A regional bank approached Markswebb to identify opportunities for increasing digital sales of personal loans through its mobile app.

The team wanted to understand what prevented customers from completing the lending journey: how the customer journey worked in practice, where users lost motivation, which steps created unnecessary effort, and how interface and operational issues affected conversion from initial interest to loan disbursement.

Markswebb conducted a mobile lending UX audit covering the complete process — from finding and selecting a loan to receiving the funds. We also compared the journey with solutions implemented by leading banks, allowing the client to see not only where the experience failed but how each barrier could be removed.

Contents

Personal loans are among the banking products where the quality of the digital journey has a direct impact on business performance. The experience determines how many customers complete an application, how quickly they reach document signing, and whether they ultimately receive the funds.

The bank needed to identify where potential borrowers dropped out of the mobile journey and what prevented users who had already shown interest from completing the process.

The mobile lending UX audit focused on several factors with the strongest potential impact on conversion:

The customer journey analysis had to reveal where users encountered unnecessary actions, uncertainty, or delays—and what could be changed to shorten the path to loan disbursement.

The bank received a detailed customer journey map covering the digital personal loan process from product selection to the moment the funds reached the customer’s account.

The map highlighted every point where users faced additional effort, unclear information, waiting periods, or gaps between digital and assisted channels.

For each barrier, Markswebb explained its potential effect on customer behavior and loan application conversion. The analysis showed where a customer might:

We also developed practical recommendations and collected relevant examples from market leaders. The proposed improvements included:

The findings gave the product team a clear foundation for prioritizing improvements according to their business impact: shortening the journey, reducing support demand, and increasing digital loan sales.

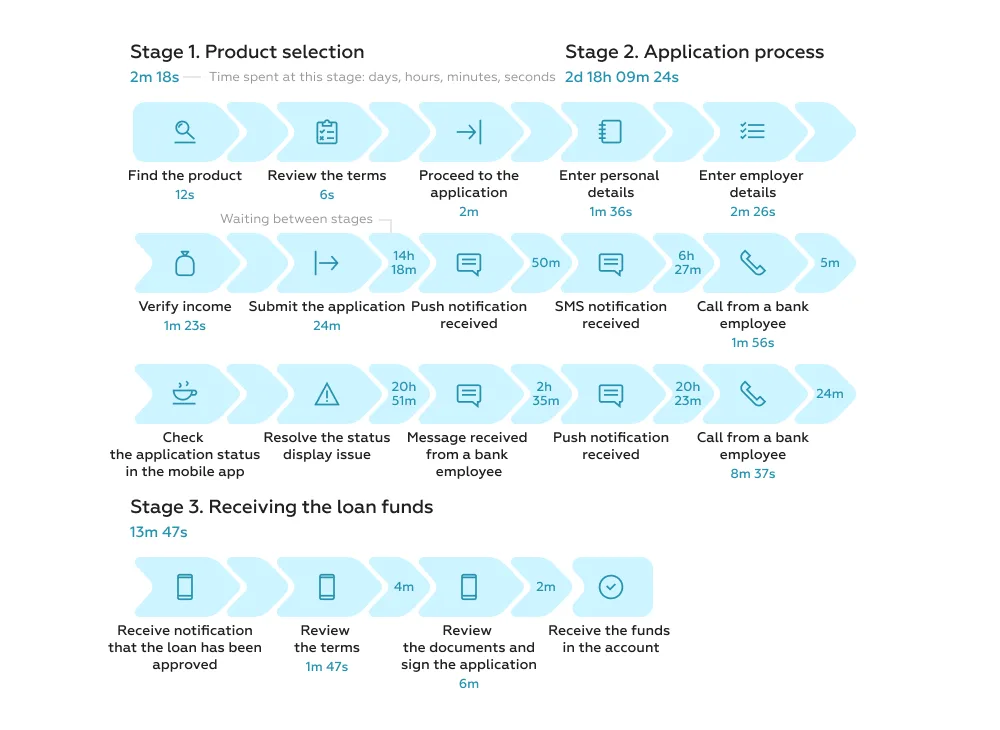

The research covered the personal loan experience in the bank’s Android application.

We divided the journey into three stages:

Markswebb researchers reproduced the full process using mystery shoppers. They located the product in the app, reviewed its terms, completed an application, waited for a decision, signed the required documents, and tracked the disbursement of funds.

At every step, the team recorded:

Based on these observations, we created a customer journey map of the complete digital loan process.

The map revealed where the app gave customers enough information and guidance, and where the experience introduced conversion barriers. These included unnecessary transitions, unclear loan terms, no preliminary payment calculation, outdated application statuses, and inconsistencies between push notifications, employee messages, and the status displayed in the app.

To make the recommendations actionable, we compared the client’s journey with implementations from leading banks. This showed which solutions were already being used to accelerate applications, improve transparency, and reduce the need for customer support.

The audit showed that the bank’s conversion problem could not be attributed to a single interface issue.

Instead, the customer experience was affected by a combination of product, UX, communication, and operational barriers.

At the beginning of the journey, customers could find the loan relatively quickly. However, they did not receive enough information to make a confident decision. The app lacked:

The barriers became more serious after the customer submitted the application.

Users expected a fast decision, but the process extended over a much longer period. Even after receiving messages suggesting that the loan had been approved, the status in the mobile app remained outdated.

As a result, customers had to determine what was happening on their own. They contacted the in-app chat, called the contact center, or waited for additional messages from bank employees.

The loan journey was technically available in the mobile app, but in practice it required manual support and additional customer effort.

This is particularly risky in lending. When customers need money urgently, they are unlikely to spend time resolving inconsistent statuses or switching between communication channels. They may instead apply through another bank offering a faster and more transparent experience.

The mobile lending UX audit also revealed a significant difference in processing time.

At the client bank, the complete journey from choosing a loan to receiving the funds took more than two days. At one of the market-leading banks, a comparable process took approximately 25 minutes.

Most of the delay occurred during the application stage. Customers waited for confirmation and encountered information in the app that did not reflect the actual state of the application.

For the business, this created a risk of losing customers after they had already demonstrated clear purchase intent.

The customer had found the product, completed the form, submitted personal data, and received an indication of approval. However, the process then became unclear.

At this point, the bank risked losing not only the loan disbursement but also the customer’s trust in the mobile channel.

The audit transformed the general impression that “the journey is difficult” into a specific map of conversion losses. It showed:

Markswebb focused its recommendations on the areas where the bank could most quickly influence loan conversion.

The proposed changes were designed to remove unnecessary actions, clarify product terms before application, accelerate the decision process, and eliminate communication gaps after approval.

Increase completed applications

Customers are more likely to submit an application when they understand the offer before the process begins.

Showing an estimated payment, key requirements, expected timelines, and required information reduces uncertainty and helps users make an informed decision.

Reduce drop-off while customers wait for a decision

An up-to-date application status, a clear decision timeline, and an obvious next step help customers remain engaged after submitting their information.

This is especially important because the customer has already invested effort in the process and may be highly motivated to complete it.

Lower customer support demand

When the app does not explain the current status or expected timeline, customers contact the chat or call center.

Providing this information directly in the interface can reduce repetitive questions about approvals, document signing, and fund disbursement.

Strengthen the mobile app as a sales channel

A mobile channel becomes a complete lending channel only when customers can select a product, apply, receive a decision, sign the documents, and obtain the money without manual assistance.

Removing operational and UX gaps allows the bank to process more loans digitally.

Increase digital disbursements without acquiring more traffic

A shorter and more transparent journey can generate more loan disbursements from the bank’s existing mobile audience.

Instead of investing only in attracting new applicants, the bank can increase sales by helping more users complete journeys they have already started.

A customer journey audit connects individual UX issues with measurable business outcomes. It helps the product team understand not only where users experience difficulty, but how those barriers may affect sales, operational costs, and digital-channel performance.

Application conversion

The audit identifies where customers lack the information needed to decide whether to apply—for example, estimated payments, timelines, document requirements, or product restrictions.

Improving these areas can help more users progress from viewing the loan offer to submitting an application.

Application-to-disbursement conversion

After submission, conversion depends on decision speed, accurate statuses, clear next steps, and the ability to complete the process without manual assistance.

When customers understand what is happening, they are more likely to sign the documents and receive the funds.

Digital loan sales

A shorter and more transparent journey allows the bank to generate more disbursements from its existing app traffic, without proportionally increasing customer acquisition costs.

Customer support workload

A mobile lending UX audit reveals where customers are forced to ask for help — for example, to confirm the application status, understand how the decision will be delivered, check disbursement timing, or clarify contract terms.

Closing these information gaps can reduce both initial and repeated support requests.

Trust in the mobile channel

When the application displays accurate information, explains loan terms, and supports the full process without interruptions, customers are more likely to perceive the mobile app as a reliable channel for purchasing complex financial products.

Speed of product improvements

The customer journey map helps the team prioritize changes according to their proximity to a lost application, a support request, or a breakdown in the digital process.

Instead of improving individual screens in isolation, the bank can focus first on the barriers with the greatest potential impact on conversion and operational efficiency.

The case demonstrated that providing an application form in a mobile app does not automatically create an effective digital lending experience.

Customers evaluate the journey as a whole: whether the offer is clear, whether the process moves at the expected speed, whether statuses are accurate, and whether they can complete every step without contacting the bank.

By mapping the full customer journey and comparing it with market-leading practices, Markswebb helped the bank identify where UX and internal processes were limiting digital loan sales — and which improvements could make the mobile channel faster, clearer, and more effective.

Every year we conduct up to 15 studies of digital services. These are industry benchmarks that reflect the state of the market and trends.