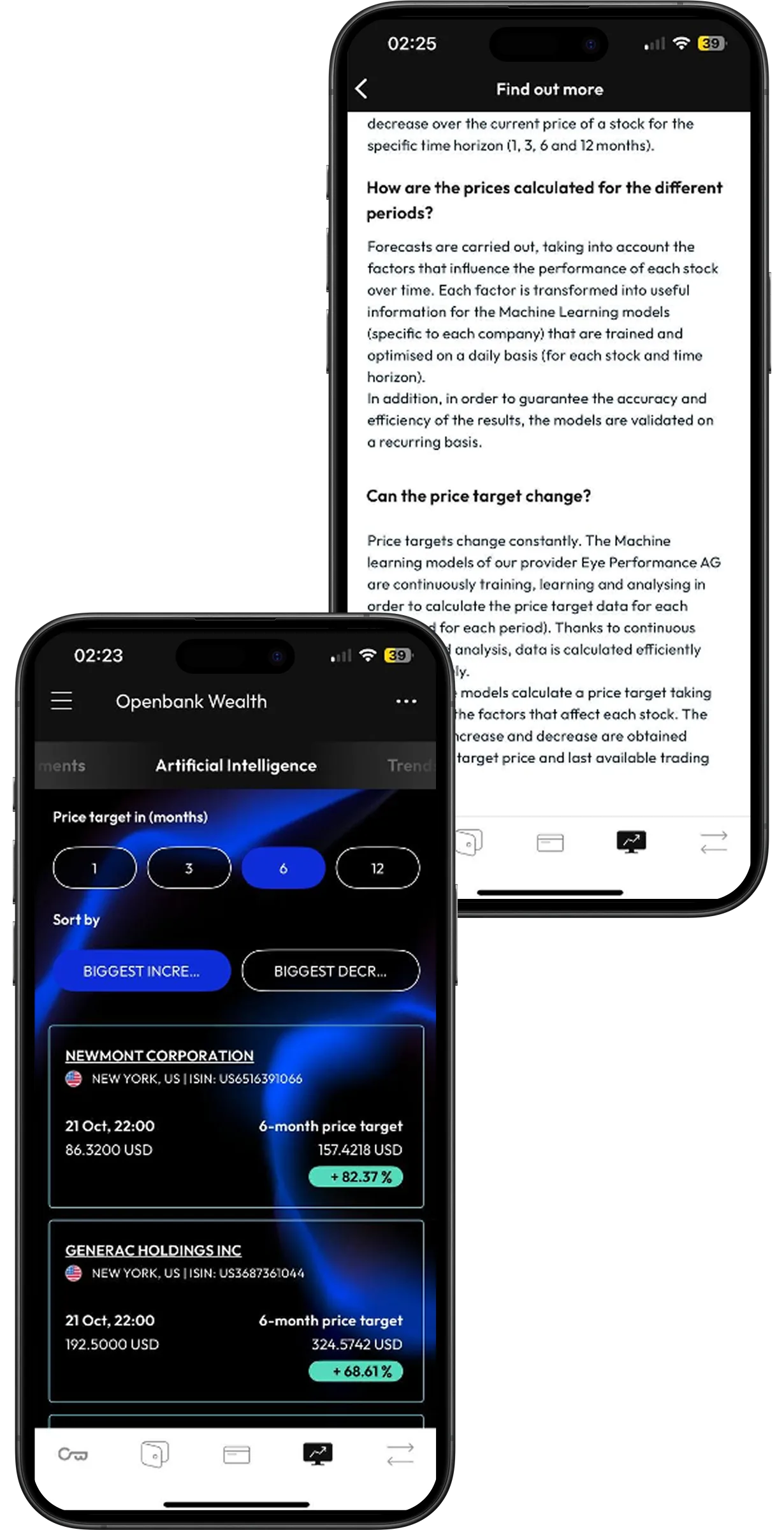

Translating signals into future scenarios

Openbank shows AI-based forecasts across multiple time horizons, turning complex market signals into clear expectations.

Across these examples, the pattern is consistent:

flexibility creates control, clarity builds confidence, and interpretation enables decisions.

Regardless of segment, every European investor faces the same structural challenges in products for investing:

These challenges shape how users interact with products and where most experiences still break.

We will explore each in detail in the next articles — based on insights from the upcoming State of Digital Investment in Europe study.

For services, the focus shifts from adding features to making them usable in real scenarios.

Product teams should prioritize:

These principles help align the product with how the investor in Europe actually makes decisions.

More detailed breakdowns will follow in upcoming articles based on SDIE insights.

There is no single European investor. What looks like one audience is a set of different behaviors — and digital investment ecosystems compete on how well they support them.

The advantage no longer comes from features. It comes from aligning UX with real scenarios: starting to invest, adjusting portfolios, reacting to changes.

Products that map to these moments feel natural — and win.

All of these insights, along with UX benchmarks and best practices, will be revealed in the upcoming State of Digital Investment in Europe study.

If you want early access and a competitive edge in building digital investment products and services for the investors in Europe, get in touch with our team via WhatsApp or email.

We respond to all messages as soon as possible.

We’ve evolved dozens of successful financial services and are eager to prove that our expertise can be implemented in other industries and around the world. Have a look at our success stories!