In 2026, growth in digital products is no longer constrained by traffic — it’s constrained by efficiency. Paid acquisition is still scalable, but its economics are tightening: rising ad costs and competition mean that simply “buying growth” no longer guarantees returns. According to McKinsey & Company, companies that focus on improving customer experience can achieve 2–3x higher revenue growth compared to peers. At the same time, research by Bain & Company shows that increasing retention by just 5% can boost profits by 25–95%.

The implication is clear: sustainable growth now depends less on acquisition volume and more on how efficiently products convert, retain, and monetize users.

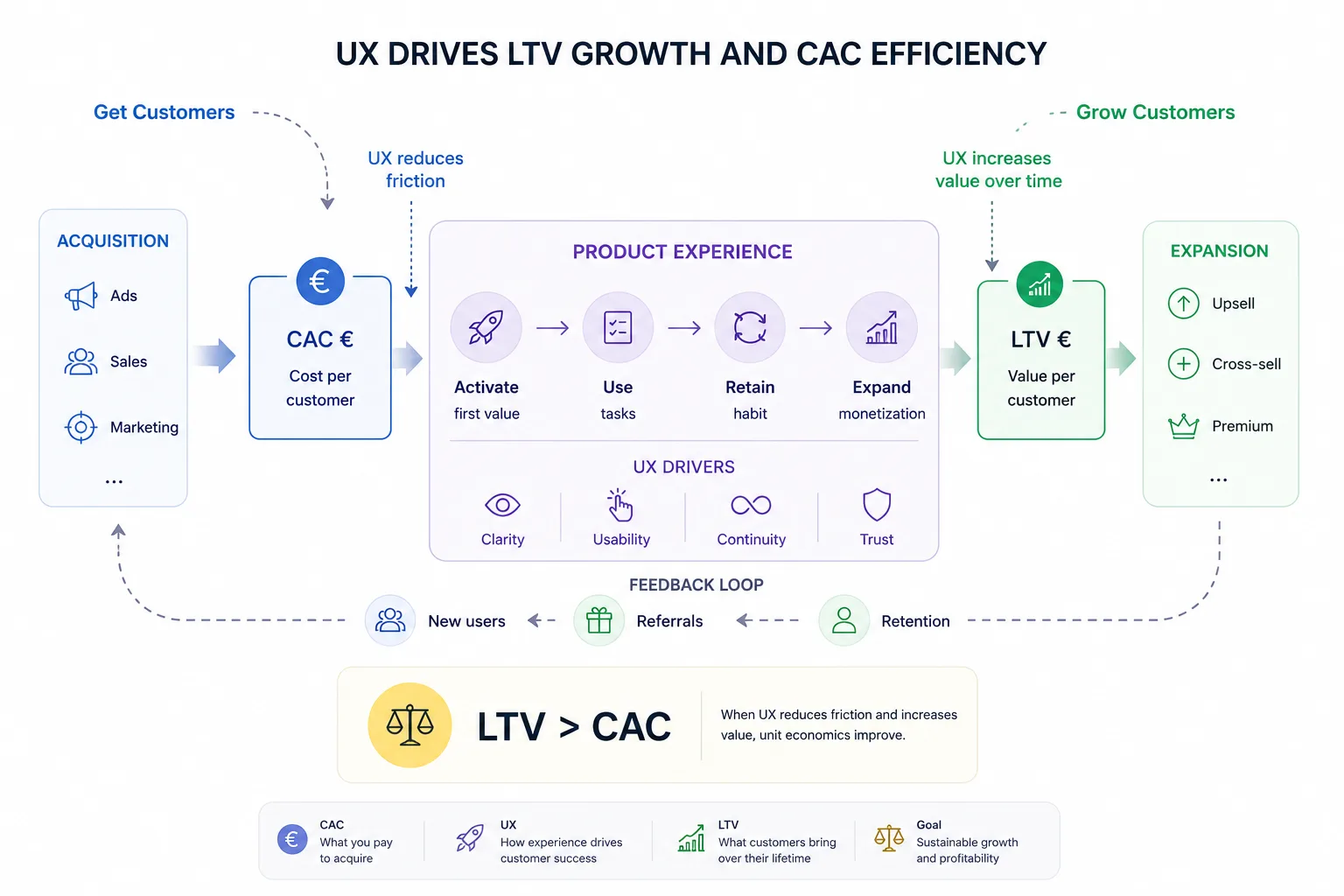

This is where LTV and CAC stop being isolated marketing metrics and become core product performance indicators. CAC reflects how efficiently a product turns interest into active users, while LTV reflects how well it keeps and grows them over time. Both are directly shaped by the quality of the experience users go through — not just in onboarding, but across every interaction.

In this article, we focus specifically on the UX impact on LTV and UX impact on CAC, showing how product experience defines unit economics in practice — from the first interaction to long-term retention, and ultimately, revenue expansion.

Contents

Customer Lifetime Value (LTV) is the total revenue a product generates from a customer over the entire period of their relationship. In simple terms, it answers: how much value does one user bring before they leave?

In enterprise digital products, LTV is not a single number — it’s a system of interdependent metrics: activation rate, usage frequency, feature adoption, expansion revenue, and churn. Small UX decisions across dozens of user scenarios compound into measurable differences in UX and customer lifetime value.

Customer Acquisition Cost (CAC) is the cost of acquiring a new customer — including marketing spend, sales effort, and onboarding resources.

In enterprise environments, CAC is primarily influenced by:

This is where UX and customer acquisition cost become tightly linked — because experience defines how efficiently users move through the funnel.

At a structural level, both metrics are shaped by four core drivers — but in enterprise products, each of them unfolds across dozens of user scenarios and touchpoints.

Activation is not just about sign-up. It’s about how quickly a user reaches first real value — whether they successfully complete a meaningful task and understand what the product can do for them. The shorter and clearer this path, the stronger the foundation for both UX impact on CAC and long-term value.

Retention is built through repetition. Users return not because they were acquired once, but because the product consistently helps them solve recurring tasks. In enterprise environments, this often means embedding into workflows — which directly defines UX and customer lifetime value.

Friction accumulates silently. Extra steps, unclear states, duplicated actions — each of these increases effort and reduces completion rates. Individually, they may seem minor; collectively, they shape drop-offs, slow down funnels, and weaken both conversion and retention.

Trust is what turns usage into revenue. Users need to understand what is happening, what it costs, and what to expect next. Without this, even a functional product struggles to monetize effectively — a critical aspect of UX impact on unit economics.

These drivers are widely known. The non-obvious part is this: UX is the layer where all four are either enabled or broken — at the level of specific interactions, not abstract strategy.

It may sound obvious, but in 2026 the relationship between UX and unit economics is no longer theoretical — it is measurable, trackable, and increasingly decisive in competitive markets.

UX does not influence LTV and CAC indirectly — it operates through concrete mechanisms inside the product. The impact becomes visible when you look at how users move through key scenarios.

Onboarding → conversion rate

The first experience defines whether users activate or drop off. Simplified flows, contextual guidance, and reduced cognitive load shorten time-to-value — directly improving UX and conversion rate optimization.

Clarity of value → lower acquisition cost

When users understand the product’s value inside the interface, the need for external explanation decreases. This reduces reliance on paid channels and sales effort — a core mechanism behind how UX reduces customer acquisition cost.

Fewer drop-offs → better funnel efficiency

Every removed friction point increases the percentage of users moving forward. The result is higher output from the same traffic — a direct and measurable UX impact on CAC.

Usability → frequency

If tasks are easy to complete, users return more often. Over time, this increases engagement depth and expands usage scenarios — a fundamental driver of UX for retention and growth.

Continuity → retention

Products that preserve context across sessions, devices, and channels reduce the need to “start over.” This continuity lowers churn and strengthens UX impact on retention and churn.

Transparency → trust & monetization

Clear system feedback, understandable pricing, and predictable outcomes build confidence. This directly affects willingness to pay and upgrade — a key link between product experience and LTV.

Across all these points, the pattern is consistent: UX is not a layer on top of the product — it is the mechanism through which LTV grows and CAC becomes more efficient.

Challenge

Users comparing mobile banking apps faced difficulties making informed decisions about which bank to choose and which services to trust. Key differences between products were not clearly communicated within the interface, and important functionality was either hard to discover or poorly explained. As a result, users could not easily understand product value during early interactions, which reduced conversion from interest to active usage.

What we did

We conducted a comparative UX benchmark of mobile banking apps, analyzing how effectively each product supports users in key scenarios — from initial exploration to performing financial tasks.

The assessment focused on:

We identified best practices and gaps in how leading apps guide users toward first meaningful actions and help them evaluate the product.

Impact

By improving visibility of key features and clarifying product value within the interface, banks can reduce user uncertainty at early stages. This leads to higher activation rates and more efficient conversion from acquisition to usage — a direct UX impact on CAC.

At the same time, better structured early experience sets expectations and builds trust, increasing the likelihood of continued use and contributing to UX and customer lifetime value.

Challenge

Financial companies were looking for ready-made fintech solutions to expand their product offering, but struggled to evaluate and integrate them effectively. From a user perspective, this translated into fragmented experiences: new services appeared in products without clear positioning, inconsistent UX, and weak integration into existing scenarios. As a result, users did not adopt new functionality or used it only once — limiting retention and long-term value.

What we did

We conducted a structured analysis of fintech solutions available on the market and evaluated how they can be integrated into digital products from a UX perspective.

The work focused on:

We also mapped how different solutions support recurring use cases — the key driver of retention.

Impact

By integrating services in a way that aligns with existing user scenarios, products can significantly increase feature adoption and usage frequency. This turns new functionality from a one-time interaction into a recurring habit.

As a result, companies strengthen UX for retention and growth, directly impacting UX and customer lifetime value through deeper engagement and expanded usage over time.

Challenge

Banking chatbots were widely used, but mostly limited to basic support scenarios. Users could resolve simple issues, but complex or high-value tasks still required switching channels or contacting human support. This broke continuity, reduced trust in the channel, and limited both usage depth and monetization potential.

What we did

We analyzed how chatbots can evolve from support tools into full-scale business assistants integrated into key financial scenarios.

The work focused on:

We also defined best practices for embedding chatbots into core product journeys rather than treating them as a separate channel.

Impact

Expanding chatbot capabilities and improving interaction quality allowed users to complete more tasks without leaving the interface. This increased frequency of use and reduced dependency on alternative channels.

As a result, the product strengthened engagement and trust, unlocking new monetization opportunities. This demonstrates a clear link between product experience and LTV, as well as the broader UX impact on retention and churn.

UX should not be treated as interface quality — it is a driver of unit economics. The UX impact on unit economics becomes visible when you stop measuring screens and start measuring task success, time-to-value, and scenario completion rates. This shift is critical: it connects design decisions directly to business outcomes.

LTV and CAC cannot be improved through marketing alone. Acquisition can bring users in, but only product experience determines whether they activate, return, and generate value over time. The real lever is how effectively the product helps users achieve their goals — consistently, predictably, and without friction. This is the foundation of both UX and customer lifetime value and how UX reduces customer acquisition cost.

In practice, this requires moving from isolated UX improvements to a systematic approach:

This is where UX and conversion rate optimization and UX impact on retention and churn become part of the same system — not separate initiatives.

We consistently see this pattern across our research at Markswebb: products that measure UX at the level of real user tasks outperform competitors in both acquisition efficiency and long-term value. The difference is not in design polish — it is in how well the product executes critical scenarios.

In practical terms, strong UX can deliver measurable impact:

These effects compound over time, which is why the relationship between UX and unit economics becomes more visible as products scale.

Ultimately, companies that treat UX as a measurable system — not a visual layer — are the ones that improve LTV/CAC predictably. They invest not only in acquisition, but in improving retention through UX design, building trust, and expanding usage. This is what drives sustainable growth and defines leaders in competitive benchmarks.

If you want to understand how UX design improves LTV in digital products or how UX impacts CAC in SaaS and fintech — and apply it to your product with measurable results — reach out to us.

We respond to all messages as soon as possible.

We’ve evolved dozens of successful financial services and are eager to prove that our expertise can be implemented in other industries and around the world. Have a look at our success stories!