By 2026, the migrant banking sector has moved far beyond simple currency exchange. With the rise of credit portability services (like Nova Credit) and the increasing burden of remittance taxes, migrant customers are demanding more than just a debit card—they demand a seamless financial home. But how well do traditional digital banks actually serve them? This benchmark of 6 Eastern European banks reveals a fragmented market and uncovers the UX strategies that truly reduce ambiguity for foreign users.

Contents

The starting point of the migrant banking research was a growing interest among banks in Eastern Europe in better serving migrant customers. To address this, we adapted our mobile banking benchmark methodology to analyze the experience of this specific segment. This approach made it possible to objectively compare how different banks support migrant users and to examine the experience across multiple service channels rather than focusing on a single interface.

The evaluation criteria and their weights were revised to reflect scenarios that are particularly important for migrants. This resulted in a structured framework for assessing the banking experience of foreign users as a distinct audience with specific needs, rather than treating them as a minor variation within the general customer base.

The research covered six banks operating in an Eastern European market. These included widely recognized services among migrant customers as well as banks that publicly offer products designed for foreign users.

For each bank, we examined both the website and the mobile application. The services were evaluated with the help of non-resident agents who were not customers of the banks at the beginning of the study. They provided access to the digital services, after which researchers documented how different features and scenarios were implemented.

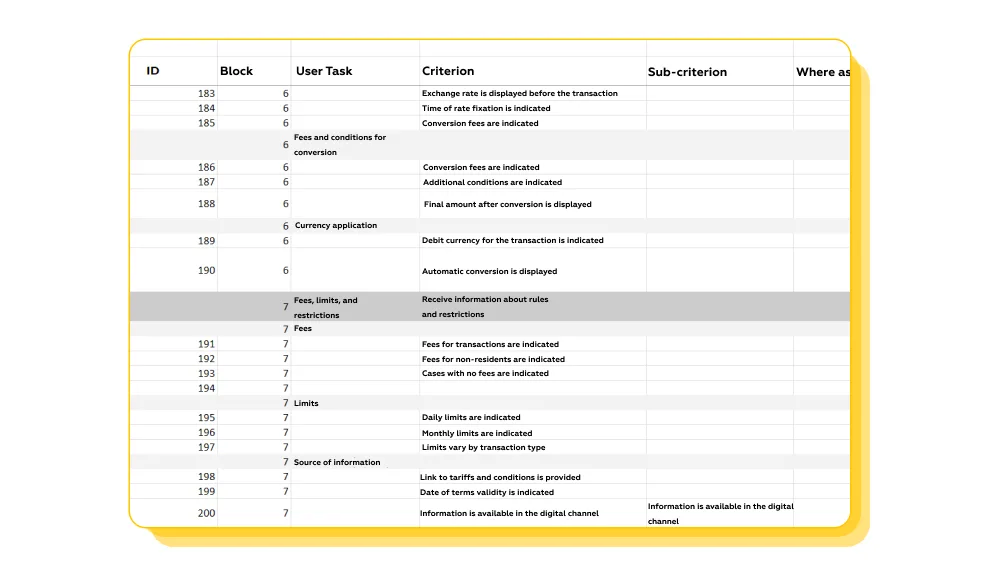

In total, the evaluation included more than 200 criteria grouped into nine major task areas. Each criterion was verified directly within the service using a binary model: it was either implemented or not. This approach allowed the researchers to capture the actual user experience rather than relying on product descriptions or marketing materials.

The analysis covered the entire journey of a migrant customer — from the first interaction with information on the website to opening financial products, managing accounts and cards, making transfers, and interacting with customer support.

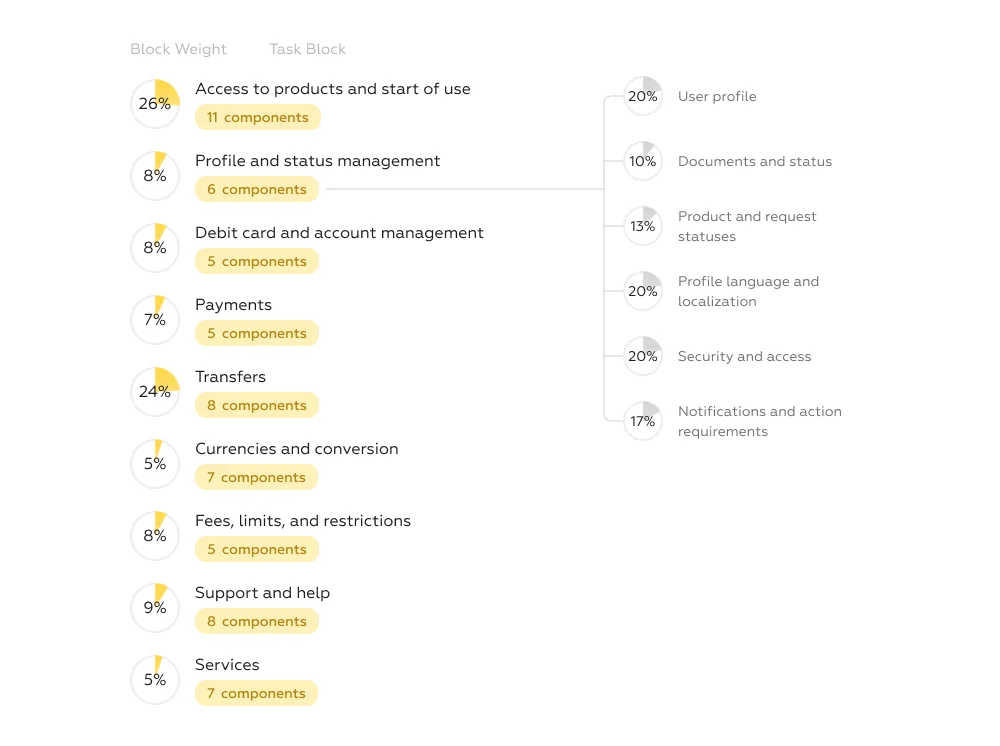

The specific needs of immigrant users influenced not only the selection of evaluation criteria but also their relative weights in the final score. Scenarios that are more critical for migrant customers had a stronger impact on the overall assessment.

To better understand what matters most for foreign users in migrant banking services, the framework was informed by qualitative research conducted by an independent research agency in collaboration with a research center. Based on these insights, a representative user persona was developed and experts assigned weights to different criteria and task groups in the overall evaluation.

The weight of each task group reflected several factors:

This need for clear status verification aligns with the global trend of Credit Portability. In markets like the US and UK, newcomers no longer accept starting from zero; they expect their financial history to follow them via platforms like Nova Credit or Zolve. While Eastern European banks in our study are just beginning to explore this, the banks that scored highest showed a systematic approach to clarifying which foreign documents are accepted, laying the groundwork for future integration with international credit data. This isn't just about compliance anymore—it's about recognizing a migrant's pre-existing financial identity.

To accurately model the experience of migrant banking customers and understand which banking tasks matter most to them, the research was built around a working user persona — a generalized portrait of a immigrant user based on qualitative interviews and analysis of real migration scenarios.

The persona represents a typical migrant customer who has recently arrived in the country.

Example persona

Our persona (a 29-year-old worker) represents a significant segment. However, the 2026 market is increasingly shaped by international students who face even stricter collateral requirements for loans. While our benchmark focused on the general migrant worker, the UX patterns identified—clear document lists, multilingual support, and step-by-step guidance—are universal. The banks that master these for our persona will be best positioned to capture the growing, yet underserved, international student demographic highlighted in spring 2026 enrollment trends.

Using this evaluation framework, we assessed the quality of digital user experience provided by several banks operating in an Eastern European market across all task groups and scenarios.

Scores were calculated on a scale from 0 to 100 and reflected how effectively each service supports migrant users throughout the digital journey.

The results show that the market is still developing and remains highly uneven. Overall experience scores vary widely across banks, indicating large differences in how services support migrant customers. Even the closest competitor trails the leading bank by a noticeable margin.

While most banks demonstrate relatively mature functionality in standard banking operations, clear differences emerge in early-stage scenarios and in managing the status of migrant customers. These differences point to a structural split in the market and growing competition in how banks design services for foreign users.

The leading position is occupied by a bank in Eastern Europe that demonstrates a highly systematic approach to migrant banking support. Its strong performance is driven by balanced quality across the entire customer journey — from onboarding to everyday operations and support. The service clearly communicates which products are available to migrant users, provides broad international transfer coverage, and supports multiple interface and support languages. The app also includes additional services that help migrants navigate administrative tasks and integrate into everyday life in the country.

Other banks show solid performance in core banking functionality but provide more limited adaptation for migrant-specific needs. For example, some offer multilingual product pages or basic information for foreign users but lack detailed guidance or structured sections that help migrants navigate available services.

A third group of banks provides only minimal support for migrant customers. In these services, migrants typically have access only to basic products such as a debit card, domestic transfers, and a limited set of payments. International operations are often restricted, localization options are fewer, and the product offering is narrower. As a result, many migrant-specific scenarios remain only partially supported.

Globally, the market for starter credit cards aimed at 'credit invisibles'—including immigrants—is booming. Yet, our research shows a gap in Eastern Europe. While banks provide basic debit accounts, few have adapted their credit algorithms to consider alternative data, such as gig economy income or local utility payments. The bank leading our ranking succeeded by making its existing products understandable to migrants, but the next frontier, as seen in the US with cards from Petal or Tomo, will be using cash flow data to offer credit where no local credit history exists.

The benchmark framework also allows the experience to be compared across specific task areas.

Payments represent one of the most mature areas of digital banking. Scores across banks are relatively close, and most services successfully support routine payments such as mobile services, internet subscriptions, and utilities. However, differences still appear in details — particularly in the clarity of forms, explanations of conditions, and assistance provided when errors occur.

Certain payments that are especially relevant for migrant users can still be difficult to find. In some services, these payments are clearly labeled and easy to access. In others, they are hidden within general payment categories without clear explanations, making it difficult for users to understand which option they should choose.

With the introduction of new remittance taxes in 2026 and rising living costs, the ability to send money home cheaply is no longer a 'nice-to-have' but a primary driver of bank choice. Migrants are shifting from traditional money transfer operators to digital corridors. Our benchmark found that while routine local payments are mature, international transfers remain a friction point. Best-in-class banks in our study made remittance options visible and clearly labeled, directly addressing the 'crisis of cost' that defines the 2026 remittance landscape.

Another area where services differ significantly is customer support.

Support channels exist in most banking apps for migrants, typically including in-app chat, hotline numbers, and the ability to submit requests with attached documents. However, the quality and accessibility of these channels vary widely.

In some services, contact information is available directly within the app interface, while in others it is hidden behind multiple steps or only accessible through the website. If a user remains inside the mobile app, it may even appear that phone support is unavailable.

Information about support availability and response times is not always clearly communicated. In some services, users can track the status and history of their support requests, while in others this functionality is missing.

Support in foreign languages remains particularly limited. Only a small number of banks provide multilingual support within their services, and explicit information about available languages is rarely communicated. For migrant customers, this is critical: language barriers significantly increase the complexity of solving any problem.

Specialized information for migrant banking users is also uncommon. In rare cases, apps provide dedicated sections that aggregate useful information and guidance. In most services, however, relevant materials are scattered across the website or not clearly highlighted within the digital interface.

The migrant banking research identified more than ten recurring problems in digital banking services for migrants, as well as over thirty best practices that help address these issues and improve the effectiveness of digital service channels.

Most difficulties arise because foreign users struggle to understand which banking products are available to them, what documents are required, and how specific operations — such as international transfers, limits, and currency transactions — actually work. The most effective solutions address this problem by making conditions explicit, adapting interfaces to reflect the user’s status, introducing dedicated navigation for migrant-related scenarios, and providing clear step-by-step explanations for complex tasks.

These design approaches help migrants navigate traditional banking services that were originally built for local users. In complex product catalogs and unfamiliar interfaces, clear structure and guidance allow foreign customers to quickly find the scenarios that are relevant to them.

Below are two examples of practices that help reduce ambiguity — one of the most common barriers in migrant banking journeys.

One example is implemented by a bank in Eastern Europe, where a payment form specifically relevant for migrant banking users is placed in a clearly visible location within the interface. This reduces the time required to find the necessary function and helps users quickly access an operation that is important for their everyday life. A dedicated navigation element labeled for migrant-related needs guides users directly to the services most likely to be relevant to them.

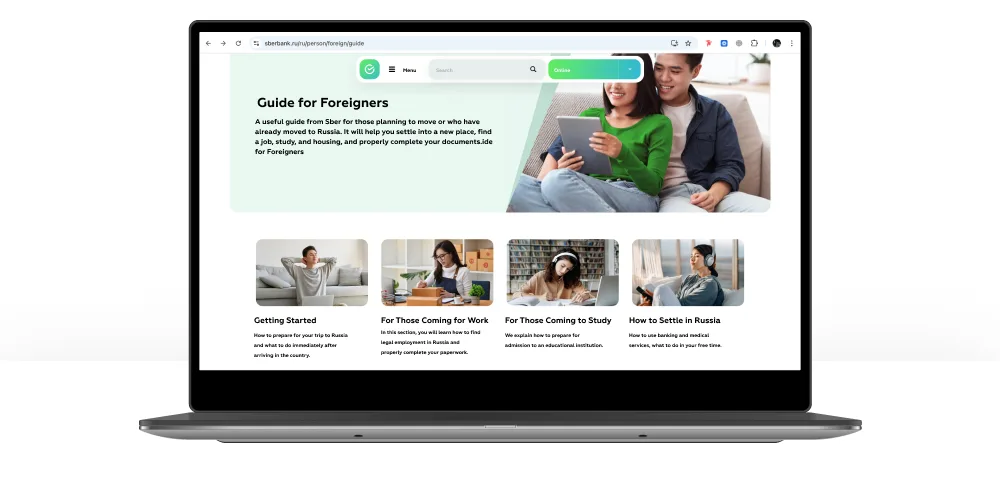

Another example is a structured information hub designed for migrant banking customers. In this implementation, the bank provides a dedicated section that aggregates guidance and service information in a single place. The page is divided into several thematic blocks that help users navigate the available services based on their goals — for example, starting to work in the country, managing finances, or sending money abroad. This structure helps migrants avoid confusion and better understand which services they can use.

This migrant banking research demonstrates how evaluation frameworks can be adapted to analyze the experience of a specific customer segment or industry scenario. By focusing on migrant users, the benchmark provides a clear view of how different banks support this audience and where meaningful gaps still exist.

Such analysis helps organizations objectively assess the competitive migrant banking landscape, identify strengths and weaknesses across key customer journeys, and understand where services differ — from the first interaction with the bank to everyday operations and customer support.

Expert evaluation also allows internal assumptions to be compared with real market practices. For executives, this creates a transparent picture of the maturity level of their digital services. For product teams, it provides concrete guidance on which improvements can deliver the greatest impact.

Benchmarking also highlights practices that can be adopted from other services and identifies areas where innovation can create differentiation. By focusing on measurable user experience rather than intuition alone, banks can make more informed decisions when designing services for strategically important customer segments.

The migrant of 2026 expects a bank that recognizes their global financial identity from day one. As credit portability becomes the norm and remittance corridors digitize, the banks that win will be those that reduce ambiguity in their UX.

Looking to benchmark your digital services against these global trends? At Markswebb, we adapt our evaluation frameworks to your strategically important segments. Contact our analysts to discuss a custom audit for your bank.

Every year we conduct up to 15 studies of digital services. These are industry benchmarks that reflect the state of the market and trends.